The Pass-Through of Fuel Costs to Core PCE Inflation

by:Joel Prakken

|in:Viewpoints

Iran’s closure of the Straits of Hormuz on March 2 has sent fuel costs spiraling upwards. The Fed’s preferred measure of inflation is of the price index for core personal consumption expenditures (PCE). These exclude consumers’ direct (or “final”) purchases of gasoline & other motor fuel. However, increases in the cost of fuel used to produce and transport core consumer goods & services may pass through to core prices. In a recent paper I present compelling empirical evidence that the pass-through of intermediate fuel costs to final core consumer prices is highly significant and could contribute as much as 0.8 extra percentage points to second-quarter annualized core inflation.

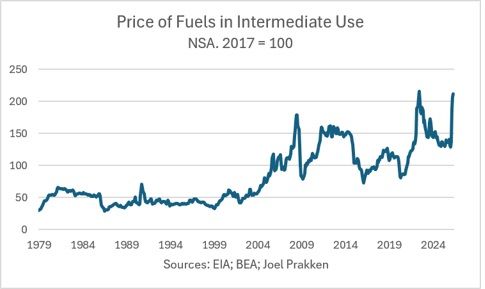

I began by constructing a price index for the intermediate consumption of the three major fuels: diesel fuel, gasoline, and jet fuel. In doing so I assumed the domestic consumption of diesel fuel and jet fuel is all intermediate while treating as intermediate the domestic consumption of gasoline not included in PCE. The average (since 1979) shares of the three fuels in intermediate use are: diesel fuel (62%), gasoline (25%), and jet fuel (14%), but recently those shares are 66%, 13% and 21%, respectively.

The monthly price index (2017=100, not seasonally adjusted) is shown through May in the chart. I seasonally adjusted the monthly index, quarterly averaged the seasonally adjusted series, and then included the change in the fuel price in my Phillips Curve model for core PCE inflation. The resulting highly significant estimate implies that each one percentage point of fuel cost inflation raises core PCE inflation by .00525 percentage point.

Implications? In the first quarter of 2026 the price index for intermediate fuels grew at a 44.7% annual rate, contributing 0.00525x44.7 = 0.23 percentage point to core PCE inflation. However, almost all the first-quarter increases in fuel prices occurred in March, creating unfavorable “statistical momentum” for prices heading into the second quarter. As seems reasonable, assume that recent daily prices persist through the end of June. Then, the second-quarter rate of increase in the price index of intermediate fuels would be around 157%, contributing 0.00525x157 = 0.82 percentage point to core PCE inflation! Lags in the model would temporarily propagate these shocks.

A complete version of this commentary is available here.

Joel Prakken

AuthorMore in Author Profile »Joel Prakken is former Chief US Economist of S&P Global and IHS Markit, co-founder of Macroeconomic Advisers, and past president and director of the National Association for Business Economics. He has served as an outside advisor to the Congressional Budget Office, on the Advisory Panel of the Bureau of Economic Analysis, and as a consultant to the Joint Committee on Taxation. He holds a BA in economics from Princeton University and a PhD in economics from Washington University in Saint Louis.