Global| Jan 29 2026

Global| Jan 29 2026Are We In An AI Bubble?

by:Andrew Cates

|in:Viewpoints

Excess, innovation and why this boom may still have room to run

Recent weeks have seen financial markets gripped by a shifting mix of narratives. A weaker US dollar, rising rate volatility and renewed geopolitical uncertainty have revived talk of a tentative “sell America” trade, as investors reassess US exceptionalism after several years of outperformance. At the same time, global equity markets have remained remarkably resilient, supported in large part by continued optimism around artificial intelligence and the powerful investment cycle it has unleashed.

Against this unsettled backdrop, a familiar question has returned to the centre of market debate: are prices being driven by fundamentals, or by faith? With artificial intelligence, that conversation has clearly arrived. Equity markets — particularly in the United States — have surged on the back of a relatively small group of AI-exposed firms that now account for a striking share of index gains. Valuations increasingly rest on the assumption that AI will deliver a sustained uplift to productivity, profits and long-run growth. Investors are no longer debating whether AI will transform the economy; instead, they are debating how quickly — and how completely — those gains will materialise.

Lessons From History

History offers a useful starting point. Truly transformative technologies almost always arrive alongside periods of financial excess. Railroads, electricity, telecoms and the internet all produced extraordinary investment booms that ultimately reshaped economic structures, even as they destroyed large amounts of capital along the way. The presence of a bubble never meant the technology was flawed. It meant expectations moved faster than cash flows, infrastructure deployment and balance-sheet reality. AI fits this historical pattern uncomfortably well.

In this environment, narrative often dominates near-term profitability, and that is typically how transformative technologies diffuse rapidly across the economy. But where bubbles become truly dangerous is not via investor enthusiasm itself, but in the financing structures that accompany large infrastructure build-outs. Equity investment in diversified firms with strong balance sheets is fundamentally different from debt-financed bets on long-lived assets whose viability depends on uncertain demand and rapidly evolving technology. Yet we are already seeing significant capital being channelled into data centres, energy infrastructure and specialised AI facilities, increasingly funded through project-level vehicles and long-dated financing. These investments rest on assumptions about sustained utilisation, manageable energy costs and technological continuity — assumptions that inevitably carry risk.

This should feel familiar. The late-1990s telecoms boom was not undone because fibre optics were useless, but because capacity was financed almost entirely with leverage long before revenues caught up. When pricing power collapsed, investors absorbed enormous losses, even as the infrastructure went on to support the digital economy that followed.

The Macro Dimension

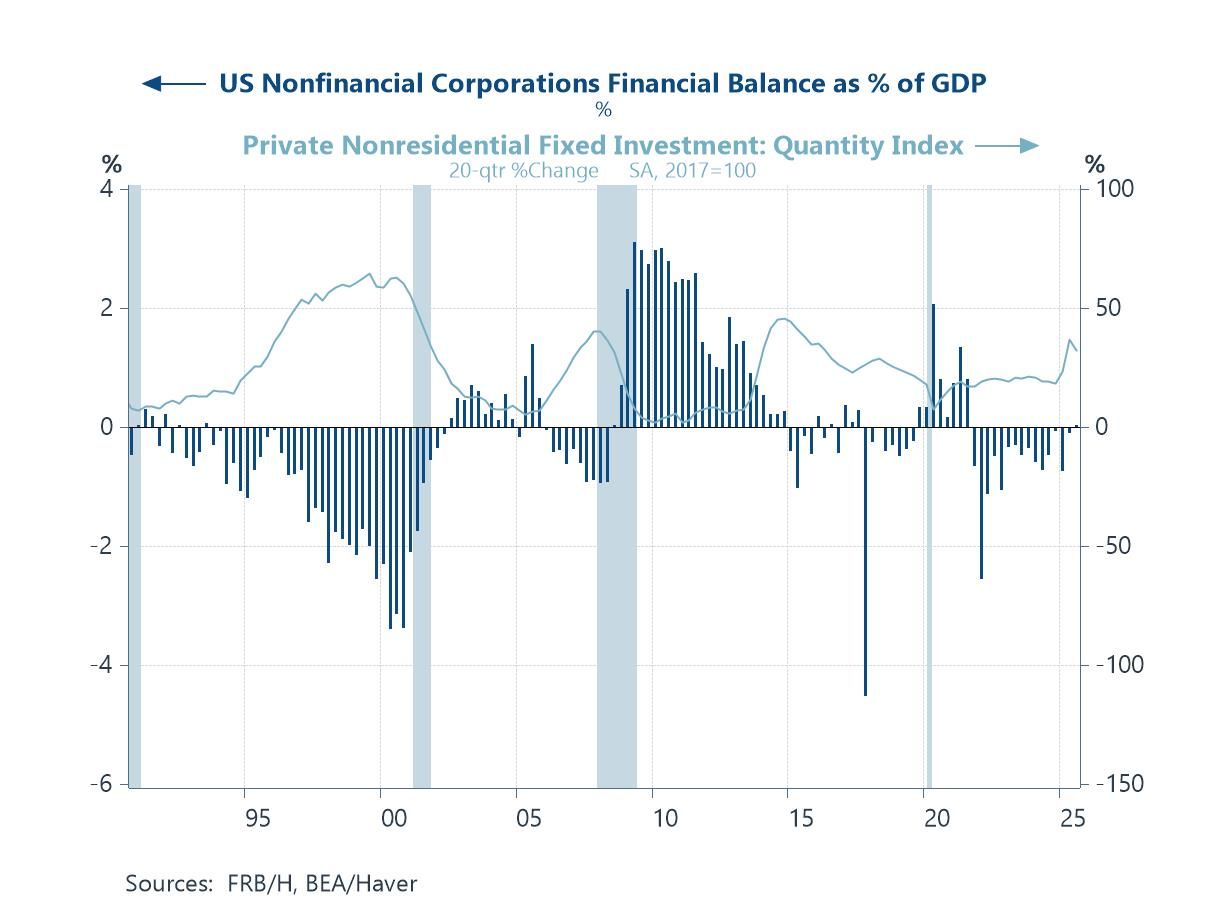

However, there is also a macro dimension in this debate that deserves more attention, and this is where today’s AI boom still looks somewhat different from past excesses. The chart below contrasts private non-residential investment in the US with the financial balance of non-financial corporations. During the dot-com era, corporate investment surged at the same time as the corporate sector moved deep into financial deficit. Firms were spending far beyond internal cash flows, and increasingly reliant on external financing — particularly debt — to fund speculative expansion. That combination of soaring investment and widening financial imbalances was a classic Minsky-style warning sign.

Today’s picture looks more restrained. Investment in advanced technology and AI-related infrastructure has risen meaningfully, but it has not been accompanied by anything like the same degree of system-wide corporate dissaving. Corporate financial balances, as of Q3 2025, remain much closer to neutral, reflecting strong cash flows at large firms funding much of the investment internally. This does not mean risk is absent. Pockets of debt-financed AI infrastructure are clearly expanding and deserve close scrutiny. But at the aggregate level, the US economy does not yet exhibit the hallmark of bubble periods that morph into systemic crises: widespread leverage-driven overinvestment.

That healthier balance-sheet backdrop suggests that even if parts of the AI ecosystem experience sharp valuation corrections, the macroeconomic aftershocks may be more manageable than in previous technology busts. Historically, bubbles become crises not simply because some investments fail, but because leverage transforms losses into economy-wide financial stress.

So are we in an AI bubble? Almost certainly in parts of the ecosystem. Expectations are lofty, narratives are powerful and capital is flowing rapidly. But history also suggests that bubbles around transformative technologies often inflate for longer — and go further — than many of the sceptics expect.

Andrew Cates

AuthorMore in Author Profile »Andy Cates joined Haver Analytics as a Senior Economist in 2020. Andy has more than 25 years of experience forecasting the global economic outlook and in assessing the implications for policy settings and financial markets. He has held various senior positions in London in a number of Investment Banks including as Head of Developed Markets Economics at Nomura and as Chief Eurozone Economist at RBS. These followed a spell of 21 years as Senior International Economist at UBS, 5 of which were spent in Singapore. Prior to his time in financial services Andy was a UK economist at HM Treasury in London holding positions in the domestic forecasting and macroeconomic modelling units. He has a BA in Economics from the University of York and an MSc in Economics and Econometrics from the University of Southampton.