U.S. Personal Income and Consumption Post Solid Gains in August; Inflation Edges Up

by:Sandy Batten

|in:Economy in Brief

Summary

- Personal income increased 0.4% m/m but compensation slowed.

- Real PCE increased 0.3% m/m in August on top of a 0.4% m/m increase in July.

- July/August real PCE up 2.8% annualized from Q2 average, providing a solid base for Q3 GDP growth.

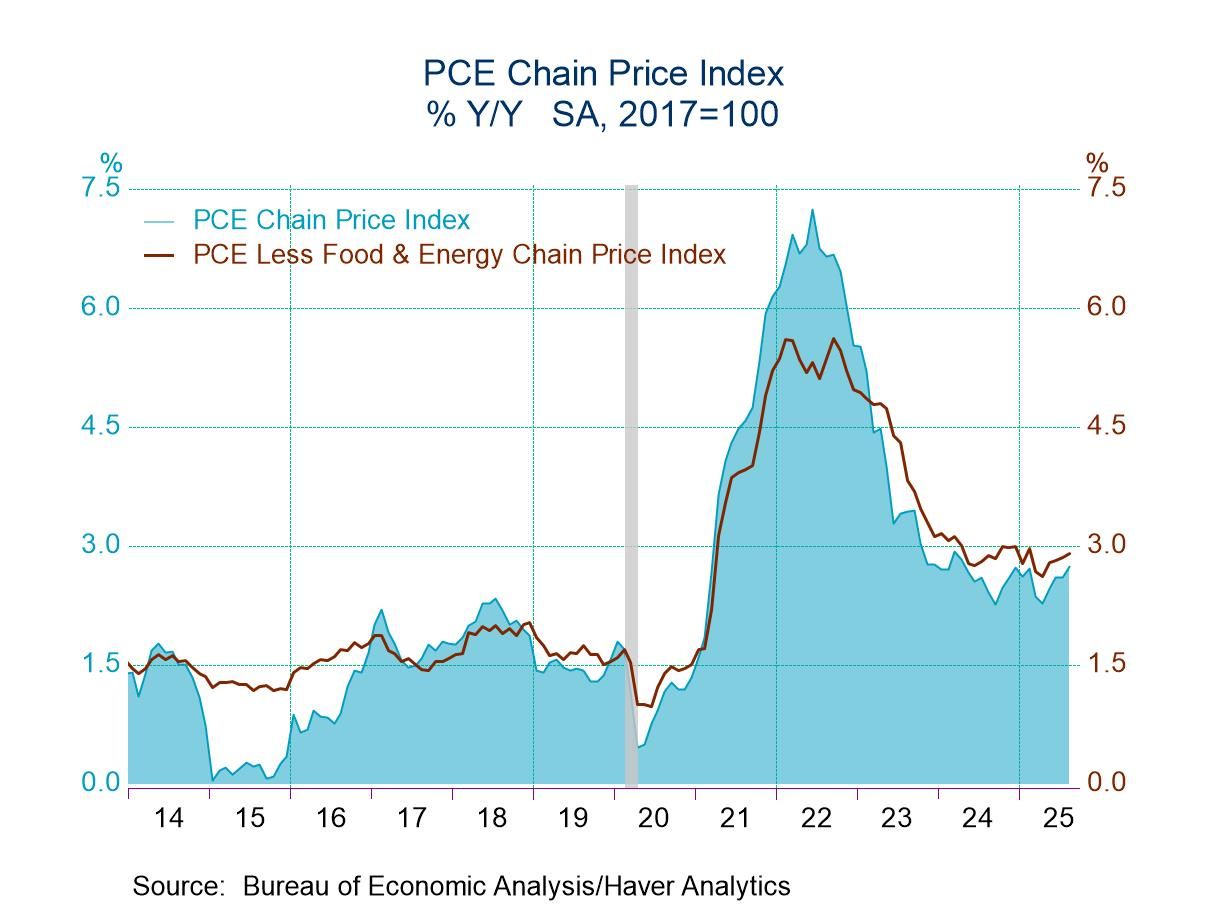

- Headline PCE inflation edged up further to the fastest y/y pace since February.

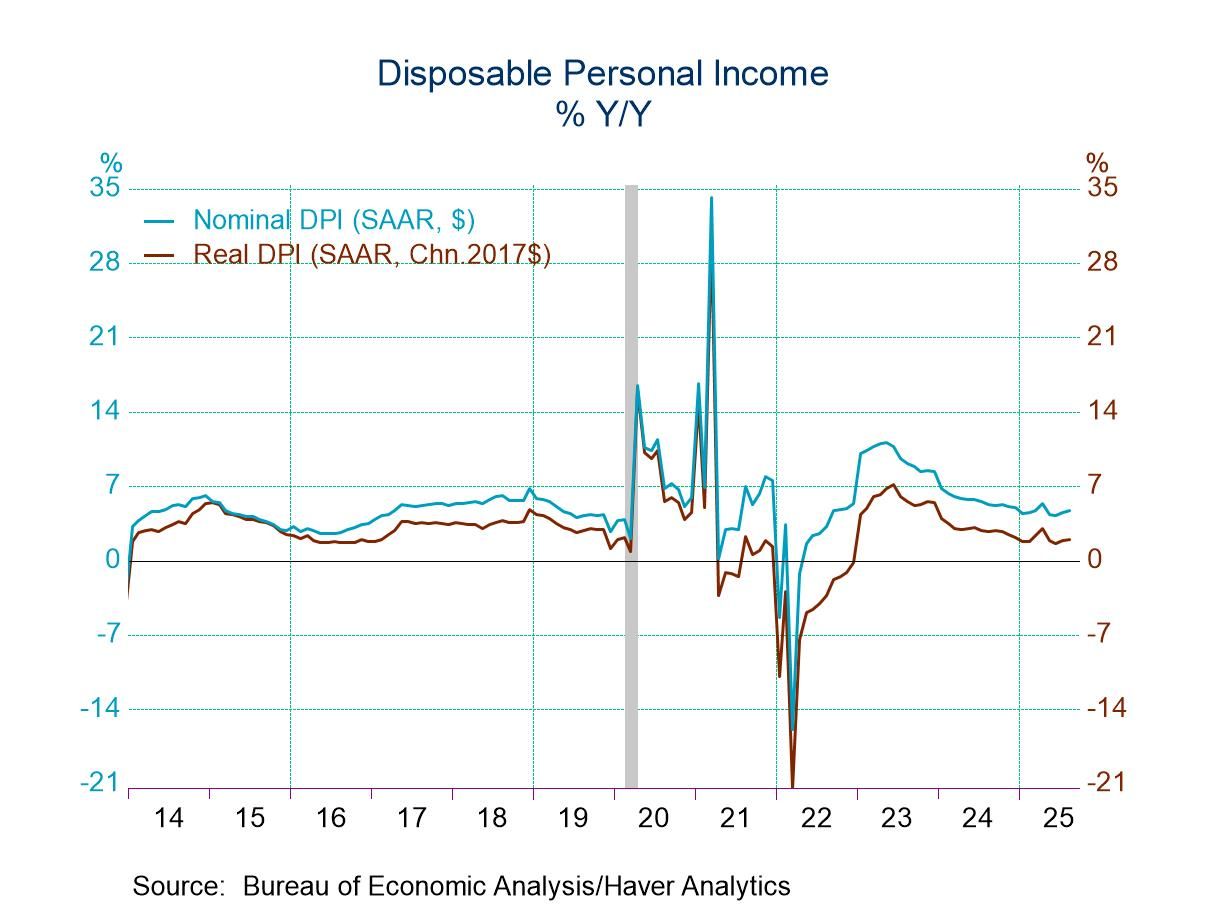

Personal income increased 0.4% m/m (5.1% y/y) in August, the same monthly gain as in July. However, growth of wages and salaries slowed to 0.3% m/m (4.9% y/y) in August from 0.5% m/m in July, a likely indication of slowing labor market conditions. The Action Economic Forecast Survey looked for a 0.3% monthly gain in personal income in August. Real personal income (that is, after adjusting for inflation) inched up 0.1% m/m (2.3% y/y) after a 0.2% monthly rise in July. Real disposable income also increased 0.1% m/m (1.9% y/y) in August versus 0.2% m/m in July.

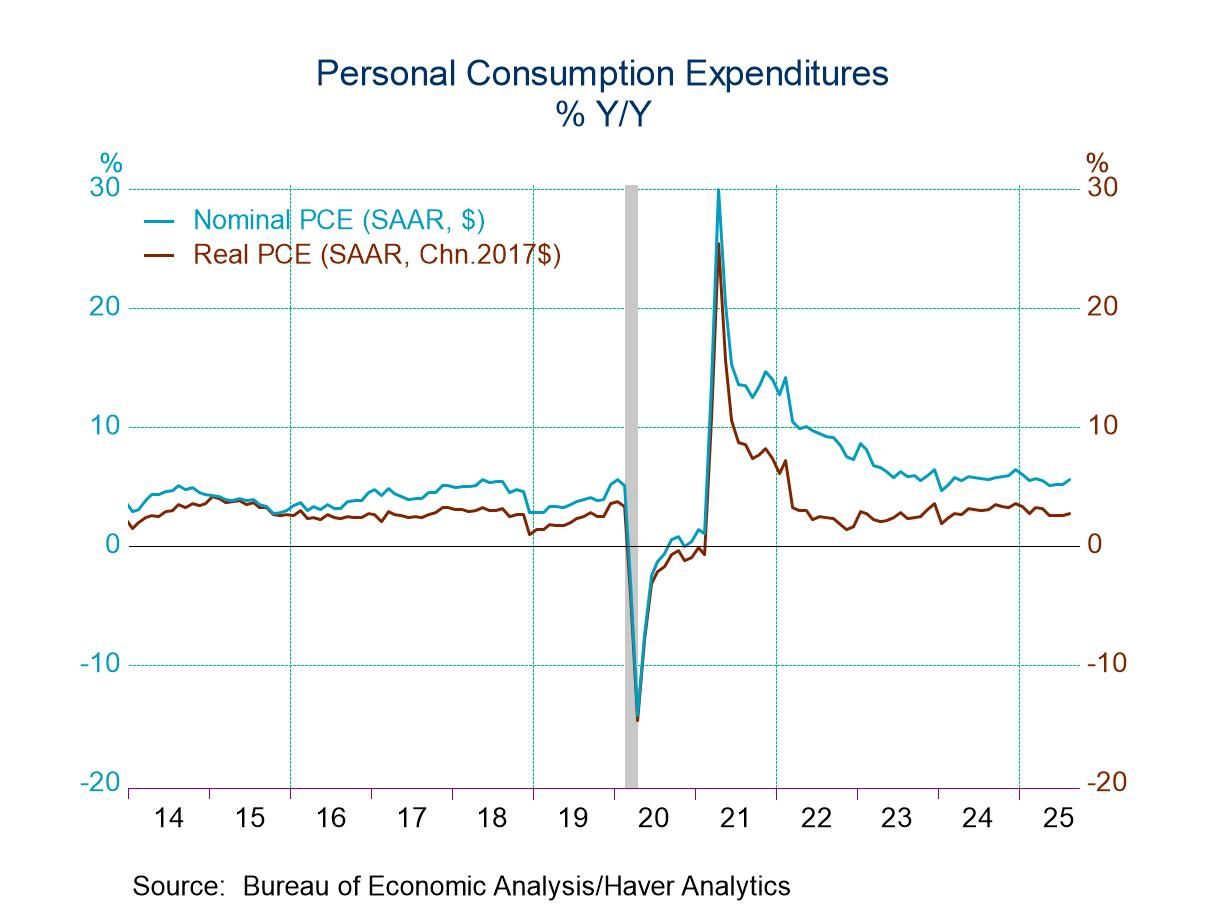

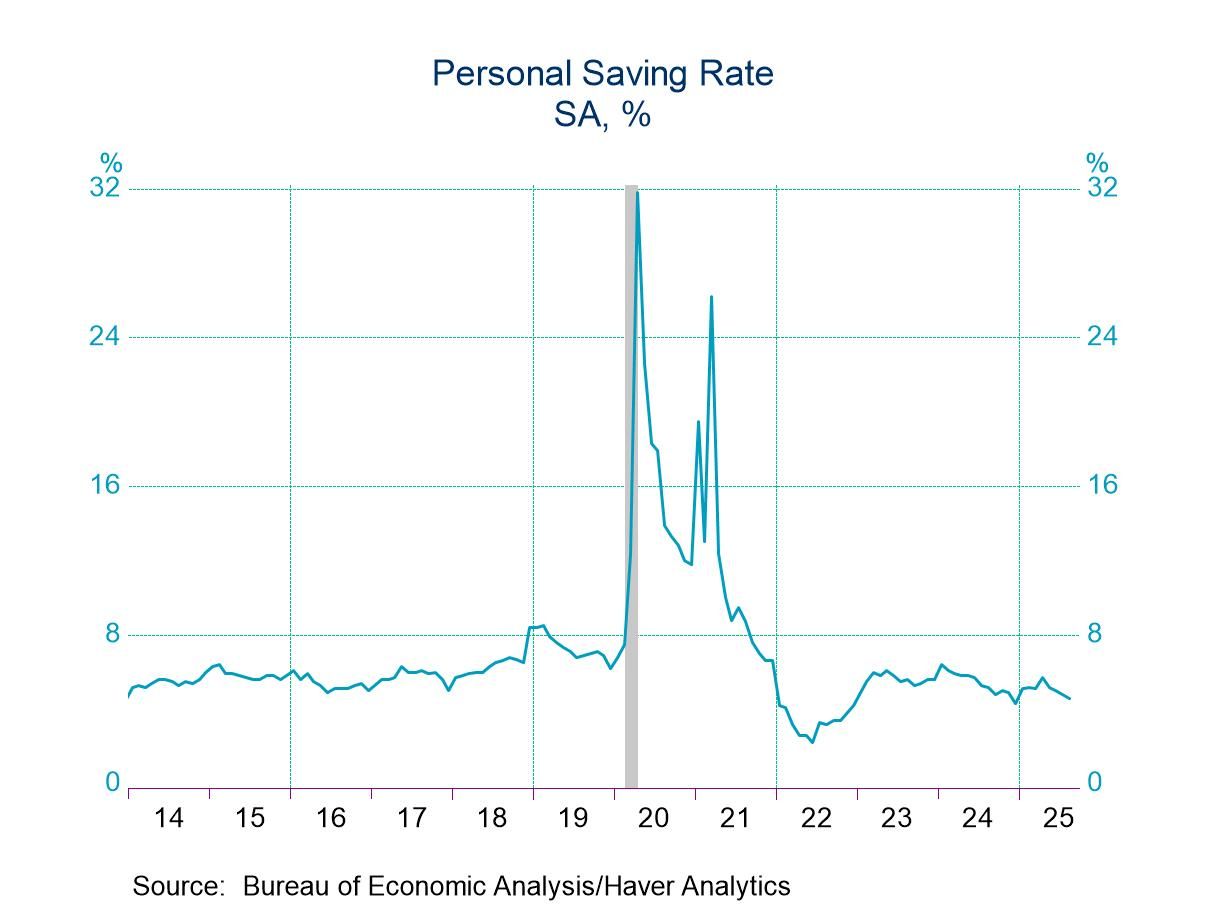

Personal consumption expenditures (PCE) posted another solid monthly gain, rising a larger-than-expected 0.6% m/m (5.6% y/y) in August on top of a 0.5% increase in both June and July. The Action Economics Forecast Survey looked for a 0.5% monthly gain. After adjusting for inflation, real PCE rose 0.3% m/m (2.7% y/y, the fastest annual pace since April) in August after a 0.4% m/m increase in July and a 0.3% m/m gain in June. The July/August average of real PCE stands 2.8% at an annual rate above the Q2 average. As PCE makes up around 2/3 of GDP, the solid July/August figure provides a strong base for Q3 GDP. With PCE growing a little faster than personal income in August, the saving rate slipped to 4.6% from 4.8% in July, which was revised up from 4.4%.

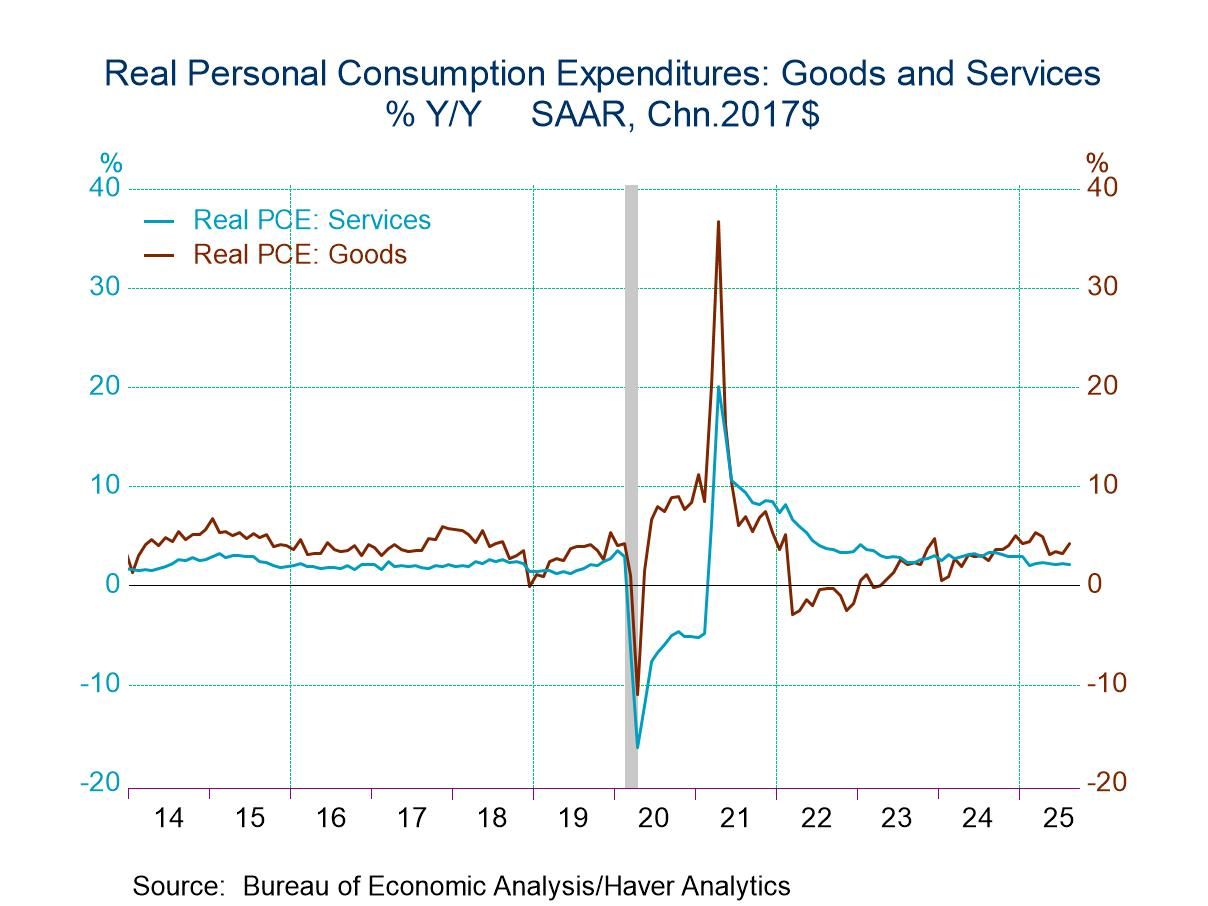

In PCE, real spending on goods increased 0.7% m/m in August, the same monthly advance as in July. Purchases of durable goods rose 0.9% m/m following a 1.8% monthly jump in July. Sales of motor vehicles slipped 0.3% m/m in August following a 2.9% surge in July. Nondurable goods sales picked up in August, rising 0.5% m/m after edging up 0.1% m/m in July. Consumption of services gained 0.2% m/m, the same monthly rise as in each of the preceding three months.

This report also contained benchmark revisions from the beginning of 2020 to the beginning of 2025. For annual data, these were relatively uneventful. After revision, personal income grew 6.3% saar from 2019 to 2024, up from 6.1% previously. Real disposable income rose 2.6% versus 2.3% previously. PCE increased 6.6% versus 6.5% while real PCE growth was unrevised at 2.9%. In general, in the benchmark revision, the monthly saving rate was revised up 0.4-1.0%-point per month, indicating a more solid financial position for households than previously estimated.

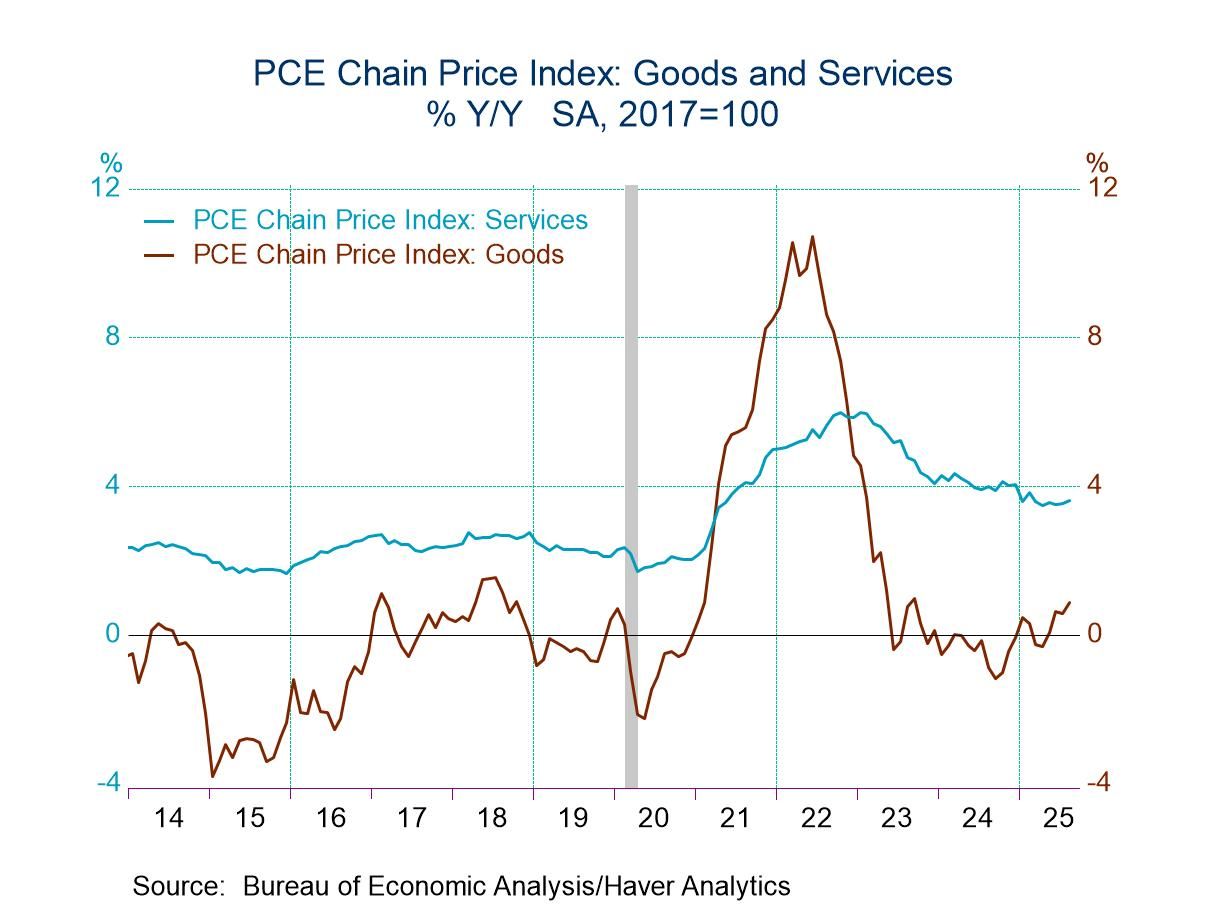

Inflation remained elevated in August, although this was generally expected, but it remains well above the Fed’s 2% target. The PCE price index increased 0.3% m/m in August, as expected, following a 0.2% monthly gain in July. The y/y rate rose to 2.7%, the fastest rate since February, from 2.6% in July. Goods prices inched up 0.1% m/m (0.9% y/y versus 0.6% y/y in July) with prices of durable goods falling 0.1% m/m and prices of nondurable goods rising 0.2% m/m. Prices of motor vehicles increased 0.7% m/m in August, their largest monthly gain since January. Prices of “other” durable goods soared 2.0% m/m, their largest increase since July 1991. The price of gasoline and other energy goods jumped 1.6% m/m in August, its largest gain since January.

Prices of services increased 0.3% m/m, the same monthly increase as in July. The y/y rate inched up to 3.6% from 3.5% in July. The core PCE price index (that is, excluding food and energy prices) rose 0.2% m/m in August, as expected and the same monthly increase as in July, with the y/y rate unchanged at 2.9%. Prices of services excluding energy and housing, a measure closely watched by the Fed, increased 0.3% (3.4% y/y) in August, up slightly from a 0.3% monthly increase in July.

The personal income and consumption figures are available in Haver’s USECON database with detail in the USNA database. The Action Economics forecasts are in AS1REPNA.

Sandy Batten

AuthorMore in Author Profile »Sandy Batten has more than 30 years of experience analyzing industrial economies and financial markets and a wide range of experience across the financial services sector, government, and academia. Before joining Haver Analytics, Sandy was a Vice President and Senior Economist at Citibank; Senior Credit Market Analyst at CDC Investment Management, Managing Director at Bear Stearns, and Executive Director at JPMorgan. In 2008, Sandy was named the most accurate US forecaster by the National Association for Business Economics. He is a member of the New York Forecasters Club, NABE, and the American Economic Association. Prior to his time in the financial services sector, Sandy was a Research Officer at the Federal Reserve Bank of St. Louis, Senior Staff Economist on the President’s Council of Economic Advisors, Deputy Assistant Secretary for Economic Policy at the US Treasury, and Economist at the International Monetary Fund. Sandy has taught economics at St. Louis University, Denison University, and Muskingun College. He has published numerous peer-reviewed articles in a wide range of academic publications. He has a B.A. in economics from the University of Richmond and a M.A. and Ph.D. in economics from The Ohio State University.

More Economy in Brief

Global

Global