Global| Aug 18 2025

Global| Aug 18 2025The Power of AI

The global race in the field of Artificial Intelligence is becoming a priority for both nations and firms alike. However, we are concerned that the overwhelming energy needs of AI will force countries to compromise on the competing goal of environmental sustainability. In the second of his three-part Viewpoint series, The Age of Constraints, Andy Cates did an energy reality check. There he highlighted real energy prices and the ever-changing energy demands that are needed to power and cool the data centers supporting AI functionality. We further explore how leading economies have pursued energy generation over the past 20 years and deduce which directions they might take to power up AI.

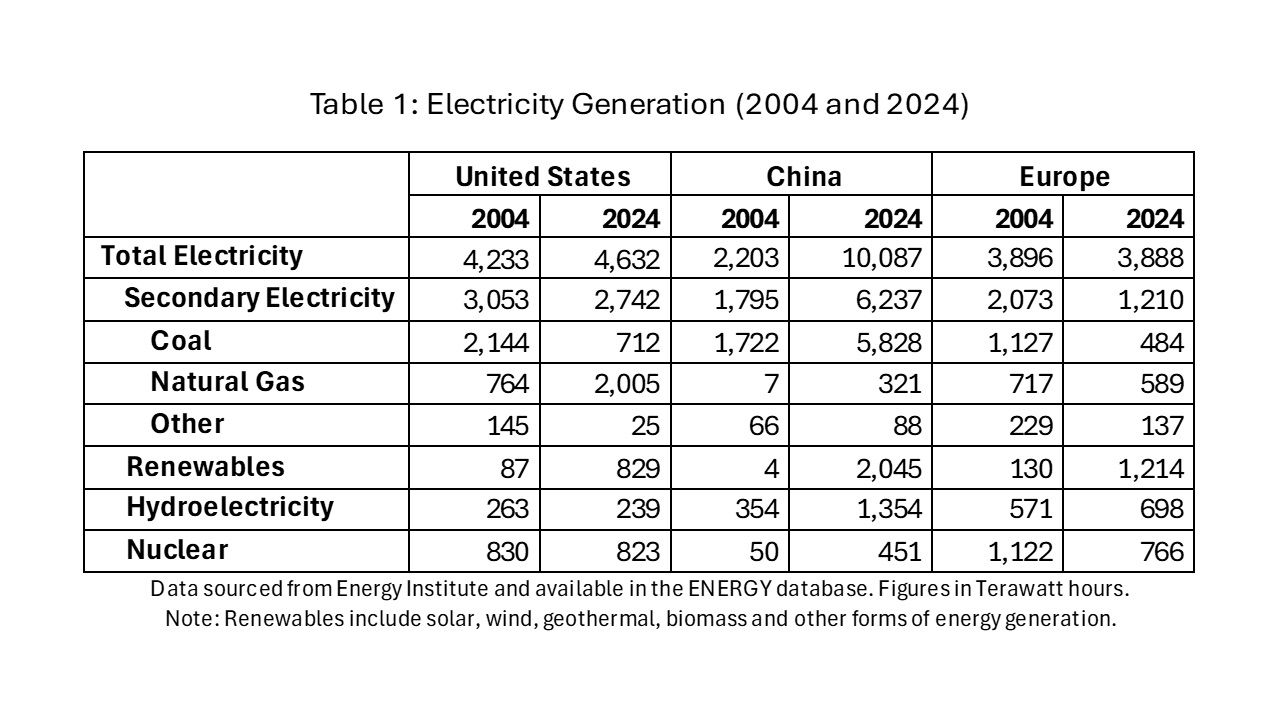

Specifically, we compare the forms of electricity generation across the three major players in the AI race – the United States, China, and Europe. This comparison shows the stark differences in total power needs as well as the contrasting compositions of power generation. These compositions reflect both physical capacities and societal goals across the three major economies.

United States The most striking change in total US electricity over the past two decades has been the shift in fuels for secondary electricity generation from coal to natural gas. Coal use has collapsed from 2,144 TWh in 2004 to 712 TWh in 2024, while natural gas use has surged from 764 TWh to 2,005 TWh. There also has been a notable increase in renewables, which have gone from just 87 TWh to 829 TWh. Other sources of electricity – hydroelectricity and nuclear – have not really changed much in the past 20 years. Total electricity generation has seen a slight increase from 4,233 TWh to 4,632 TWh.

Given the enormous energy demands of AI, Cates reports that this total is set to rise by about 500 TWh in the next five years. President Trump recently released “Winning the Race – America’s AI Action Plan” on the Whitehouse website. It has three pillars: Accelerate AI innovation, Build American AI Infrastructure, and Lead in International AI Diplomacy and Security. The second pillar explicitly states that American energy capacity has stagnated since the 1970s and stresses the dire need to develop a power grid that matches the pace of AI innovation.

So, what form of energy could the US increase rapidly to power AI? The US has capacity to increase its electricity production very quickly using natural gas and coal. Given the climate in Washington and the need for more energy, we may very well see a significant reversal in the downward trend in coal and a pickup in the usage of natural gas. We are unlikely to see a surge of renewables and nuclear power.

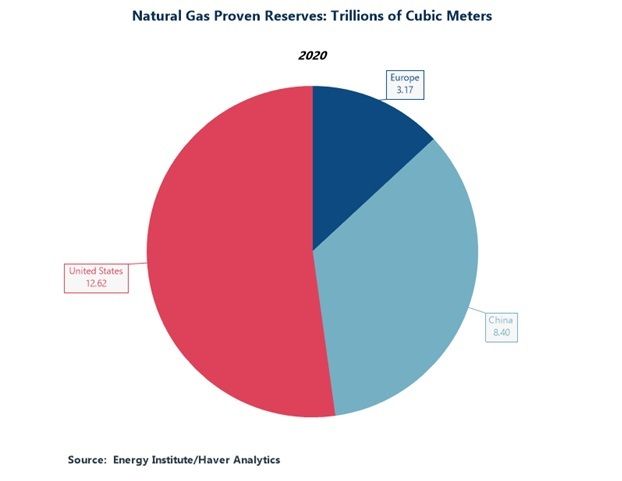

In terms of capacity, the US has tremendous natural gas and coal reserves. As of 2020, the US had 12.62 Trillion Cubic Meters of natural gas proven reserves, which is slightly more than China and Europe combined (see figure below).

China Over the past 20 years, China has ramped up its electricity production to more than the US and Europe combined. Total electricity generation has increased from 2,203 TWh in 2004 to 10,087 TWh in 2024, or 358%. Coal accounts for the lion’s share of electricity generation, and has been the main source of growth, skyrocketing from 1,722 TWh in 2004 to 5,828 TWh in 2024. China has been building up its ability to produce clean or renewable energy as well, but the increases have been nowhere near sufficient to meet the rise in its needs. In the past decade, hydroelectricity has steadily risen from 354 TWh to 1,354 TWh and renewable energy generation has jumped from 4 TWh to 2,045 TWh. Natural gas and nuclear energy have accounted for a growing but minor share of the total.

As the Chinese economy continues to grow, the rise in energy needs shows no sign of abating. As such, China’s latest Five-Year Plan calls for the building of 150 new nuclear reactors over the next decade with the goal of generating about 150GW of additional nuclear energy by 2035. Based on the IRENA dataset in ENERGY, we estimate that this could add nearly 1,500TWh of electricity. However, a near-term jump in additional electricity needs due to AI would likely add to the Chinese electricity need and have to be satisfied by more coal generation.

Europe Europe has been shifting away from fossil fuel electricity generation and toward renewables for the past two decades. Renewable energy is now the biggest electricity generation sector in Europe and is rising rapidly. It went from 130 TWh in 2004 to 1,214 TWh in 2024, offsetting declines in coal and nuclear energy. Coal has fallen from 1,127 TWh to 484 TWh, and nuclear energy has drifted down from 1,122 TWh to 766 TWh. Other sectors (hydroelectricity and natural gas) have drifted sideways. Total electricity generation is essentially unchanged.

Given the cultural and political will to reduce fossil-fuel emissions, Europe would probably redouble its efforts to expand its carbon-neutral energy generation to satisfy its additional AI power needs. However, the reality is investment in renewables takes time. In the near term, Europe would have no choice but to increase its electricity generation from fossil fuels or risk falling behind in the AI race.

Conclusion Based on our analysis of current power generation and capacities, we believe that the United States, China, and Europe will face a dilemma: either meet their carbon reduction goals by producing less energy from fossil fuels or meet their AI goals by burning more fossil fuels. We believe the AI race could reverse much of the environmental gains made in the past two decades and could have deleterious consequences for global warming.

Shashwat Indeevar

AuthorMore in Author Profile »Shashwat Indeevar is a Senior Economic Data Manager at Haver Analytics, where he has been part of the Research Team since 2017, working in both the New York and London offices. He focuses on the organization and presentation of large-scale datasets, the improvement of database-building processes, and the management of daily workflow. His economic research interests include global energy use, environmental sustainability, and artificial intelligence.

He holds a Master of Science in Management of Technology from New York University, where he studied finance, economics, and operations management. He also earned a Bachelor of Engineering in Electronics and Communications from Panjab University, India.

Peter D'Antonio

AuthorMore in Author Profile »Peter started working for Haver Analytics in 2016. He worked for nearly 30 years as an Economist on Wall Street, most recently as the Head of US Economic Forecasting at Citigroup, where he advised the trading and sales businesses in the Capital Markets. He built an extensive Excel system, which he used to forecast all major high-frequency statistics and a longer-term macroeconomic outlook. Peter also advised key clients, including hedge funds, pension funds, asset managers, Fortune 500 corporations, governments, and central banks, on US economic developments and markets. He wrote over 1,000 articles for Citigroup publications. In recent years, Peter shifted his career focus to teaching. He teaches Economics and Business at the Molloy College School of Business in Rockville Centre, NY. He developed Molloy’s Economics Major and Minor and created many of the courses. Peter has written numerous peer-reviewed journal articles that focus on the accuracy and interpretation of economic data. He has also taught at the NYU Stern School of Business. Peter was awarded the New York Forecasters Club Forecast Prize for most accurate economic forecast in 2007, 2018, and 2020. Peter D’Antonio earned his BA in Economics from Princeton University and his MA and PhD from the University of Pennsylvania, where he specialized in Macroeconomics and Finance.