Could “Temporary Deflation” follow the “Temporary Oil-Driven Spike in Inflation”?

|in:Viewpoints

*The dramatic spike in oil prices generated 3 months of outsized increases in CPI and PCE inflation that pushed up their yr/yr measures.

*The Fed has kept rates on hold and did not accommodate the negative supply shock, core inflation measures have not increased much, and inflationary expectations have remained anchored.

*Oil prices have fallen sharply, and if current prices stick close to current levels (around or below $75/barrel)—which is uncertain as inventories need rebuilding--continued rapid price declines in gasoline and other energy may result in several months of declines in the CPI and PCE Price Index.

*This would ease some price pressures on consumers and let the Fed breath more easily.

In a note in mid-April, I described how the spike in oil prices from $65/barrel to $95/bbl would temporarily boost the monthly inflation data for about three months as retail prices adjusted to the higher oil prices. I emphasized the importance of the Fed not accommodating the negative supply shock, which would keep its impacts temporary, limit the pass through of the higher oil prices to the prices of nonenergy goods and services, and constrain inflationary expectations. I noted that if oil prices remained around $95/bbl, after several months of outsized increases, the monthly inflation data would revert to their prior increases, while their yr/yr measures would rise to absorb the temporary monthly spikes.

I continued: “However, if oil prices fall, subsequent months' CPI and PCE Price Index data would possibly decline, and the temporary months of deflation would reduce the general price level from its oil price-driven peak.” That process is now beginning to unfold. Yippee: a positive supply shock that involves a partial reversal of the negative supply shock imposed by the conflict in the Middle East and relief to consumers and businesses.

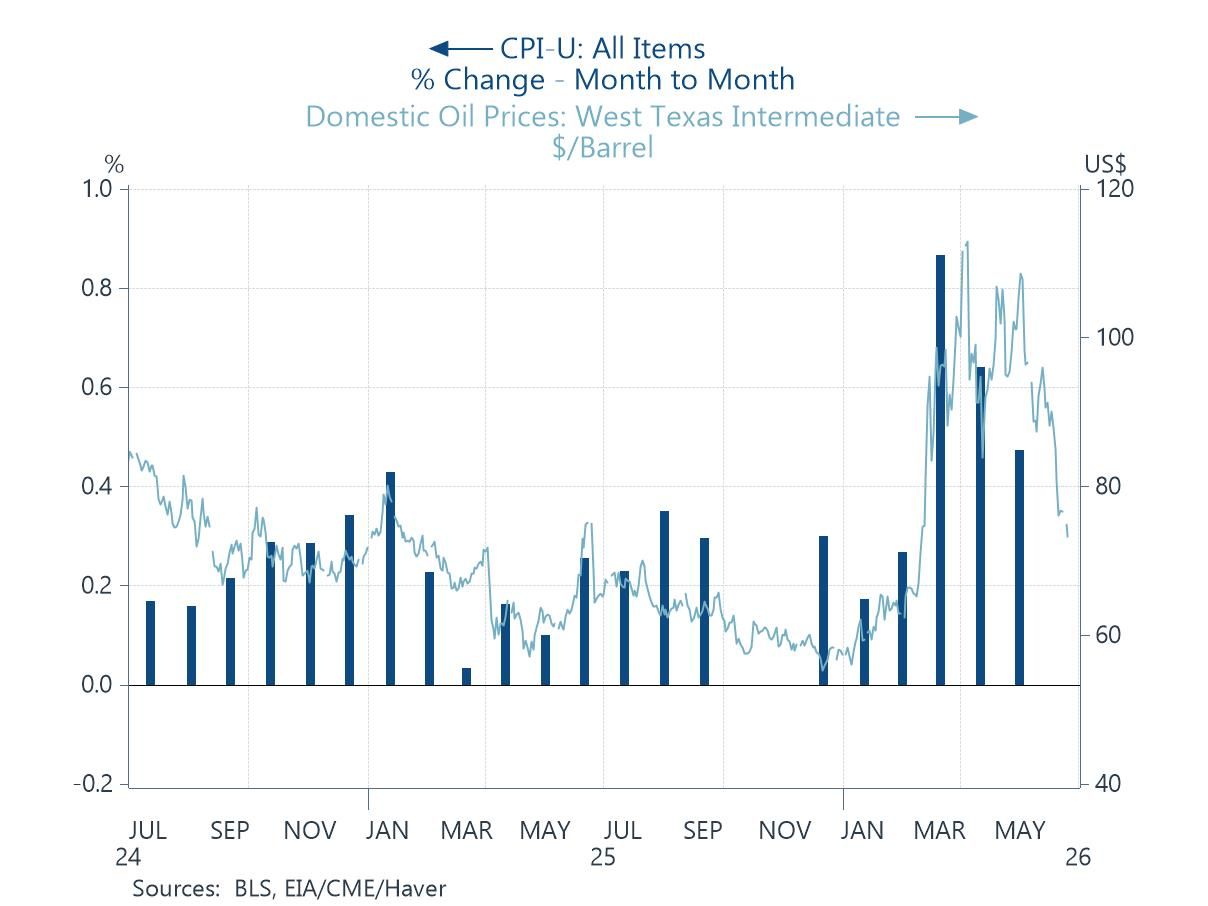

Here’s the situation: in the prior 12 months through February 2026, CPI inflation was 2.4%, averaging a 0.2% increase per month, while PCE inflation was 2.9%, averaging a 0.3% rise per month. The oil price spike pushed up CPI inflation 0.9%, 0.6% and 0.5% in March, April and May, lifting its yr/yr inflation to 4.2% in May, while PCE inflation rose 0.7% and 0.4% in March and April, lifting its inflation to 3.8% in April (PCE inflation for May will be reported tomorrow). See Chart 1. During these months, both core CPI inflation and PCE inflation rose a bit (CPI: 0.2%, 0.4% and 0.2%; PCE: 0.3% and 0.2%), but the details of the CPI indicate that the pass through of the oil price spike was fairly limited to specific categories, including energy services (electricity and utilities) and airline fares. Most categories in the CPI showed little effect of the higher oil prices.

Chart 1. CPI Inflation and WTI Oil Prices

The fall in oil prices will start to show up in the June inflation data and be much more pronounced in the July data. Declines in monthly CPIs are fairly rare, but do occur, particularly when large declines in oil prices generate falling gas and energy prices, like in late 2014).

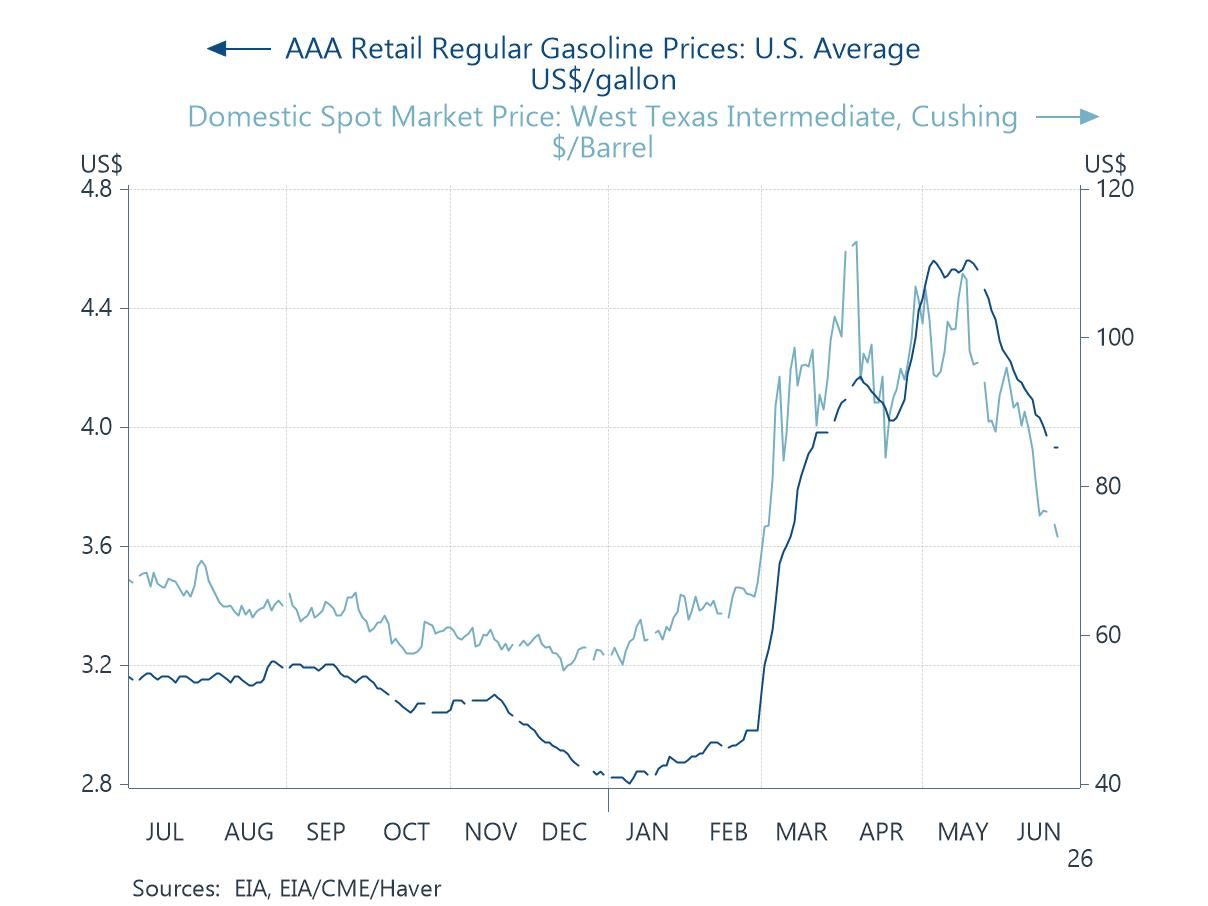

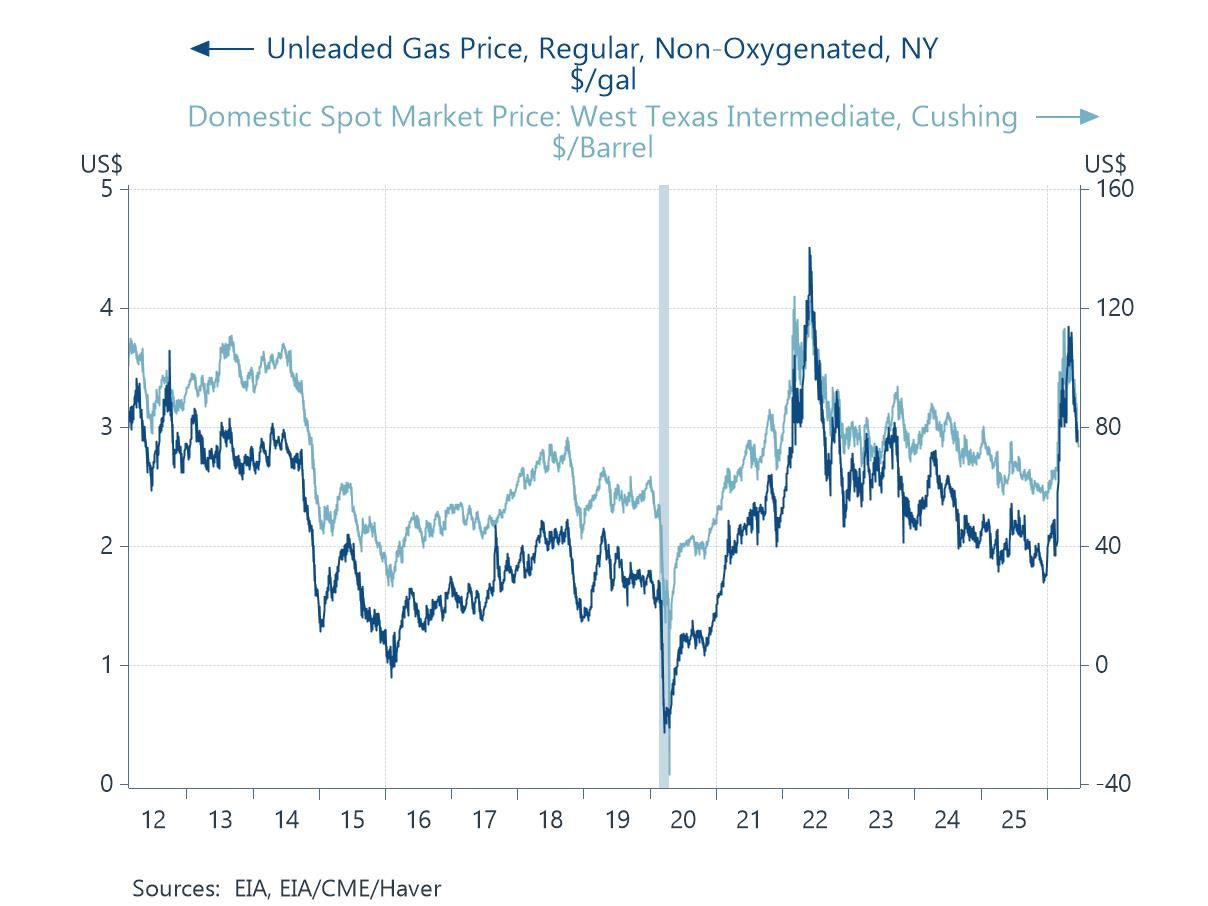

WTI oil prices averaged $97.8/bbl in May and have fallen sharply, averaging $75/barrel in the last week. At this writing, they are around $72/bbl. The speed of the decline in crude oil prices has been impressive, and contrary to the warnings by oil experts that the rebuilding of global oil inventories would keep oil prices high. Thanks to the ramping up of domestically-produced oil, refined products are plentiful. So far, retail gasoline prices have also fallen rapidly, consistent with their historical pattern of adjusting quickly to changes in crude oil prices (Charts 2a and 2b).

Chart 2a. WTI Oil Price and Retail Gas Price

Chart 2b. WTI Oil Price and Unleaded Gas Price

In the first three weeks of June, when oil prices have averaged approximately $86.5/bbl, gasoline prices averaged $4.16/gallon, down from their $4.50/gallon average in May. These declines in retail gas prices should be reflected in the June inflation data, enough to ease the monthly increase in the CPI and PCE Price Index. The CPI should also get some relief from lower prices of airfares, where anecdotal evidence suggests some easing of prices. On the other hand, energy-related surcharges on distribution costs and other services are expected to be slower to adjust to the lower gasoline and energy prices.

If oil prices hold anywhere close to current levels, outright declines in the monthly inflation measures would be likely. They would reduce the yr/yr inflation back toward its pre-oil price spike levels. That would make the March-May oil price shock truly temporary.

A note on the term “temporary”. The Fed’s reference to the surge in inflation beginning in 2021 as a “transitory supply shock” was erroneous and misguided. While the Covid pandemic bottled up global supply chains and was a temporary negative shock to supply, the unprecedented fiscal and monetary stimulus (deficit spending was increased by 25% of GDP and the Fed reduced rates to zero and effectively purchased one-half of the increase in Treasury bond issuance) generated the strongest acceleration of aggregate demand in modern U.S. history, which obviously contributed to the high inflation. The Fed, which had presumed inflation would stay low as it did during the recovery from the Great Financial Crisis, called the rise in inflation “transitory”, and subsequently, it purposely chose to understate (ignore) its role in generating the surge in inflation, instead blaming it on a negative supply shock. Also, remember that after the surge in inflation, the Fed emphasized that its goal was to reduce inflation to 2%, thus accepting the permanently higher general price level that it had contributed to.

In response to the recent oil price shock, if the Fed had accommodated it, the temporarily higher monthly inflation could have become a more permanent one. But the Fed wisely kept monetary policy on hold, so its inflationary impact will be temporary. Now, the lower oil prices hold the prospect that the general price level will fall and partially reverse some of its sharp rise during the negative supply shock.

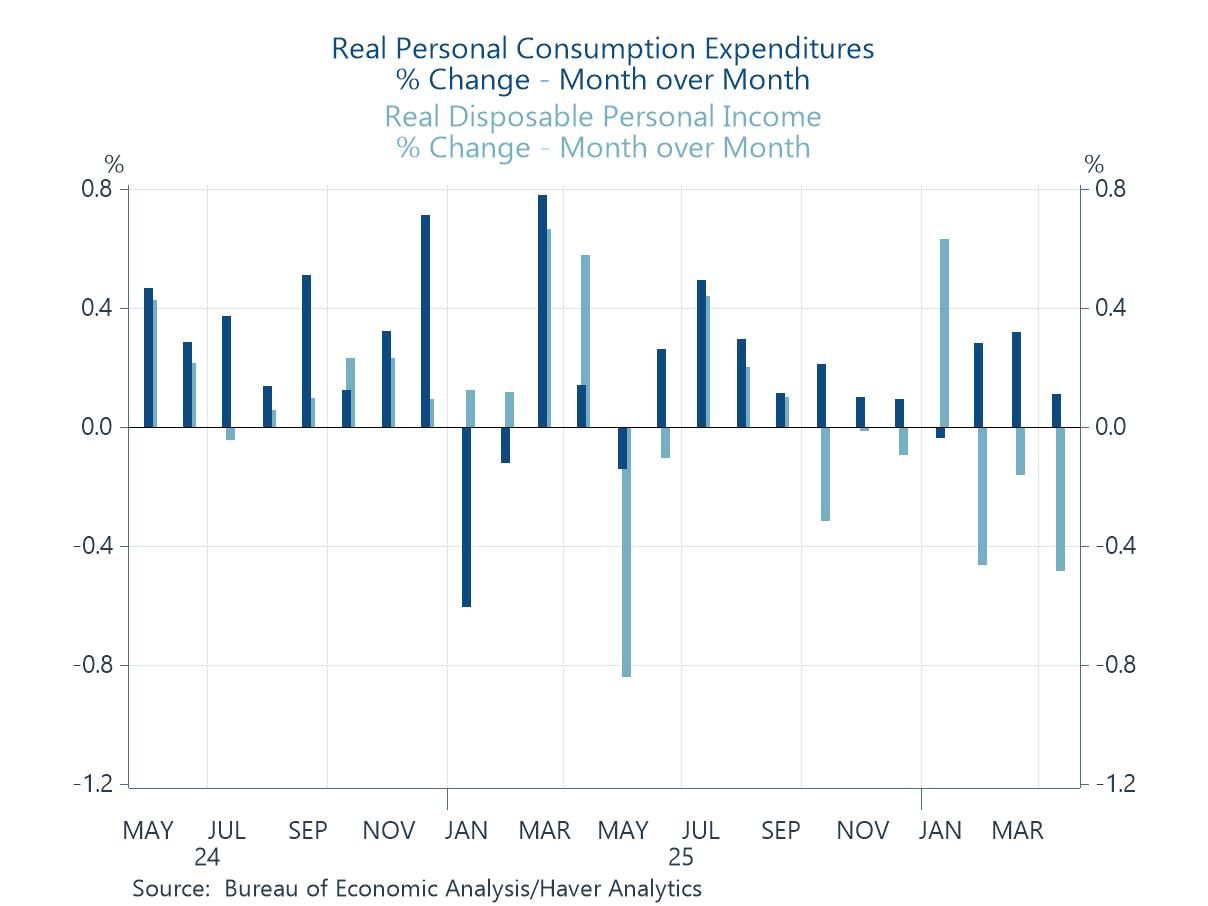

Consumer spending patterns. Consumers have remained resilient. While the three months of spikes in inflation have resulted in declines in real disposable personal income, inflation-adjusted consumption has continued to rise (Chart 3). On average, consumers have drawn down their rate of personal saving of disposable income and smoothed spending (in April, the rate of personal saving fell to 2.6%, close to an all-time low). The continued rise in consumption has been aided by several factors: following a period of weakness, employment payrolls have increased in each of the last three months; last year’s tax cut package increased tax rebates in Spring 2026; and rising household net worth has supported higher propensity to spend. Of note, in contrast to prior surges in oil and gas prices, motor vehicle sales rose a bit during the three months March-April-May when gasoline prices surged.

An easing of inflation--or better yet a reversal of the recent inflation spikes with some temporary (couple of months) of deflation--would provide relief for consumers and increase their purchasing power. That relief would come during peak seasons for driving and electrical services usage.

Chart 3. Real Consumption and Disposable Income

The Fed’s monetary policy. The Fed is to be commended for not accommodating the negative oil supply shock. At its June FOMC meeting and at Kevin Warsh’s first post-FOMC meeting press conference, Warsh made clear that reducing inflation to the Fed’s 2% target was a priority, and he moved away from the Fed’s earlier characterization that monetary policy was mildly restrictive. In its updated June Summary of Economic Projections, the FOMC members estimated that a rate hike may be appropriate to be consistent with its dual mandate. But the FOMC member dots are not binding, and subject to changing conditions.

Could a bout of temporary deflation change the monetary policy landscape? Yes. Of course, the Fed’s monetary policy deliberations would depend on core inflation, but several months of deflation would raise the real Fed funds rate and change the environment. Warsh and the Fed favor lower inflation, but Warsh is also practical. I doubt if the Fed would vote to raise rates in an environment in which the general price level is declining.

Stay tuned.

Mickey D. Levy

AuthorMore in Author Profile »Mickey Levy is a macroeconomist who uniquely analyzes economic and financial market performance and how they are affected by monetary and fiscal policies. Dr. Levy started his career conducting research at the Congressional Budget Office and American Enterprise Institute, and for many years was Chief Economist at Bank of America, followed by Berenberg Capital Markets. He is a Visiting Fellow at the Hoover Institution at Stanford University and a long-standing member of the Shadow Open Market Committee.

Dr. Levy is a leading expert on the Federal Reserve’s monetary policy, with a deep understanding of fiscal policy and how they interact. He has researched and spoken extensively on financial market behavior, and has a strong track record in forecasting. Dr. Levy’s early research was on the Fed’s debt monetization and different aspects of the government’s public finances. He has written hundreds of articles and papers for leading economic journals on U.S. and global economic conditions. He has testified frequently before the U.S. Congress on monetary and fiscal policies, banking and credit conditions, regulations, and global trade, and is a frequent contributor to the Wall Street Journal.

He is a member of the Council on Foreign Relations and the Economic Club of New York, and previously served on the Panel of Economic Advisors to the Federal Reserve of New York, as well as the Advisory Panel of the Office of Financial Research.

Dr. Levy holds a Ph.D. in Economics from University of Maryland, a Master’s in Public Policy from U.C. Berkeley, and a B.A. in Economics from U.C. Santa Barbara.