Europe's Challenge

|in:Viewpoints

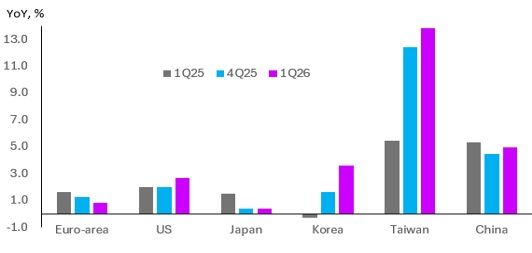

Europe entered the latest energy shock from a weaker position than it occupied before the 2025 global tariff shock. Unlike much of Asia, its exporters have yet to regain momentum and economic growth has slowed. First-quarter GDP data underline the divergence. Euro-area output expanded by only 0.8% year on year, weaker than at the end of last year and below the pace recorded a year earlier. By contrast, growth accelerated in the United States, Korea, Taiwan and China, while Japan broadly held steady (Figure1). Europe therefore enters the latest period of geopolitical uncertainty with less economic momentum than many of its major competitors, leaving businesses and policymakers with less room to absorb further shocks.

Figure 1: GDP

Source: Haver Analytics & Westbourne Research

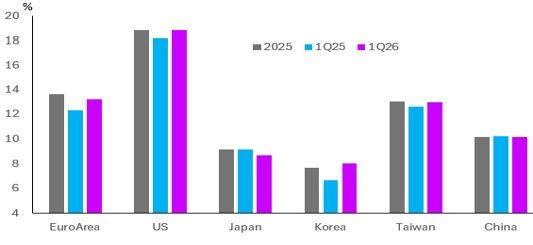

Corporate resilience masks a weaker economy There are nevertheless important positives. Corporate profitability continued to strengthen during the first quarter, with average return on equity for listed companies almost one percentage point above the level recorded a year earlier (Figure 2). Corporate balance sheets remain relatively healthy, financing costs remain favourable in real terms and the profit cycle continues to improve.

Figure 2: Return on equity

Source: Bloomberg & Westbourne Research

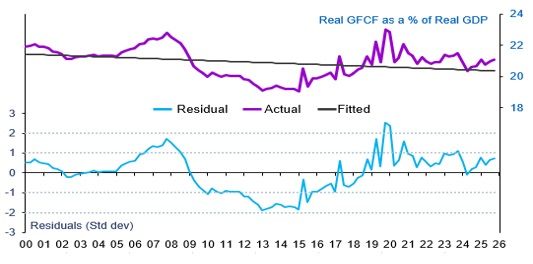

The investment cycle also remains in upswing and strengthened through the first three months of the year (Figure 3). So far businesses have proved remarkably resilient despite weaker domestic demand and rising energy costs.

Figure 3: Euro-area investment cycle

Source: Haver Analytics & Westbourne Research

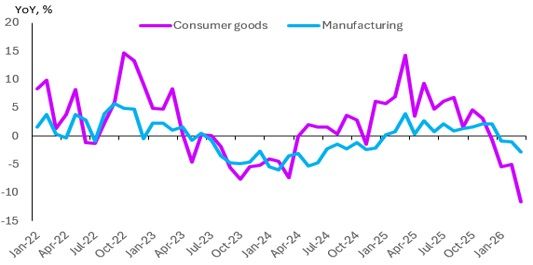

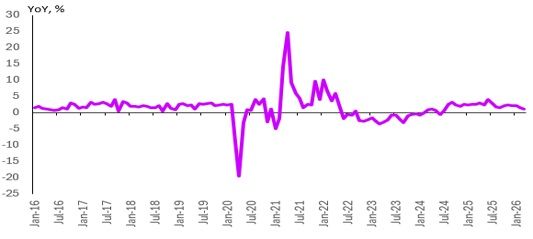

Downside risks are building The concern is that downside risks are increasing. Manufacturing remains in contraction while consumer goods production has softened markedly, suggesting that household demand is becoming increasingly fragile (Figure 4). Export orders have also weakened, reflecting slower global trade and continuing uncertainty surrounding tariffs and supply chains. The investment recovery is therefore taking place against an increasingly uncertain backdrop.

Figure 4: Industrial output

Source: Haver Analytics & Westbourne Research

The credit cycle provides little reassurance. Despite attractive real borrowing costs, loan demand remains subdued. Banks report weaker appetite for investment finance from businesses and expect lending standards to tighten further because of rising risk perceptions, deteriorating asset quality and continuing regulatory pressures.

European consumers are also becoming more cautious (Figure 5). Although unemployment remains historically low, confidence has deteriorated amid concerns over energy prices, living costs and the broader economic outlook.

Figure 5: Euro-area retail sales volumes

Source: Haver Analytics & Westbourne Research

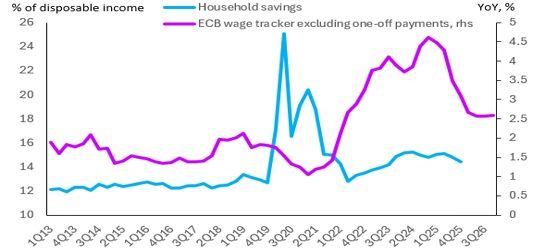

Against this backdrop, recent monetary tightening appears premature. Inflation has largely reflected external energy shocks rather than excessive domestic demand). As global energy prices have moderated, headline inflation has already begun to ease. Fiscal support also remains limited, with assistance focused primarily on energy-intensive industries rather than households. Slower wage growth and softer consumer confidence suggest household spending is likely to remain subdued during the second half of the year (Figure 6).

Figure 6: Household savings and ECB wage tracker

Source: Haver Analytics & Westbourne Research

China competition highlights structural obstacles Europe's relationship with China has undergone a profound strategic shift. Policymakers increasingly view China not simply as a trading partner but also as a strategic competitor. The response has been an expanding range of anti-dumping measures, foreign investment screening, procurement restrictions and industrial policies designed to reduce dependence on Chinese supply chains. Chinese electric vehicles have received most attention, but the policy response extends well beyond the automotive sector to steel, chemicals, industrial inputs, semiconductors and strategic technologies. Carbon border measures and tighter investment screening reinforce the same objective: rebuilding domestic industrial capacity while reducing strategic vulnerabilities.

These concerns are understandable. China has become increasingly dominant across many manufacturing industries, supported by substantial state investment and economies of scale. European policymakers worry about subsidised exports, industrial overcapacity, dependence on critical minerals and broader supply-chain resilience. Yet the evidence suggests Europe's principal challenge is not China itself but its own structural competitiveness.

The European Central Bank has highlighted the growing competitive challenge posed by China, particularly in medium- and high-technology industries. Yet the broader trade picture tells a more nuanced story. Since 2020, US exports to the EU have increased by a cumulative 75%, significantly outpacing the 44% rise in Chinese exports. America's gains have been driven by its leadership in advanced technologies, defence, energy, digital services and artificial intelligence—sectors in which Europe has struggled to build globally competitive industries.

Nor has China's growing presence been an unequivocal negative. Chinese imports of intermediate goods have lowered input costs for European manufacturers, improving competitiveness and supporting industrial production. While imports of finished goods have undoubtedly intensified competition for domestic producers, they have also delivered lower prices and greater choice for consumers. The overall impact is therefore far more balanced than political rhetoric often suggests.

The trade data reinforce this point. Imports from China reached US$632 billion in 2025, accounting for 8.6% of total EU imports. By comparison, imports from the US totalled US$402 billion, or 5.4% of the total. These are relatively modest shares. In contrast, intra-EU trade still accounts for around 62% of all imports, a proportion that has remained remarkably stable since 2016. Viewed in this context, both China and the US have largely gained market share at the expense of other external exporters rather than European producers themselves.

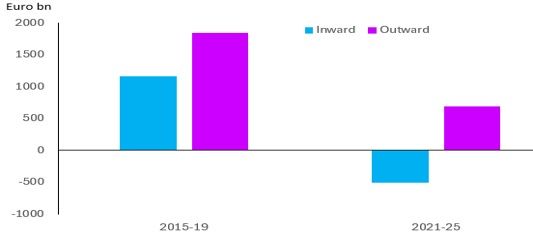

Europe's deeper challenges are therefore largely home-grown. High energy costs, excessive regulation, bureaucratic complexity, weak productivity growth and chronically low private investment have steadily undermined the continent's competitiveness. Foreign direct investment trends tell the same story. Even before the pandemic, outward investment consistently exceeded inward investment. Since then, inward investment has weakened further while many European companies have continued to expand overseas (Figure 7). Europe's competitiveness problem is fundamentally structural, not Chinese.

Figure 7: Euro-area inward and outward foreign direct investment

Source: Haver Analytics & Westbourne Research

Protectionism cannot solve these structural weaknesses. Shielding domestic companies from competition may provide temporary relief, but it risks reducing incentives to innovate, invest and improve productivity. Greater inward investment, faster technology transfer, regulatory reform and a more competitive business environment would provide a more durable foundation for long-term growth.

Investment implications For investors, Europe continues to offer opportunities, but a selective approach is increasingly important. Corporate profitability remains supportive and the investment cycle is in upswing. However, weakening consumer confidence, softer manufacturing activity and tighter credit conditions argue for a more defensive allocation.

High-quality companies with strong balance sheets, pricing power and resilient earnings should continue to outperform. Defence, infrastructure, renewable energy and selected industrial technology businesses remain attractive given structural spending priorities across the continent. Consumer staples also appear well positioned if household spending weakens further. By contrast, export-oriented cyclicals, luxury goods and consumer discretionary sectors remain vulnerable to slowing demand, tighter financial conditions and continuing geopolitical uncertainty.

Sharmila Whelan

AuthorMore in Author Profile »The founder of Westbourne Research (www.westbourne-research.com), Sharmila Whelan is a seasoned Global Geopolitical-Macro Strategist with nearly three decades of experience advising buy-side clients on multi-asset investment strategies and asset allocations. Her career has been defined by her differentiated thinking, a deep understanding of the intricate connections between global geopolitics, macro and policy dynamics, and the Austrian business cycle approach to economic analysis. She has counseled governmental bodies such as the CIA, the US State Department, the British High Commission, DFID, and China’s NDRC.

Sharmila has held prominent roles in both London and Hong Kong, serving as Managing Director at Aletheia Capital, Director at Merrill Lynch Bank of America, Senior Economist at CLSA, and Asia Regional Economist at BP Plc. In 2022, Bloomberg recognised her as one of the UK's "12 New Expert Voices." She is a frequent media commentator on Bloomberg TV and radio, BBC World Business News, and CNBC, and is a sought-after speaker at high-profile events such as the Financial Times Wealth Summit and CFA UK & India conferences. Sharmila also contributes opinion pieces to Financial Times Professional Wealth Management and the Economist Group’s EIU.