U.K. Inflation Dips and Shows Progress

It's an interesting time for the Bank of England to be meeting; it has its next policy meeting on June 18. Top money center central banks have been meeting, and the European Central Bank delivered a rate hike, with what is believed to be a likelihood of another hike before the end of the year. The Bank of Japan as just met and executed a 25-basis-point rate hike that brought the overnight interest rate up to 1% for the first time in 31 years. The Federal Reserve meets today and although the Fed is not expected to make an interest rate change, it is widely expected to remove the language that implies the next rate change is likely to be a reduction. Against that background, there is a pending deal to be signed on Friday between the United States and Iran to end the hostilities, to open the Strait of Hormuz, and to allow a normalization—or at least a transition toward normalization—of traffic flow through the Strait of Hormuz and the restoration of the delivery of the world's oil supplies.

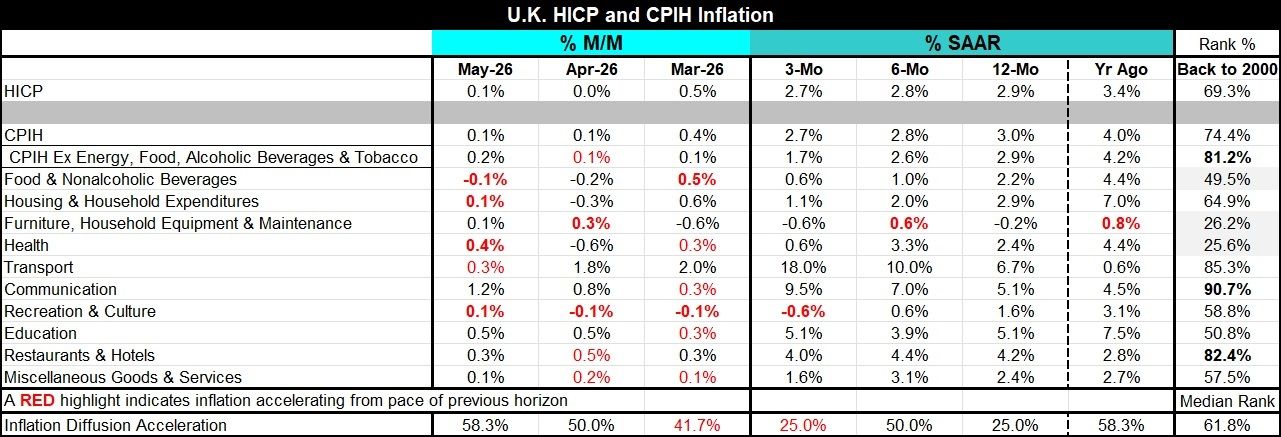

Against this background, the Bank of England will be making its rate decision. Part of this background shows other central banks having taken steps to become less accommodative or more vigilant against inflation risks and what have been ongoing overshoots of inflation targets by monetary policy globally. The Bank of England is part of this phenomenon as its rate of inflation, measured by the CPIH, is 3% year-over-year, a full percentage point above where it's supposed to be. However, both the CPIH and the HICP treatments for measuring U.K. inflation show inflation edging slightly lower—from 3% for the CPIH over 12 months to 2.7% over three months annualized. For the HICP, it moves from 2.9% over 12 months to a 2.7% annual rate over three months. Both of these are small moves but in the right direction. In addition, the CPIH core measure, excluding food, energy, alcohol, and tobacco, shows inflation declining from 2.9% over 12 months to 2.6% at an annual rate over six months, and to 1.7% at an annual rate over three months.

In short, inflation progress in the U.K. is very much in gear for the headline; inflation is quite moderately easing, however. For the core, the move lower is impressive and considerable. The question is whether the MPC at the Bank of England will find these movements sufficient in and of themselves to stay their hand and hold interest rate policy, or whether the Committee will join the ranks of central banks hiking interest rates to make sure that inflation makes that turn lower.

The situation in the Strait of Hormuz is hopeful, but not definitive, and there have been a number of ceasefires in the Middle East that have been called and then broken up relatively quickly. This time, markets are reacting to this particular announcement much more decisively and treating it as if this one is the ‘Real McCoy’ with oil prices having fallen down into the mid $70/barrel range and other indicators showing that markets are convinced that prices are moving lower too. Are the Bank of England's MPC members buying onto this as well? Or are they going to treat this as perhaps one last opportunity to get interest rates up and to make sure that the inflation rate goes down?

U.K. inflation on a monthly basis shows a slight tendency to accelerate in May, with inflation diffusion measuring inflation acceleration month-to-month at 58.3%, above the neutral reading of 50. However, diffusion had been at 50% in April and at 41.7% in March. Acceleration has been broadly blunted. In addition, the May increase in the CPIH was only 0.1%, the same as in April, with March having posted a much stronger increase of 0.4%.

Looking at trends sequentially over 12 months, six months and three months, diffusion is only 25% over 12 months; it is 50% over six months and 25% over three months. These metrics reinforce the view that inflation is not broadly accelerating but rather decelerating and moving back into line.

Taking the year-over-year inflation rate, it's a ranking of overall inflation rates back to January 2000. The headline CPIH is still high at a 74.4 percentile standing; that means it has been higher than 3% about 25% of the time and lower about 75% of the time. The average ranking across the various metrics in the table is 61%. That's above a ranking of 50% that delineates the median for the period. And despite the fast fall in the CPIH core rate, the year-over-year core is at 2.9% and has an 81.2 percentile ranking, meaning it has been higher since January 2000, less than 20% of the time. However, that 12-month rate of 2.9% is now down to 1.7% over three months. There are too many ways to look at inflation, at the environment, at what other central banks have done, and at trends to know with any certainty what the BOE will do.

The Bank of England has had a long period of overshooting its inflation target. It certainly will want to make sure that it's on a clear path toward getting inflation back to 2%. There's a question here about how much the Bank of England will want to trust the trend that it sees, how much it wants to trust the fast drop in the core rate, and then how much it wants to believe that the deal struck with Iran to open the Strait of Hormuz is going to prove durable. There are no real answers to these questions; they're going to be based upon opinions and perceptions, and they're also going to be based upon the pressure that the Bank of England feels about needing to make sure that it gets inflation back to 2% after its long period of intransigence. We'll find this out tomorrow.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Asia

Asia