AI Lag and Investment Stagnation Cloud India’s Outlook

|in:Viewpoints

India remains an equity overweight, but the shine has faded from both its cyclical recovery and its structural growth story. Two issues stand out: the country is lagging badly in the AI revolution, and the corporate investment cycle—despite strong macro conditions—has failed to ignite.

AI: A Race India Is Not Winning

India has attracted several high-profile announcements. Google plans to invest US$15bn over five years to build an AI data centre. Microsoft has committed US$3bn over two years, Amazon US$12.7bn by 2030, and the government’s latest budget allocates US$1.25bn to develop the domestic AI ecosystem.

On paper, this sounds substantial. In reality, it pales next to the intensity of global AI investment. The big four US hyperscalers—Amazon, Microsoft, Google and Meta—are currently spending around US$90bn per quarter on AI. Even compared to peers like China, the gap is stark. Over the past decade, state-backed venture capital in China has channelled roughly US$912bn into strategic industries including AI. China now hosts over 4,500 AI enterprises, accounts for 45% of global computing power, filed 60% of AI patents in 2024, and is expected to invest US$85–98bn in AI capex in 2025 alone.

India’s GenAI Landscape: Growing, but Too Slowly

The domestic AI start-up ecosystem is expanding. As of 1H25, India hosts more than 890 generative AI start-ups, up from 240 a year earlier, with cumulative funding of US$900m. The funding mix, however, shows a narrow focus: 88% into AI infrastructure, 8% into services and only 4% into applications. Karnataka dominates with 39% of AI start-ups, followed by Maharashtra (14%), Delhi (9%) and Telangana (7%).

India’s AI market is forecast to grow at a 25–35% CAGR, reaching roughly US$17bn by 2027. NASSCOM, the industry body for the tech sector, estimates data and AI could contribute US$450–500bn to GDP by 2025––approximately 10% of the country’s original US$5trn target.

But scaling remains slow relative to the global frontier. India’s AI spending is small, investor appetite is weak, and the ecosystem faces structural barriers.

The Challenges

1. Lack of Regulatory Clarity Policy uncertainty has deterred funding, especially for deep-tech. Capital inflows remain limited, forcing start-ups to operate under severe funding constraints. Although 25+ new GenAI firms launched last year, both seed and late-stage investment have contracted sharply.

2. Talent Is Scarce Demand far exceeds supply. NASSCOM estimates India suffers one of the world’s highest AI talent shortages—around 50%. With insufficient advanced training capacity, scaling becomes difficult.

3. Government Response Is Reactive Thus far, policy has focused on short-term fixes and pilot initiatives. What is missing is a coordinated long-term strategy. According to NASSCOM, India needs large-scale public–private co-investment to de-risk innovation. But resistance to policy change and bureaucratic inertia remain barriers.

India is positioned to participate in the AI economy, but not to lead it. And without leadership or scale, the structural growth narrative weakens.

The Business Cycle: Why Hasn’t Investment Turned?

The second problem is more puzzling. India’s corporate investment cycle should be rising strongly, given macro conditions. Instead, it remains in a downtrend—even before pandemic disruptions and well before Trump’s 50% tariff shock.

The Good News

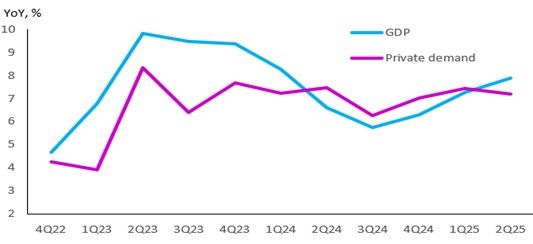

Growth momentum is solid. GDP has accelerated since 4Q24, powered largely by private demand—especially consumption in 2Q25 (Figure 1). The economy expanded 7.6% YoY on average in 1H25, outperforming regional peers and handily beating China.

Figure 1: India GDP and private demand, real

Source: Haver Analytics & Westbourne Research

Corporate fundamentals are also sound. Profits remain strong, balance sheets are healthy, and both households and companies remain significantly underleveraged and cash-rich.

CRISIL Ratings—tracking 7,300 companies—reported 499 upgrades vs 230 downgrades in the first half of FY2026. The upgrade rate of 14% exceeds the decade-long average of 11%. Eighty percent of companies saw stable or improved ratings, reflecting broad strength across infrastructure, engineering, capital goods, construction, renewables, and steel. Export-oriented firms drove most downgrades.

Drivers of strength are clear: • 54% of upgrades were driven by revenue growth • 10%—primarily in construction—were due to robust order books • FY2026 median revenue growth is projected at 8% • EBITDA margins holding near 12% • Gearing declining; interest coverage improving to 5.3x

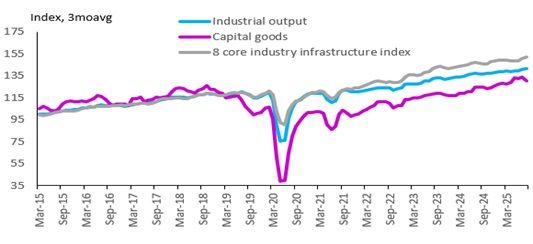

Industrial production is recovering, capital goods output is rising, and the eight-core infrastructure index (cement, steel, energy, fertilisers, electricity etc.) continues to climb (Figure 2).

Figure 2: Industrial, capital and core infrastructure sectors output

Source: Haver Analytics & Westbourne Research

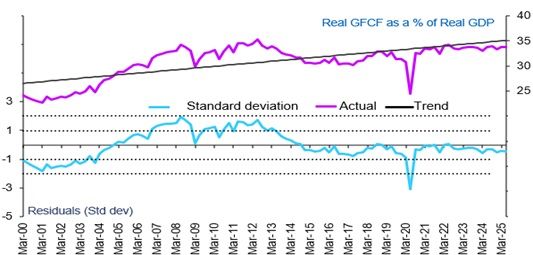

Yet Investment Isn’t Responding

Despite strong demand, profitability, cash reserves and balance sheets, the investment cycle remains in a downswing (Figure 3). This is the biggest drag on the India story.

Figure 3: India investment cycle

Source: Haver Analytics & Westbourne Research

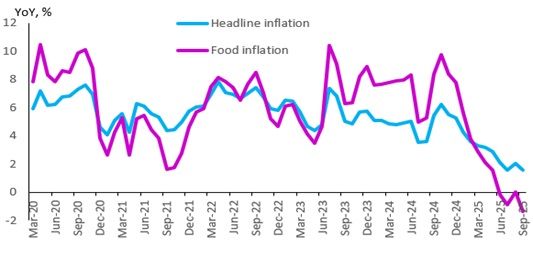

By contrast, the consumption outlook looks robust. Credit growth is picking up as monetary conditions ease. Inflation has cooled sharply, especially food inflation, giving a lift to rural purchasing power. We expect the RBI may cut another 25bps this year. GST rate cuts—from 12% and 28% down to 5% and 18%—offer additional support to consumption and discretionary demand.

Figure 4: Headline consumer and food prices should lend additional support

Source: Haver Analytics & Westbourne Research

The Trump Shock

And that brings us to the final issue — the 50% import duty Trump has slapped on Indian exports and the restrictions on H-1B visas.

On H-1B visas, the impact looks limited. Restrictions apply mainly to new hires, not existing workers. But many Indian IT firms were already localising US hiring and increasingly executing work remotely. Indians on H-1B visas now account for only 3–5% of US tech workforces.

India is also not heavily reliant on remittances. Inflows stood at 3.5% of GDP in 2024, stable within a 2.7–3.6% range for a decade. By comparison, the Philippines records 8–10% of GDP in remittances. Paradoxically, tighter US visas could even help: some highly trained AI and IT graduates may return, easing India’s talent shortage.

On tariffs, the headline number looks worrying, but the macro effect is small. Exports comprise only 12% of GDP—and exports to the US account for just 2.2%. The affected industries are labour-intensive, but second-round effects on employment and consumption should be contained. Export-sector employment—about 60 million people—is small relative to India’s one-billion-plus consuming population. Meanwhile, GST cuts likely provide a net boost to domestic demand that outweighs the drag from tariffs.

Conclusion: Where to Invest?

Under Prime Minister Modi, India has delivered significant structural reforms: liberalising FDI, streamlining regulation and launching production-linked incentives to draw private capital. Yet the country remains far behind in AI and other next-generation industries. Without meaningful acceleration in innovation investment, India risks being a fast-growing follower rather than a global leader.

The corporate investment drought is the bigger and more immediate concern. Without a turn in the capex cycle, India’s growth stays capped near 6.5–7%, and the business-cycle recovery will remain gradual rather than powerful.

For now, equity positioning remains constructive. The bias favours consumer discretionary, banks, selective technology and real estate.

Sharmila Whelan

AuthorMore in Author Profile »The founder of Westbourne Research (www.westbourne-research.com), Sharmila Whelan is a seasoned Global Geopolitical-Macro Strategist with nearly three decades of experience advising buy-side clients on multi-asset investment strategies and asset allocations. Her career has been defined by her differentiated thinking, a deep understanding of the intricate connections between global geopolitics, macro and policy dynamics, and the Austrian business cycle approach to economic analysis. She has counseled governmental bodies such as the CIA, the US State Department, the British High Commission, DFID, and China’s NDRC.

Sharmila has held prominent roles in both London and Hong Kong, serving as Managing Director at Aletheia Capital, Director at Merrill Lynch Bank of America, Senior Economist at CLSA, and Asia Regional Economist at BP Plc. In 2022, Bloomberg recognised her as one of the UK's "12 New Expert Voices." She is a frequent media commentator on Bloomberg TV and radio, BBC World Business News, and CNBC, and is a sought-after speaker at high-profile events such as the Financial Times Wealth Summit and CFA UK & India conferences. Sharmila also contributes opinion pieces to Financial Times Professional Wealth Management and the Economist Group’s EIU.