A Dodgy CPI-Shelter Reading for November?

by:Joel Prakken

|in:Viewpoints

On December 18 the Bureau of Labor Statistics (BLS) released the Consumer Price Index (CPI) for November. In October, when the federal government was partially shut down, BLS did not conduct its survey of prices, leaving most of them unrecorded for that month. Therefore, rather than reporting the usual 1-month percent changes in prices for November, BLS reported 2-month percent changes instead. For example, from September to November, the core CPI advanced at a 1% annualized rate – a surprisingly benign reading that, if accurate, significantly improves the current narrative on inflation and strengthens the case for easier monetary policy.

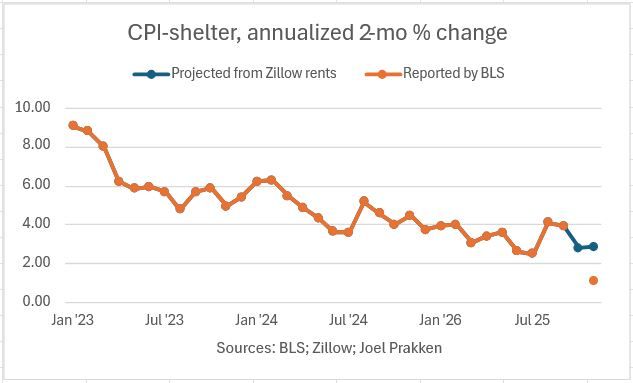

Unfortunately, the potential impact of the shutdown on both the quality and timing of the November survey raises legitimate concerns about the reliability of its results. One particularly dodgy-looking element of the report was a quite sharp deceleration in the CPI for shelter, the 2-month annualized percent change of which dropped from 3.9% in September to just 1.1% in November (gold line in chart). An erroneous reading here could be of considerable importance given that shelter costs comprise nearly 18% of “core” personal consumption expenditures.

The CPI-shelter reflects rents on tenant- and owner-occupied housing units. Imputed rents on owner-occupied units are inferred from observed rents on nearby comparable tenant-occupied units. Because shelter costs reflect average rents, they are highly inertial, lagging well behind current (i.e., marginal) market conditions for two reasons. First, rental contracts typically are for one year, requiring twelve months for all contracts to reflect a change in market conditions. Second, the BLS rotates through a panel of renters over a period of six months, adding another half year to the lag between marginal and average rents.

However, these lags allow one empirically to relate the CPI-shelter to current and past new rental contracts. I did so by estimating a model that explains the CPI-shelter with current and lagged values of Zillow indices of observed newly contracted rents. These indices are available monthly through November. I then used that model to forecast the shelter costs for the months of October and November. The resulting projection of the 2-month change in the CPI-shelter is shown in the blue line in the chart.

The model suggests that from September through November the CPI-shelter grew at an annualized rate of 2.9%, 1.8 percentage points faster than the number published by BLS. To me, the projection seems more believable than the reported figure. Replacing the latter with the former raises the 2-month annualized change in the core CPI by approximately 0.3 percentage points, to 1.3% - still a good reading, but not as good. And, of course, all this makes one wonder about the reliability of estimates of other prices in the report. So, before concluding prematurely that inflation is quiescent, it makes sense for one to await additional months of readings.

Joel Prakken

AuthorMore in Author Profile »Joel Prakken is former Chief US Economist of S&P Global and IHS Markit, co-founder of Macroeconomic Advisers, and past president and director of the National Association for Business Economics. He has served as an outside advisor to the Congressional Budget Office, on the Advisory Panel of the Bureau of Economic Analysis, and as a consultant to the Joint Committee on Taxation. He holds a BA in economics from Princeton University and a PhD in economics from Washington University in Saint Louis.