From Foundries to Fortunes: Taiwan in the AI Era

|in:Viewpoints

Taiwan stands to benefit disproportionately from the current AI-led global semiconductor upcycle. Its domestic semiconductor ecosystem has expanded at remarkable speed, more than tripling over the past decade—from about US$69bn in 2014 to US$166bn in 2024—and is estimated to approach US$200bn in 2025. This growth is no accident. Taiwan sits at the heart of the world’s most advanced logic-chip production, with demand increasingly driven by AI and high-performance computing. Its dominance reflects early specialisation, rapid scaling, and an unmatched ability to protect customers’ intellectual property.

At the centre of this ecosystem is TSMC—Taiwan’s true national treasure—which continues to consolidate its lead at the technological frontier. While near-shoring projects in Japan, Germany and the US are often framed as diversification, in practice they reinforce Taiwan’s position rather than weaken it. TSMC’s latest commitment to build five additional fabs in Arizona illustrates this point clearly. Leading-edge R&D, pilot runs and sub-7nm process know-how remain anchored on the island. Overseas fabs are best understood as extensions of Taiwan’s production model, not substitutes for it.

The foundry race is no longer about sheer scale but about leadership at the cutting edge—and that leadership still belongs to Taiwan. A November 2025 report noted that Nvidia sources 100% of its top-tier GPUs from TSMC, including advanced 3nm and emerging 2nm-class production. AI and high-performance computing now account for more than half of TSMC’s wafer revenue, with AI processors alone on track to reach around 20% of sales by 2028.

Taiwan’s strength is not limited to foundries. Its fabless sector benefits from unusually tight coupling with domestic manufacturers, rapid design-to-manufacturing feedback loops, and a dense ecosystem in which suppliers, advanced packaging, talent and fabs are co-located. This structure enables faster iteration and innovation than is possible in more geographically fragmented semiconductor hubs.

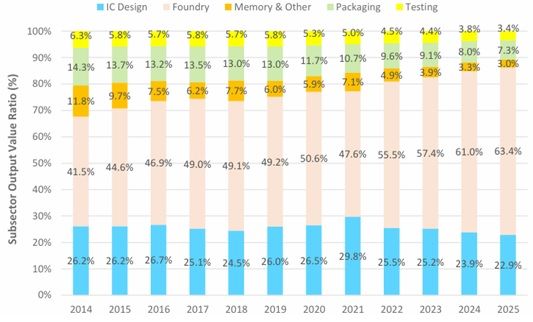

That said, the industry has become increasingly concentrated, and this brings risks (Figure 1). The foundry sector’s share of output has risen from 41.5% in 2014 to an estimated 63.4% in 2025. By contrast, other subsectors—IC design, packaging, testing and related activities—have seen their shares decline. The memory segment has shrunk particularly sharply, from 11.8% of output in 2014 to just 3% in 2025, leaving Taiwan heavily dependent on Korea in this area. IC packaging’s share has also roughly halved to around 7%.

Figure 1: Taiwan semiconductor industry structural share trend

Source: Taiwan & The Global Semiconductor Supply Chain, Taipei Representative Office, Singapore

Additional vulnerabilities include reliance on foreign chip designs and imported manufacturing tools, as well as geographic concentration that increases exposure to natural disasters and geopolitics. Still, Taiwan’s cost competitiveness remains a decisive advantage. Even with subsidies, mature-node fabs in the US cost roughly 10% more to build and up to 35% more to operate than those in Taiwan, while Europe faces energy costs roughly double those of the US. Mainland China enjoys lower costs but lacks access to leading-edge technology. Taken together, these dynamics explain why Taiwan remains indispensable to the global semiconductor industry—and why it stands to benefit most from the AI-driven investment surge now underway.

Taiwan’s economy and the business cycle

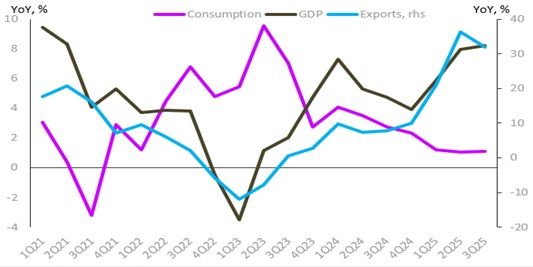

What always strikes us is how closely synchronised Taiwan’s business cycle remains with its export cycle—something unusual for a mature, ageing economy that, according to standard economic theory, should by now be a dissaving society (Figure2). But this apparent anomaly speaks to a core Austrian insight, borne out repeatedly by history: growth is fundamentally endogenous, not exogenous.

Figure 2: Taiwan GDP and components

Source: Haver Analytics & Westbourne Research

Exogenous growth models emphasise demographics, capital accumulation and productivity gains, and predict diminishing returns as economies mature and workforces age. Endogenous growth theories instead stress innovation and specialisation. These reduce production costs, expand markets, enable firms to scale, and foster the emergence of new technologies, industrial clusters and ecosystems—ultimately generating increasing returns. History is full of small countries with limited populations that became economic powerhouses by following this path. Taiwan is simply another example.

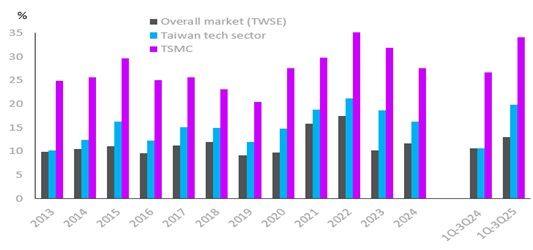

Turning to the data, Taiwan ranks at the top of the latest business-cycle indicator assessment. Four of the five indicators are positive; the only negative signal is the cost of capital, which remains too low for the current phase of the cycle. As in the US and Japan, Taiwan’s corporate profit upcycle strengthened through last year. Average returns on equity for the overall market, the technology sector and TSMC are all above their pre-Covid seven-year averages (Figure 3).

Figure 3: Taiwan average return on equity

Source: Bloomberg & Westbourne Research

Ideally, it would be useful to examine an ex-tech returns series to gauge the health of the broader corporate sector, but such data are unavailable. In any case, the question may be beside the point. For investors, Taiwan is fundamentally a technology play. It is not about domestically focused stocks—at least not until the economy enters a full boom phase in which investment, construction and consumption all grow well above trend, supported by rising incomes and credit expansion.

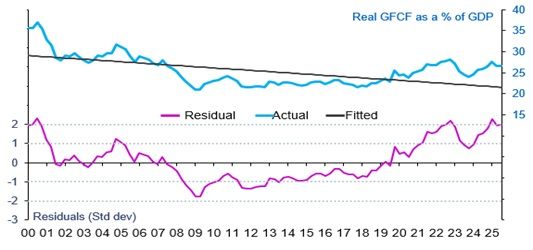

Rising profitability in the technology sector is already driving a renewed investment upswing (Figure 4). The integrated-circuit sector alone accounts for roughly 20% of GDP, underscoring its macroeconomic importance. In 2024, Taiwan’s semiconductor industry generated around US$165bn in output, equivalent to approximately 21% of GDP.

Figure 4: Taiwan investment cycle

Source: Haver Analytics & Westbourne Research

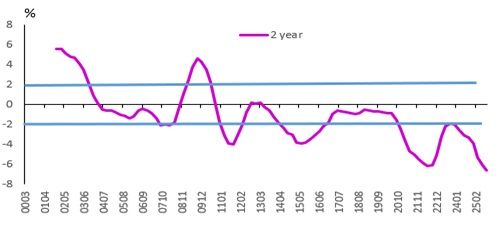

Monetary conditions remain extremely supportive. The two-year real lending rate, at around minus 6.6%, is not only well below the 2% lower threshold but also the lowest in Asia. This is a concern—but not yet a critical one. The credit cycle remains subdued, suggesting that artificially low interest rates are neither encouraging firms to borrow aggressively for long-gestation projects nor pushing households into excessive debt. That said, the central bank is clearly behind the tightening curve, even if inflation remains steady at around 1.6% year-on-year (Figure 5).

Figure 5: Taiwan two-year real lending rate

Source: Haver Analytics & Westbourne Research

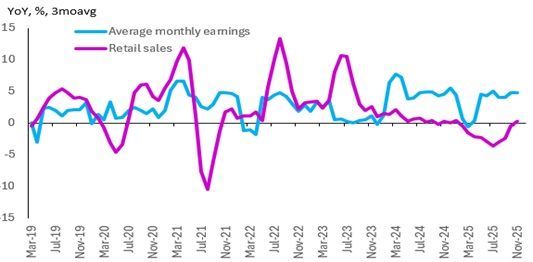

Business-cycle indicators point to continued strength, a view reinforced by high-frequency data. Exports, export orders and manufacturing activity are all trending higher (Figure 6). Consumption is also reviving as the tech-led investment upswing spills over into the broader economy, tightening labour markets and lifting wage growth (Figure 7). In short, the outlook for the year ahead is bright. Growth should accelerate, and the business cycle is likely to broaden beyond investment to consumption.

Figure 6: Exports and orders

Source: Haver Analytics & Westbourne Research

Figure 7: Average monthly earnings and retail sales

Source: Haver Analytics & Westbourne Research

Where to invest?

That Taiwan’s equity market would outperform the region in 2024 and perform strongly again in 2025 has been one of our best calls. We continue to maintain an overweight position in equities this year, particularly in the technology sector—and is certainly holding onto her TSMC shares.

As always, we remain focused on business-cycle fundamentals, which for Taiwan remain firmly positive. Taiwan is also a central beneficiary of the global semiconductor upcycle and the AI-driven “Sixth Wave” discussed last week. Risks remain—not least US import tariffs under a possible Trump administration—but the US and Taiwan appear to be edging toward a deal that would reduce tariffs from 20% to around 15%, in line with Korea and Japan.

Pressure on Taiwanese technology firms to invest in the US should be seen as enhancing rather than undermining the industry’s global position. It expands markets, diversifies investment, and reduces geopolitics-related operational risk. Taiwan Inc clearly understands this. Companies are already diversifying away from China in favour of other markets—a sensible strategy when put into perspective. In 2024, over 55% of Taiwan’s foreign direct investment assets were still located in China, compared with just 9% in the US, according to IMF data.

Sharmila Whelan

AuthorMore in Author Profile »The founder of Westbourne Research (www.westbourne-research.com), Sharmila Whelan is a seasoned Global Geopolitical-Macro Strategist with nearly three decades of experience advising buy-side clients on multi-asset investment strategies and asset allocations. Her career has been defined by her differentiated thinking, a deep understanding of the intricate connections between global geopolitics, macro and policy dynamics, and the Austrian business cycle approach to economic analysis. She has counseled governmental bodies such as the CIA, the US State Department, the British High Commission, DFID, and China’s NDRC.

Sharmila has held prominent roles in both London and Hong Kong, serving as Managing Director at Aletheia Capital, Director at Merrill Lynch Bank of America, Senior Economist at CLSA, and Asia Regional Economist at BP Plc. In 2022, Bloomberg recognised her as one of the UK's "12 New Expert Voices." She is a frequent media commentator on Bloomberg TV and radio, BBC World Business News, and CNBC, and is a sought-after speaker at high-profile events such as the Financial Times Wealth Summit and CFA UK & India conferences. Sharmila also contributes opinion pieces to Financial Times Professional Wealth Management and the Economist Group’s EIU.