U.S. ADP Employment Rises More than Expected in April

by:Sandy Batten

|in:Economy in Brief

Summary

- Private-sector payrolls rose 109,000 led by a pickup in service-producing employment.

- Services employment increased by 94,000 while the rise in goods employment slowed to 15,000.

- April job gains continued to be dominated by job increases at small firms.

- Wage growth was little changed but remained elevated for job stayers.

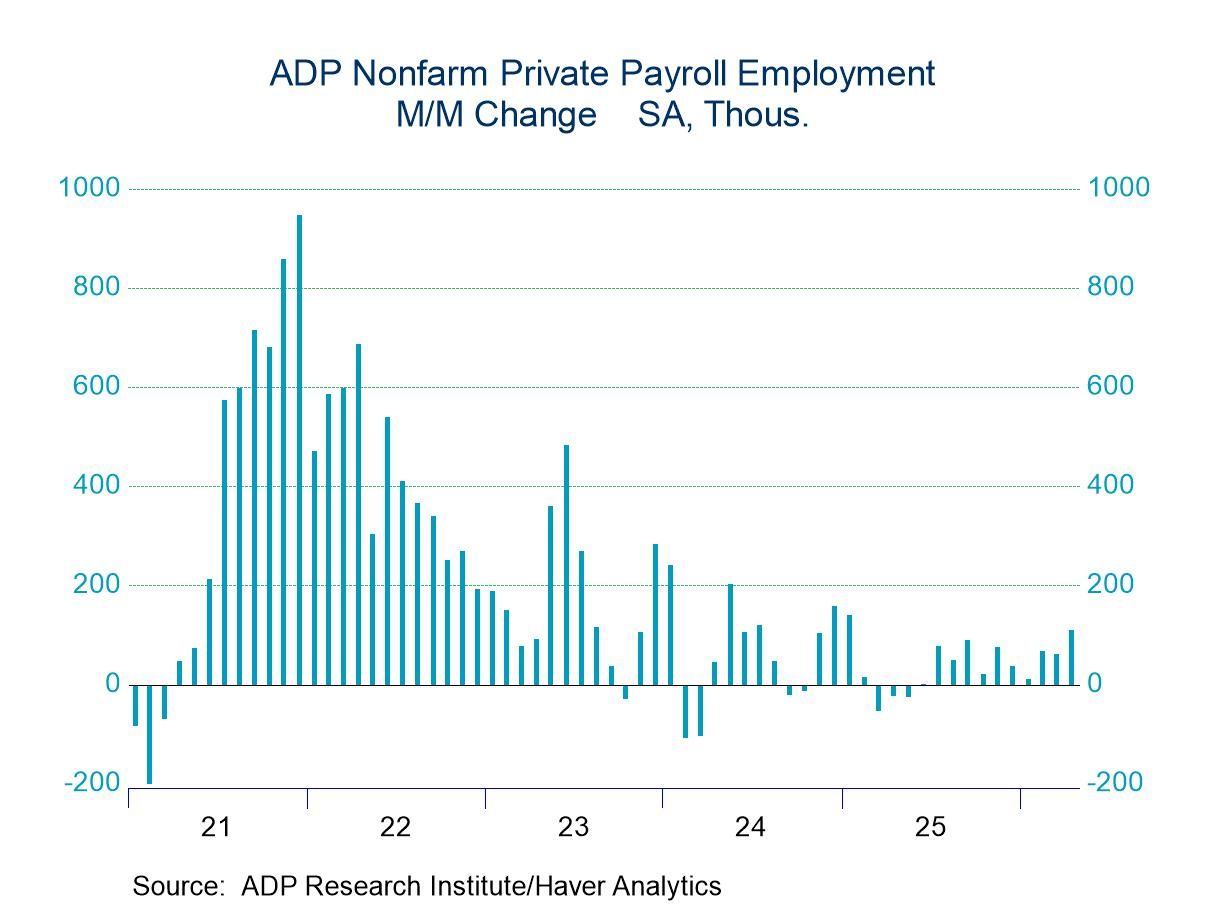

U.S. nonfarm private-sector payrolls rose a larger-than-expected 109,000 (+0.4% y/y) in April following a slightly downwardly revised 61,000 in March (previously 62,000), according to the ADP National Employment Report. The Action Economics Forecast Survey expected a 79,000 increase. The three-month average change rose to 79,000 in April from 46,000 in March and 38,000 in February. This was the highest three-month average change since February 2025.

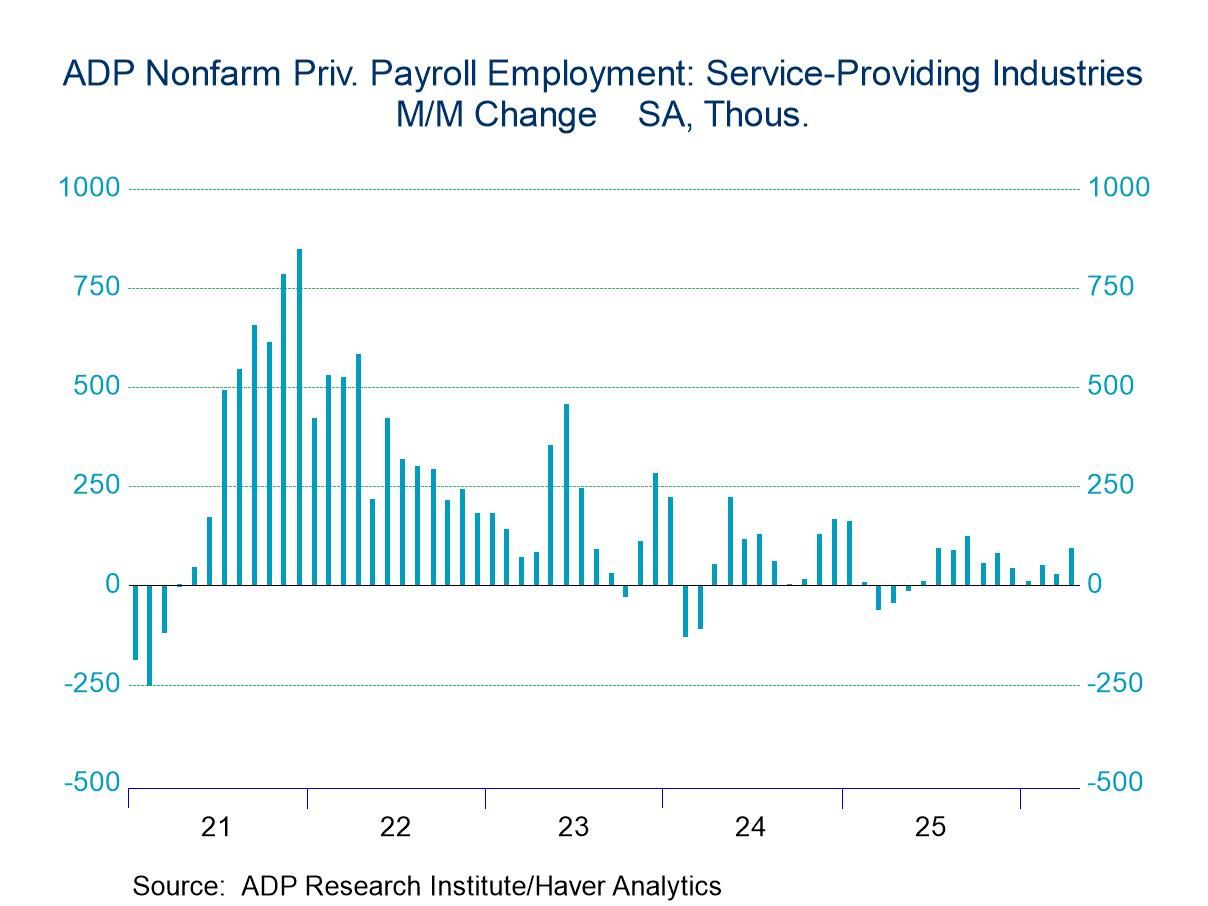

A pickup in service-producing employment led the April increase. The service-producing sectors added 94,000 jobs in April (+0.6% y/y) after a subpar 28,000 increase in March. Monthly gains in April were widespread with increases reported in every major industry except professional and business services (-8,000, the fourth monthly decline in the past five months). Education and health services employment continued to trend up, posting a 61,000 increase in April, the largest since last October. Trade, transportation and utilities employment rebounded in April, rising 25,000 after a 54,000 decline in March and a 1,000 fall in February.

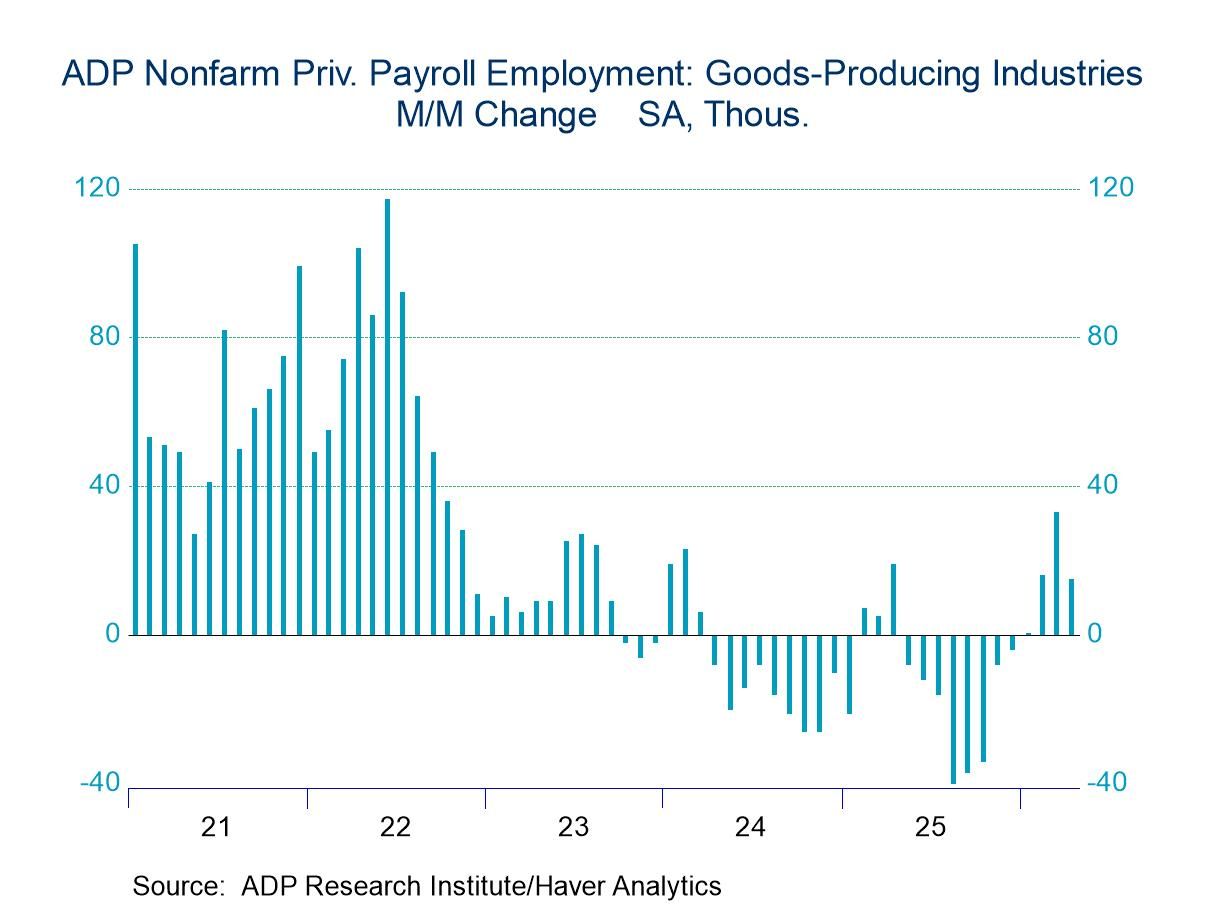

Goods-producing employment gains slowed in April with goods-producing sectors adding 15,000 jobs (-0.4% y/y) following an outsized 33,000 increase in March. Construction played the largest role in the slowdown with that sector adding 10,000 jobs in April versus 32,000 in March. Natural resources and mining jobs increased 3,000 in April, down from 13,000 in March. By contrast, manufacturing jobs increased by 2,000 in April. While this rise seems small, it was the first monthly increase since March 2024.

In terms of employment by firm size, increases at small firms (1-49 employees) continued to dominate. Employment at small firms rose 65,000 in April, the tenth consecutive monthly increase, on top of gains of 85,000 in March and 61,000 in February. Medium-size firms (50-499 employees) added only 2,000 jobs in April, but this was after a 20,000 decline in March and a 6,000 decline in February. Employment at large firms (500 or more employees) rose 42,000 in April following a 4,000 decline in March. Over the past four months, employment at large firms has risen only 30,000.

By region, nonfarm private sector employment increased 18,000 in the Northeast, 11,000 in the Midwest (the first increase in three months), 34,000 in the South and 46,000 in the West.

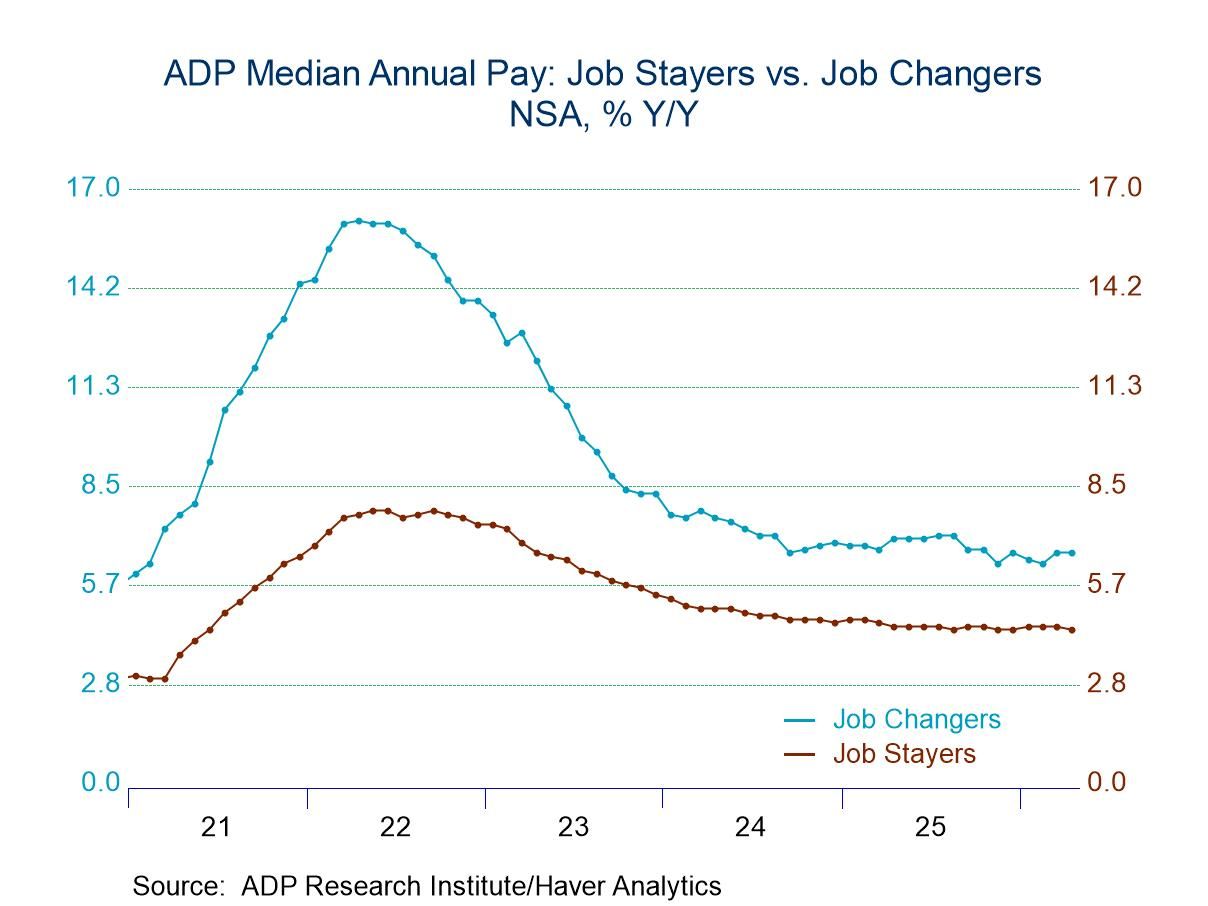

Wage growth for job changers was unchanged in April from March at 6.6% y/y. Job-changer wage growth has fluctuated between 6.3% and 6.6% over the past six months. Wage growth for job stayers slowed slightly to 4.4% y/y in April from 4.5% in March but remained elevated relative to rates that existed prior to the inflation surge in 2021-22. Job-stayer wage growth has been either 4.4% or 4.5% for the past 13 months. Wage growth in April either slowed or was the same as in March in every major industry.

The ADP National Employment Report and Pay Insights data can be found in Haver's USECON database. Historical figures date back to January 2010 for private employment. Pay data date back to October 2020. The expectation figure is available in Haver's AS1REPNA database.

Sandy Batten

AuthorMore in Author Profile »Sandy Batten has more than 30 years of experience analyzing industrial economies and financial markets and a wide range of experience across the financial services sector, government, and academia. Before joining Haver Analytics, Sandy was a Vice President and Senior Economist at Citibank; Senior Credit Market Analyst at CDC Investment Management, Managing Director at Bear Stearns, and Executive Director at JPMorgan. In 2008, Sandy was named the most accurate US forecaster by the National Association for Business Economics. He is a member of the New York Forecasters Club, NABE, and the American Economic Association. Prior to his time in the financial services sector, Sandy was a Research Officer at the Federal Reserve Bank of St. Louis, Senior Staff Economist on the President’s Council of Economic Advisors, Deputy Assistant Secretary for Economic Policy at the US Treasury, and Economist at the International Monetary Fund. Sandy has taught economics at St. Louis University, Denison University, and Muskingun College. He has published numerous peer-reviewed articles in a wide range of academic publications. He has a B.A. in economics from the University of Richmond and a M.A. and Ph.D. in economics from The Ohio State University.

More Economy in Brief

Asia

Asia