Tariffs, U.S. Trade and Economic Performance

|in:Viewpoints

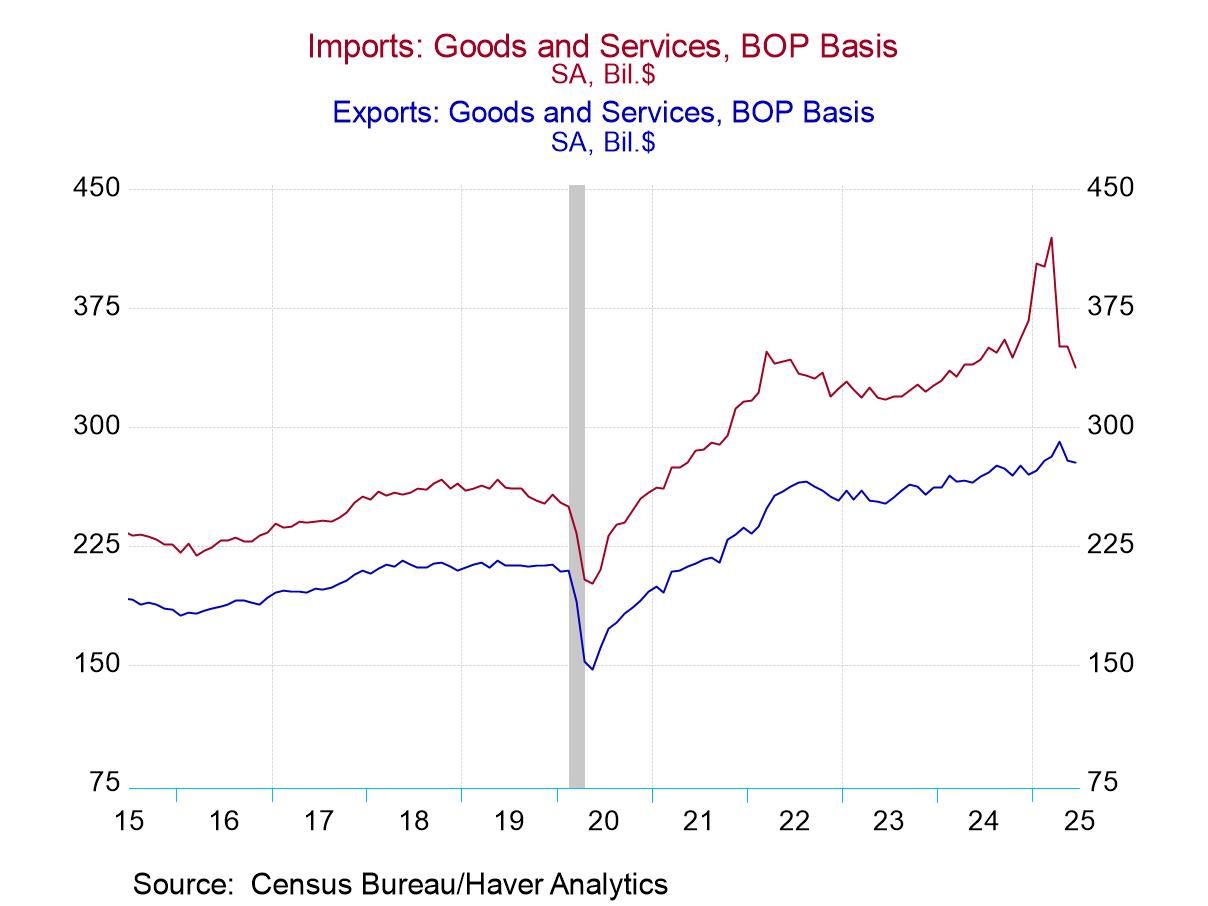

The trade deficit narrowed slightly in June, as exports fell 0.5% from May and imports fell 3.7%, clearly reflecting the negative impact of President Trump's on-again, off-again tariff policies and related uncertainties.

It was the third consecutive month of declining imports following the bulge in Q1 when U.S. businesses ramped up imports in anticipation of tariffs. Chart 1, which shows the bulge in imports earlier this year and its recent unwinding, is striking. The chart also shows the flattening of imports in 2018-2019 following a healthy rise in prior years before Trump imposed tariffs in his first term. June exports fell for the second consecutive month.

Chart 1. U.S. Imports and Exports

The surge in imports in Q1 was driven heavily by a 72.8% annualized rise in imports of information processing equipment. Amid fairly weak consumption, a hefty portion of the rise in imports resulted in a rise in business inventories. Consumption accelerated modestly in Q2, rising 1.4% annualized compared to 0.5% in Q1 (and well below a 2.6% average in 2023-2024), but that was enough to allow businesses to sell much of their accumulated inventories in Q2. The National Income and Product Accounts recorded a swing from inventory accumulation of $120 billion in Q1 to liquidation of $20 billion in Q2.

As shown in Table 1, the widening of the trade deficit associated with the spurt in imports subtracted 4.6 percentage points from RGDP, offset by a 1.4 ppt contribution by business fixed investment and the surge in inventories that added 2.6 ppt to RGDP.) The tariff-induced reversal in Q2 resulted in a narrowing trade deficit that added 5.0 ppt to RGDP while the inventory liquidation subtracted 3.2 ppt.

Since businesses' prices to customers were based on inventoried goods that had largely preceded the tariffs, there was no material impact on the measures of inflation--the PPI (at both final goods and intermediate goods stages) were flat and the PCE price index and CPI inflation each rose a touch but it's hard to see the impact of tariffs.

So far, the actual tariffs that U.S. businesses have remitted to the Customs Bureau of the U.S. Treasury Department has actually lagged behind calculations of the "average effective tariff" that has been commonly measured, for reasons explained by Marina Azzimonti of the Federal Reserve Bank of Richmond in "Why Predicted and Actual Tariff Rates Diverged in May 2025", but they should be rising a bit in coming months (Azzimonti's empirical research on the tariffs has been very informative.) Nevertheless, total tariffs in July were $29 billion, with a projected run rate exceeding $300 billion.

Note that if the tariff's revenues in July were extrapolated into the future, the total magnitude of tariffs would be similar in magnitude as the OBBBA tax cuts. Does that mean the tariffs will have impacts that offset the major tax cuts just enacted? No. The distortions to business production and consumers, combined with the spike in uncertainty generated by President Trump’s on-again, off-again tariff policies and retaliations by foreign trading partners, will accentuate the negative economic impact of the tariffs. I don’t expect recession, but they are a definite negative for the economy, both in the near term and the longer run.

I continue to hold to my early assessment that Trump's tariffs will have a much larger negative impact on the real economy than on inflation (or a one-time boost to the general price level). The slowdown in aggregate demand that has begun to unfold supports that view. As the Employment Report for July indicates, while businesses have not increased layoffs of workers, they have paused hiring. The slowdown in employment will be reflected in a slowdown of wage and salary incomes. Combined with heightened uncertainties, this will likely dampen consumer spending. At the same time businesses are taking steps to avoid raising prices to the extent that they harm customers, while inflation-weary customers substitute for cheaper goods.

These interactions create distortions and harm the overall economy, but mitigate the impact on the general price level. Note that consumers’ instincts to substitute cheaper goods or higher priced, tariffed imports also points toward lower measured inflation of the PCE Price Index, which is chain-weighted, than the CPI.

If Trump follows the pattern he established in his first term, the tariff skirmishes will not let up. That means uncertainty will persist—note the Baker-Bloom-Davis Economic Policy Uncertainty Index remains very elevated--which will affect business and household decisions.

The combination of the hit to the real economy, particularly weaker labor markets, and elevated inflation, puts the Fed in a difficult situation in terms of achieving its dual mandate. Historically, the Fed has responded much more quickly to labor market weakness than to higher inflation. Not surprisingly, the futures markets have priced in lower interest rates. Interesting, that’s what happened in Trump’s first term: the tariffs first imposed in mid-2018 that continued with the trade war with China materially slowed growth. This led the Fed to begin lowering rates aggressively beginning in mid-2019. We seem to be following a similar path. President Trump does not seem to have learned from history, even from his first term.

Mickey D. Levy

AuthorMore in Author Profile »Mickey Levy is a macroeconomist who uniquely analyzes economic and financial market performance and how they are affected by monetary and fiscal policies. Dr. Levy started his career conducting research at the Congressional Budget Office and American Enterprise Institute, and for many years was Chief Economist at Bank of America, followed by Berenberg Capital Markets. He is a Visiting Fellow at the Hoover Institution at Stanford University and a long-standing member of the Shadow Open Market Committee.

Dr. Levy is a leading expert on the Federal Reserve’s monetary policy, with a deep understanding of fiscal policy and how they interact. He has researched and spoken extensively on financial market behavior, and has a strong track record in forecasting. Dr. Levy’s early research was on the Fed’s debt monetization and different aspects of the government’s public finances. He has written hundreds of articles and papers for leading economic journals on U.S. and global economic conditions. He has testified frequently before the U.S. Congress on monetary and fiscal policies, banking and credit conditions, regulations, and global trade, and is a frequent contributor to the Wall Street Journal.

He is a member of the Council on Foreign Relations and the Economic Club of New York, and previously served on the Panel of Economic Advisors to the Federal Reserve of New York, as well as the Advisory Panel of the Office of Financial Research.

Dr. Levy holds a Ph.D. in Economics from University of Maryland, a Master’s in Public Policy from U.C. Berkeley, and a B.A. in Economics from U.C. Santa Barbara.