Korea Holds Back—but Builds Strength

|in:Viewpoints

We have been overweight Korean equities this year—and it has paid off, handsomely. The allocation decision was anchored in the business-cycle framework: three of five key indicators pointed clearly toward expansion at the start of the year. The cost of capital was supportive, the credit cycle was in a firm upswing, and money-supply growth was accelerating. The corporate profit cycle, though still technically in downturn, was already showing improvement thanks to strong balance sheets. The major drag was the investment cycle, which continued to lag.

What has surprised us is the speed of the profit-cycle recovery, especially against the year’s backdrop. From Trump’s tariff war to domestic political turbulence following the impeachment of President Yoon Suk-yeol and the snap elections in June, one would have expected a more cautious rebound. Instead, the listed sector delivered a solid performance. Return on equity averaged 7% in the first three quarters, up from 5.6% a year earlier and nearly back to the seven-year average of 7.3%. EBITDA cash flow per share, free cash flow per share, and retained earnings all advanced. EBITDA rose almost 20% year-on-year, cash flow per share climbed 29%, and free cash flow per share swung decisively into positive territory.

Central-bank data paint a similarly encouraging picture. Profitability and interest-coverage ratios have improved markedly for large corporates, even as debt-to-capital ratios inched higher. SMEs have seen some deterioration, but the stress is neither systemic nor alarming at this stage.

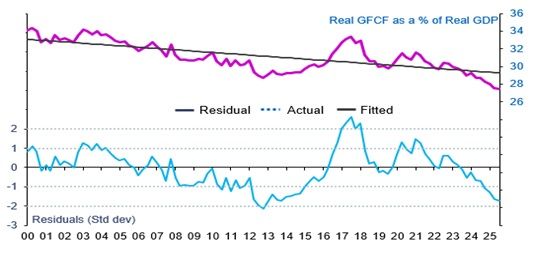

And yet, despite these solid fundamentals, Korea Inc has continued to err on the side of caution (Figure 1). Companies tightened spending this year and delayed new investment plans. As a result, the investment cycle slid deeper into downturn: real spending on both facilities and construction has contracted for six consecutive quarters. Rather than expand capacity, firms have chosen to run down inventories and utilise existing manufacturing facilities more intensively. Operating rates have increased, allowing companies to meet rising shipments without committing fresh capital.

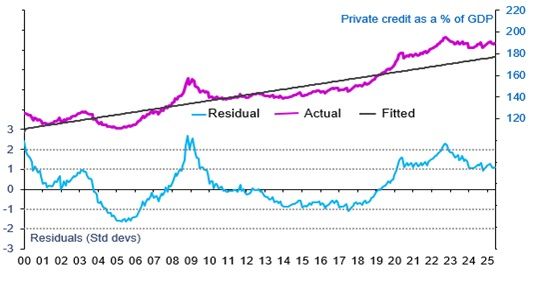

Figure 1: Korea investment cycle

Source: Haver Analytics and Westbourne Research

Weathering Trump’s Tariff War

Korean exporters have navigated the tariff conflict more effectively than many anticipated. President Lee Jae-myung secured relatively favourable terms in negotiations with the US compared with Japan or Europe. Tariffs on Korean car imports will fall from 25% to 15%. Korea will still invest US$350bn in the US—US$200bn in cash and US$150bn via a shipbuilding partnership—but annual outflows are now capped, and profits will be shared until the initial investment is recouped. This represents a meaningful improvement from the earlier agreement, which allocated 90% of profits to US stakeholders.

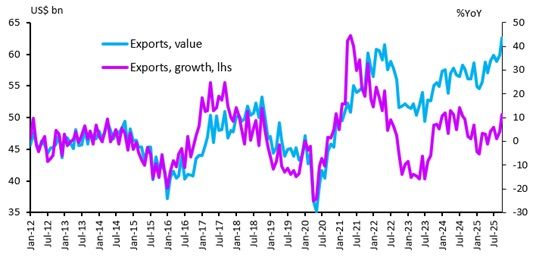

The Bank of Korea, however, remains cautious, estimating that tariffs will shave 0.45 percentage points off growth this year and 0.6 points in 2026. Inflation is expected to ease slightly. We are less convinced by the central bank’s pessimism. Export performance shows Korean firms have been resilient—more so than official forecasts imply (Figure 2).

Figure 2: Exports

Source: Haver Analytics and Westbourne Research

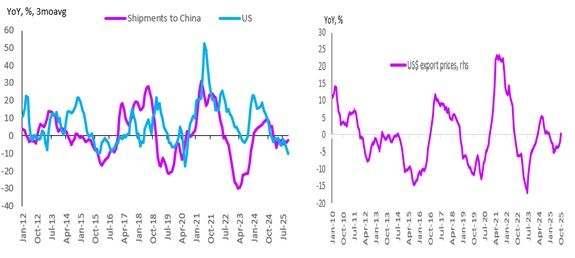

A closer look reveals why. Exports to the US have dropped sharply, and shipments to China have contracted in nine of the last ten months. Yet overall exports have continued to trend higher. Korean companies moved quickly to diversify into ASEAN and Europe, offsetting losses in traditional markets (Figure 3, Chart 1).

Moreover, exporters have again demonstrated their commercial nimbleness. Historically, Korean firms have not hesitated to discount aggressively when global demand softens, protecting market share at the cost of margins—then recoup those margins by raising prices once demand stabilises. That pattern is repeating. October marked the first month this year in which year-on-year export prices turned positive (Figure 3, Chart 2). Falling import prices and careful cost control have further strengthened profitability.

Figure 3: US & China shipments and export prices

Source: Haver Analytics and Westbourne Research

With tariff uncertainty largely behind us and the global business cycle turning upward, supported by accommodative global fiscal and monetary settings, We see the conditions forming for Korea’s investment cycle to stabilise and strengthen into next year.

Construction: Korea’s Weakest Link

If there is one clear vulnerability in the Korean economy, it is construction. The sector’s problems long predate the tariff war. Construction investment has been in a structural downturn since 2017, following tighter housing-loan regulations and a general tightening of financial conditions. A brief pandemic-era rebound—fuelled by liquidity—quickly faded as construction costs increased, interest rates rose, real-estate prices softened, and project-financing conditions deteriorated. Political uncertainty and headline-grabbing worksite accidents further delayed projects in early 2025.

Non-housing construction, which accounts for about two-thirds of investment, has been especially weak. As a mature economy, Korea has already met many major infrastructure needs. Meanwhile, commercial real estate has been oversupplied due to loose regulation in earlier years, the post-pandemic shift to online consumption, and persistent weakness in the self-employed sector. Retail vacancy rates remain high.

Regional disparities compound the issue. Seoul suffers from chronic undersupply and soaring demand, while many non-Seoul regions face weak demand and large inventories of unsold homes. Price behaviour reflects this divergence: house prices outside Seoul have fallen year-on-year since January 2023, while the Seoul market has already recovered, with November prices rising 6.7%.

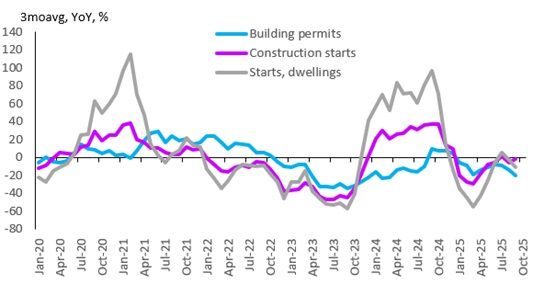

Permitting and construction-start data remain bleak (Figure 4). Yet there are glimmers of hope: the nationwide home-supply ratio has fallen sharply since its pandemic peak, and the home-ownership rate remains low at 57%. Housing sentiment has improved as mortgage rates come down and affordability increases. Still, the recovery will be slow and patchy. The government introduced new measures in June targeting the Seoul market, including tighter loan caps, restrictions on multiple-home mortgages, and reduced loan-to-value ratios for first-time buyers. Given this backdrop, we remain underweight construction, real estate, and consumer durables.

Figure 4: Building permits, construction & dwelling starts

Source: Haver Analytics and Westbourne Research

Credit Conditions, Broad Money, and the BoK

The credit cycle remains in an upswing (Figure 5), supported by household credit demand even as corporate borrowing slows. However, given the weak backdrop in construction and housing, we recommend remaining underweight banks until investment spending shows clearer signs of recovery.

Figure 5: Credit cycle

Source: Haver Analytics and Westbourne Research

Broad money growth—a key leading indicator—is accelerating at a healthy rate that supports economic activity without stoking inflation. Importantly, there are no signs of credit-cycle overheating.

The Bank of Korea has cut rates by 100 bps since last October but is expected to hold policy steady for the remainder of 2025. Despite subdued demand and lower oil prices, which should keep inflation near target, the BoK remains concerned about the won’s exchange rate and elevated household credit demand.

Real lending rates—the difference between corporate borrowing costs and nominal GDP growth—are a more relevant indicator for investment behaviour. When real rates fall below –2%, firms have strong incentives to invest aggressively; when above +2%, borrowing is discouraged. Korea’s two-year real lending rate remains comfortably within normal ranges, suggesting no structural barrier to investment once confidence returns.

Where to Invest

We maintain an overweight stance in Korean equities.

The profit cycle is nearing an upswing and has held up strongly through geopolitical turbulence. Healthy balance sheets support the view that investment will begin turning next year. Inventory-shipment dynamics and rising operating rates strengthen the argument. The credit cycle remains supportive, real lending rates are accommodative, and broad money growth is improving—implying economic growth will follow with a lag.

Sharmila Whelan

AuthorMore in Author Profile »The founder of Westbourne Research (www.westbourne-research.com), Sharmila Whelan is a seasoned Global Geopolitical-Macro Strategist with nearly three decades of experience advising buy-side clients on multi-asset investment strategies and asset allocations. Her career has been defined by her differentiated thinking, a deep understanding of the intricate connections between global geopolitics, macro and policy dynamics, and the Austrian business cycle approach to economic analysis. She has counseled governmental bodies such as the CIA, the US State Department, the British High Commission, DFID, and China’s NDRC.

Sharmila has held prominent roles in both London and Hong Kong, serving as Managing Director at Aletheia Capital, Director at Merrill Lynch Bank of America, Senior Economist at CLSA, and Asia Regional Economist at BP Plc. In 2022, Bloomberg recognised her as one of the UK's "12 New Expert Voices." She is a frequent media commentator on Bloomberg TV and radio, BBC World Business News, and CNBC, and is a sought-after speaker at high-profile events such as the Financial Times Wealth Summit and CFA UK & India conferences. Sharmila also contributes opinion pieces to Financial Times Professional Wealth Management and the Economist Group’s EIU.