Festivus 2025 – I Got a Lot of Problems with the Treasury and the Fed

|in:Viewpoints

With the passage of the One Big Beautiful Bill Act (OBBBA) of 2025, already high US federal budget deficits will rise even higher than projected by the Congressional Budget Office (CBO) at the beginning of the year. One element contributing to the rise in the deficits will be interest on the public debt. With the Treasury’s policy of shortening the maturity of the public debt and the politicization of the Fed, I fear that the US government will effectively default on its debt via inflation.

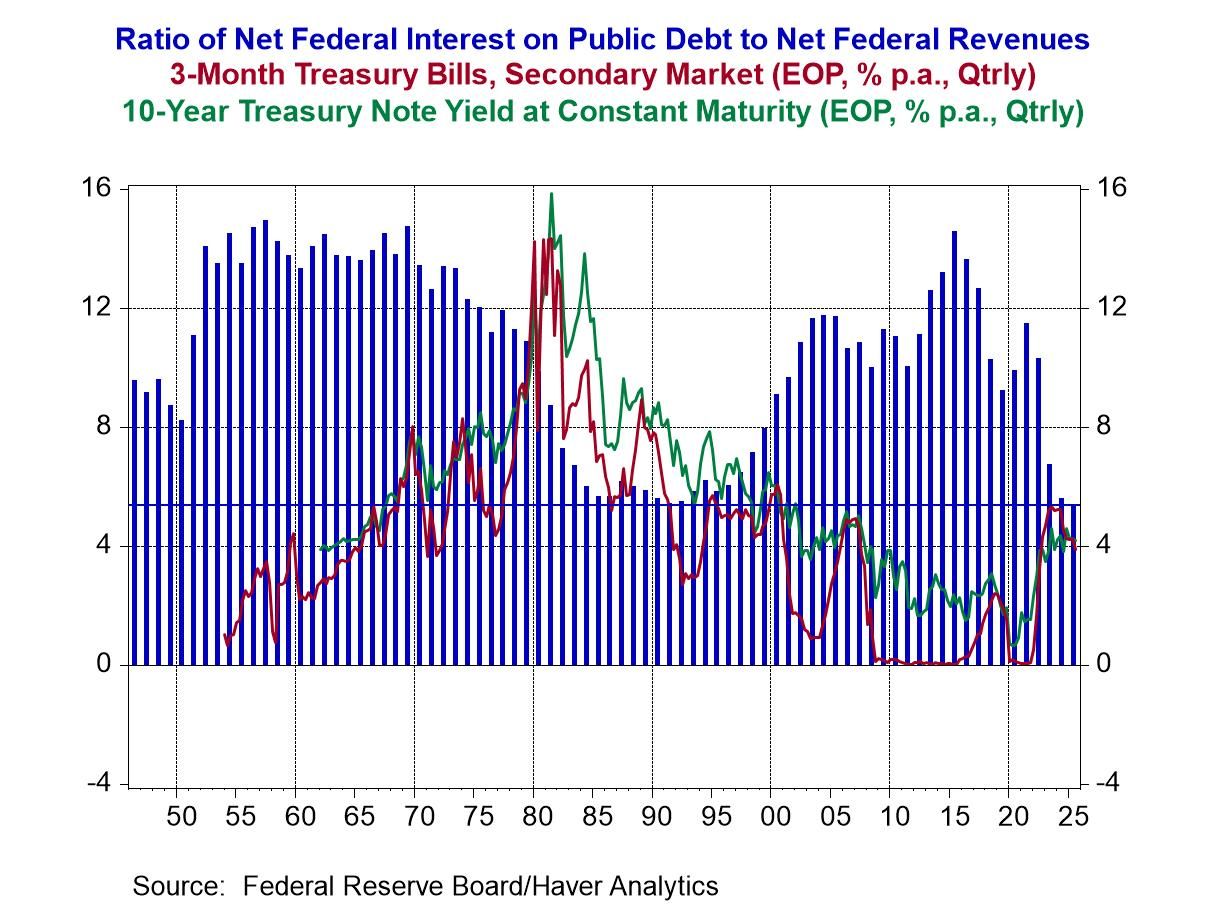

Plotted in the chart below are fiscal year (FY) ratios of federal net interest payments on the public debt to federal net revenues (blue bars) along with end-of-quarter 3-month Treasury bill rates and 10-year Treasury yields. In FY 2025, the ratio of net interest on the public debt to federal net revenues was 5.4, the lowest in the post-WWII era and the lowest since FY 1991, when interest rates were almost twice the level they are now. You can think of the ratio of net interest to net revenues as similar to a corporation’s interest coverage. The CBO forecasts that with the passage of OBBBA, net interest will increase by $4.7 trillion starting in FY 2026 through FY 2029. Unless there is a Festivus miracle resulting in a commensurate increase in federal net revenues, the federal government’s interest coverage will fall below that of an already low FY 2025’s.

The CBO is forecasting that the yields on Treasury 3-month constant maturity and 10-year constant maturity securities will average in calendar year 2028 3.2% and 3.9% respectively. On December 2026, 2025, the Treasury 3-month and 10-year securities closed at 3.64% and 4.14%, respectively. So, the CBO is forecasting a decline in the interest rates at which the Treasury will have to pay on its new and refunded debt it will issue in the next few years. And still, the CBO projects that net interest on the public debt will increase by $4.7 trillion over the next four fiscal years.

Now, let’s talk about Treasury debt management. At the Federal Reserve Bank of New York Treasury Market Conference on November 12, 2025, Treasury Secretary Bessent said that the Treasury was expanding its buyback program of longer-maturity off-the-run Treasury securities allegedly to enhance the liquidity of the overall Treasury securities market. Although Secretary Bessent did not say what maturity of securities the Treasury was selling to replace the securities being replaced, it is a good bet it is shorter-maturity securities. Secretary Bessent said that the Treasury is playing close attention to what maturity securities the market is seeking to purchase. To that point, he mentioned the increased demand for Treasury bills coming from the current and expected growth in the Stable Coin market, banks relief from supplementary leverage ratios and the Fed’s return to Treasury bills to manage bank reserves. I still do not understand the demand for Stable Coins. Why would I purchase a Stable Coin for one dollar for a promise by the issuer to pay me back one dollar on demand at some time in the future. Meanwhile, the Stable Coin issuer buys Treasury bills, money market funds and who knows what else, earning the interest. Why wouldn’t I just purchase Treasury bills or money market funds and collect the interest instead of the Stable Coin issuer unless I were going to use the Stable Coins for illegal transactions? But I digress. I think the essence of Bessent’s comments is that the Treasury is intent on shortening the maturity of the public debt. Why? Perhaps to ameliorate the interest expense on the massive amount of new debt and debt to be rolled over in the coming years, assuming short-maturity interest rates do not increase much. Increased interest expense can cause the amount of debt outstanding to explode. The Treasury would be borrowing more not only to fund the primary budget deficit (the deficit excluding net interest) but the increased net-interest expense. It is similar to household borrowing from another source to pay the rising interest on the outstanding balance on a credit card.

This is where the Fed enters the picture. The president has made no secret of his desire to see the federal funds rate move lower. The president has had the opportunity to appoint one new member to the Board of Governors, Stephen Miran, the genius behind the tariff increases. His term terminates on January 31, 2026. Whether Governor Miran is re-nominated to stay on the Board depends on a number of things, including whether Chairman Powell announces whether he will stay on the Board as a common governor after his chairmanship terminates (he will not be re-nominated as chair) and whether the president nominates a new chairman from among the current Board members or chooses someone not currently on the Board. Regardless, Governor Miran knows which side his bread is buttered on and has been outspoken in his desire to see the federal funds rate cut even more than the 75 basis that has occurred starting on September 18, 2025. A majority of the Federal Open Market Committee (FOMC) has voted for the three 25 basis-point cuts in federal funds rate starting on September 18 regardless of (in spite of) the incoming data pertaining to the US economy. I can’t help but believe that some members of the FOMC voting to cut the federal funds rate are “auditioning” for a chairmanship nomination.

If the Fed can be induced to keep the federal funds rate lower than it would otherwise would be in light of economic conditions, especially the inflation rate and the maturity of the public debt is shortening, then the Treasury’s interest expense can be held down. In turn, this can help prevent an explosion of the public debt that would otherwise result from higher interest expenses. But there’s no free lunch here. The cost of the Fed holding the federal funds rate artificially low is higher inflation. This is tantamount to the Treasury defaulting on its debt by reducing the real value of the debt. (Read “The Mandibles” by Lionel Shriver for a fictional dystopian description of this.)

I got a lot of other problems with the Fed, one of which is its use of the core inflation rate in its policy decisions. But I’ll save that for another day. After all, if the president can air his grievances nearly everyday, why can’t I?

But now it’s time to gather around the aluminum (aluminum has a high strength-to-weight ratio), tinsel-less (I find tinsel distracting) Festival pole and sing O’ Festivus (lyrics by Katy Kasriel)

O' Festivus Lyrics by Katy Kasriel To the melody of O' Tannenbaum

O' Festivus, O' Festivus, This one's for all the rest of us. The worst of us, the best of us, The shabby and well-dressed of us. We gather ‘round the ‘luminum pole, Air grievances that bare the soul. No slights too small to be expressed, It's good to get things off our chest.

Paul L. Kasriel

AuthorMore in Author Profile »Mr. Kasriel is founder of Econtrarian, LLC, an economic-analysis consulting firm. Paul’s economic commentaries can be read on his blog, The Econtrarian. After 25 years of employment at The Northern Trust Company of Chicago, Paul retired from the chief economist position at the end of April 2012. Prior to joining The Northern Trust Company in August 1986, Paul was on the official staff of the Federal Reserve Bank of Chicago in the economic research department. Paul is a recipient of the annual Lawrence R. Klein award for the most accurate economic forecast over a four-year period among the approximately 50 participants in the Blue Chip Economic Indicators forecast survey. In January 2009, both The Wall Street Journal and Forbes cited Paul as one of the few economists who identified early on the formation of the housing bubble and the economic and financial market havoc that would ensue after the bubble inevitably burst. Under Paul’s leadership, The Northern Trust’s economic website was ranked in the top ten “most interesting” by The Wall Street Journal. Paul is the co-author of a book entitled Seven Indicators That Move Markets (McGraw-Hill, 2002). Paul resides on the beautiful peninsula of Door County, Wisconsin where he sails his salty 1967 Pearson Commander 26, sings in a community choir and struggles to learn how to play the bass guitar (actually the bass ukulele). Paul can be contacted by email at econtrarian@gmail.com or by telephone at 1-920-559-0375.