UK Q1 GDP Growth Steps Up

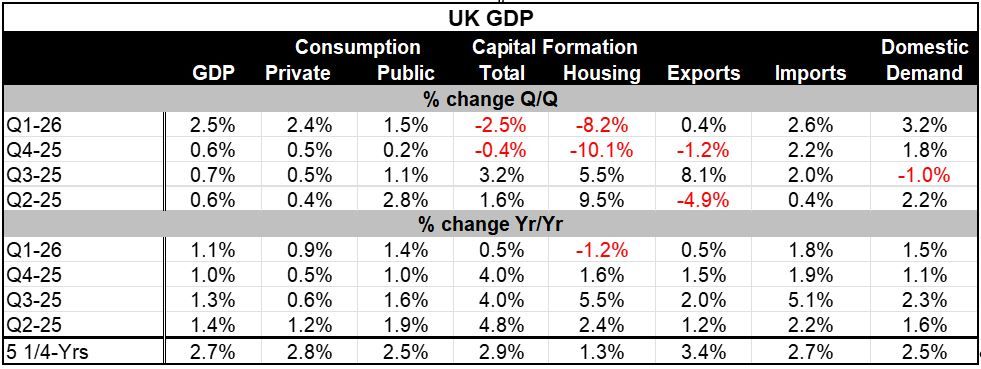

UK GDP grew by 2.5% in 2026-Q1. GDP growth quarterly was last this strong in 2024-Q2 and last stronger in 2024-Q1. This is the strongest quarterly growth in about two years. Private consumption surged in 2026-Q1, rising at a 2.4% annual rate. Capital formation and housing each backed off in the last two quarters. This is the opposite form the US where investment is strongly pushing growth ahead.

On the international side of the ledger, UK exports rose at a 0.4% annualized rate in the quarter while imports rose by a strong 2.6% annual rate, still, viewed on its own, domestic demand rose at a 3.2% annual rate.

Domestic demand growth has picked up to over 1% at 1.5% on a year-over-year basis. That is a good development. However, it is still a weak showing. Over the last 26 years domestic demand’s Year-on-year gain ranks at its 30th-percentiel; it has been weaker than this only about 30% of the time. But over the last nearly four-years the 1.5% gain is just below its median. This gives some indication of how weak growth has been in the post-Covid period. The UK was still in a post Brexit environment, when it had to deal with Covid, the invasion of Ukraine, and now the Middle East. At the same time, it has had a considerable amount of its own political turmoil and still does.

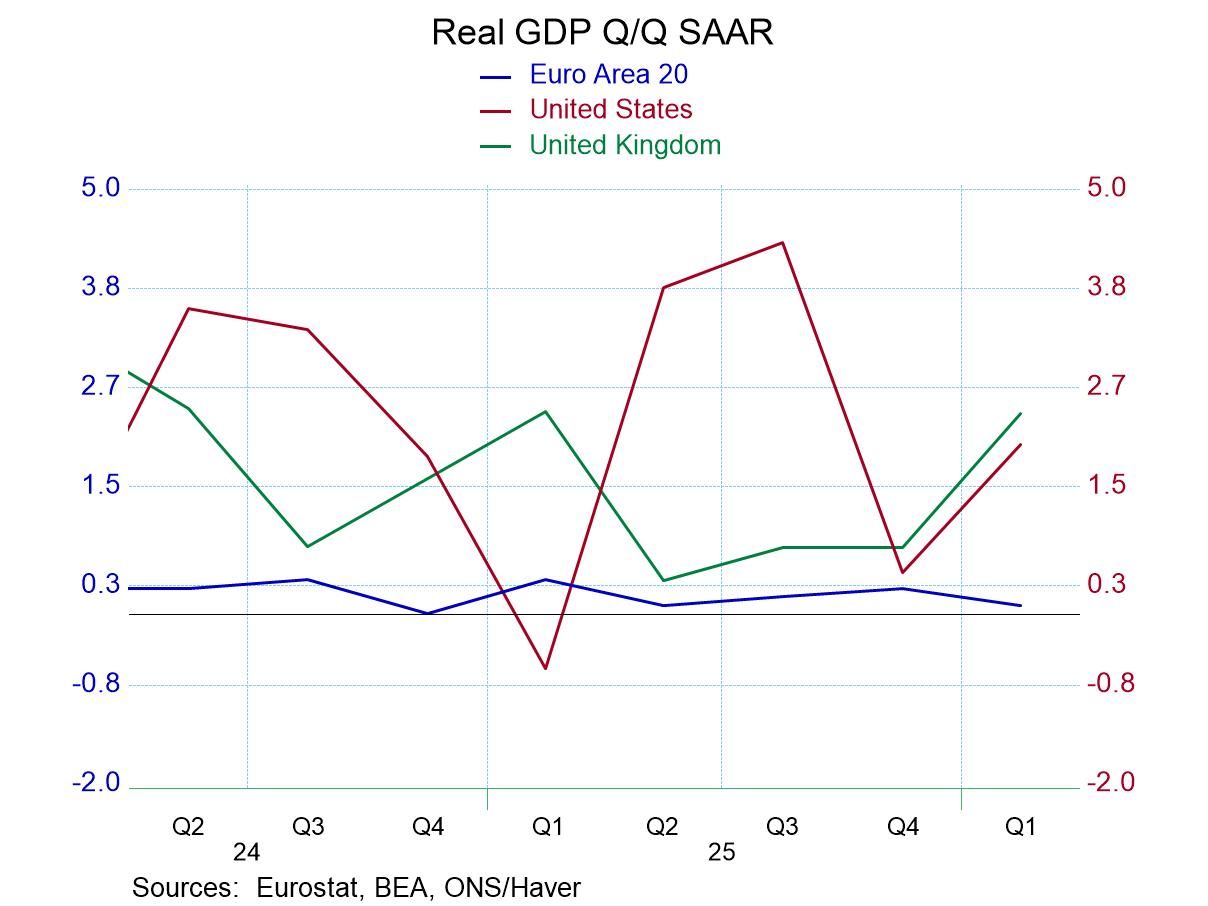

The chart above shows the snake crawl of GDP that continues to depict growth in the EMU area. That is a continuing weak environment- one of the UK’s important export markets. Europe’s fixation on social welfare spending and the need to tax to pay for it has robbed the economy of its dynamism. Still, both the UK and the Euro-Area continue to have lingering inflation issues. And both show current inflation in an upswing.

Central bankers' inflation and growth Central banks are playing a waiting game, the best that they can. Major money center country central banks have been consistently overshooting their inflation targets since Covid. And despite excess inflation banks have been reluctant to hike rates and have instead pursued a strategy of persisting slow rate reduction. It has been a curious period in which central banks have kept their inflation target goals but simply have been content to miss their targets in the short run and promise to thit them in the long run. This is clearly a policy of only temporary usefulness because it is bound to blow up, the longer inflation fails to be controlled at its targeted pace. For now, UK interest rates remain higher than in Europe, closer to the level in the US and with a monetary policy committee that seems determined to stop the overshoot as oil prices flare. We’ll see if the BOE MPC members are really ready to pull the trigger on higher rates as UK GDP growth looks firmer.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Asia

Asia