The (Minimum) Cost of the Government Shutdown

by:Joel Prakken

|in:Viewpoints

After forty-two days, the longest (partial) shutdown of the federal government on record, which began October 1, is finally behind us. Forecasters have scurried to gauge the shutdown’s impact on real GDP. The exercise is not simple. With savings as a buffer, delayed income is not necessarily delayed spending. With inventories as a buffer, delayed spending is not necessarily delayed production. Some delayed spending and production can be made up later, even within the current quarter. The task is further complicated because effects of the shutdown are not identified separately in the source data compiled by the Bureau of Economic Analysis (BEA). Nor does the BEA make special adjustments to GDP for the shutdown…with one important exception.

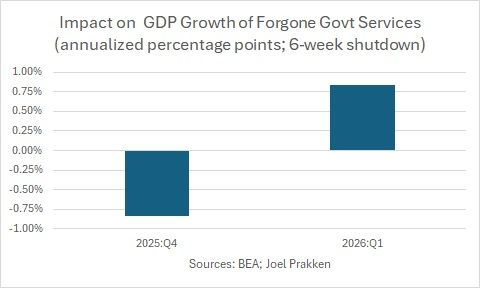

In our National Accounts services produced by government are valued at cost, the variable component of which is the compensation of government employees. The BEA treats furloughed federal workers as if their real compensation is zeroed out. This makes it straightforward to compute the real value of government services forgone during the shutdown, as well as the associated negative contribution to fourth-quarter growth of GDP. With approximately 1/3 of federal civilian workers furloughed, each extra week of the shutdown reduced the contribution of government services to fourth-quarter annualized growth of GDP by approximately 0.14 percentage point. Hence, the reduction in government services during the six-week shutdown will subtract approximately 0.8 percentage point from GDP growth in the fourth quarter.

A few caveats. This, of course, is the minimum impact, as it does not allow for the spread of effects into the private sector. And there is this subtlety. Consistent with the Government Employee Fair Treatment Act of 2019 guaranteeing furloughed federal workers their back pay, the BEA treats those workers as if their nominal compensation continued to accrue during the shutdown. Therefore, the BEA affects the appropriate reduction in real government compensation not by temporarily adjusting down the nominal pay of federal employees, but by temporarily adjusting up the deflators for government compensation. Finally, following the shutdown, government services recovered to their previous level. However, given the accounting conventions, the government services that were forgone during the shutdown will never be made up. Hence, the recovery of government services will add to first-quarter growth of GDP only the same 0.8 percentage point that their interruption subtracted from fourth-quarter growth.

It helps to put this in perspective. Currently, the Atlanta Fed’s GDPNow forecast for annualized fourth-quarter growth of GDP is 4.1%, with no allowance made for the direct impact of the shutdown on the production of government services. Making that allowance lowers the 4.1% to 3.3%. Hence, despite the shutdown, and even allowing for additional knock-on effects in the private sector, it appears the economy may record a respectable trend-like rate of growth in the fourth quarter. And, any emerging first-quarter weakness in the economy may be (partially) obfuscated by both the recovery in government services and the reversal of adverse consequences of the shutdown on activity in the private sector.

A PDF version of this commentary is available here.

Joel Prakken

AuthorMore in Author Profile »Joel Prakken is former Chief US Economist of S&P Global and IHS Markit, co-founder of Macroeconomic Advisers, and past president and director of the National Association for Business Economics. He has served as an outside advisor to the Congressional Budget Office, on the Advisory Panel of the Bureau of Economic Analysis, and as a consultant to the Joint Committee on Taxation. He holds a BA in economics from Princeton University and a PhD in economics from Washington University in Saint Louis.