Global| Mar 24 2026

Global| Mar 24 2026Shock, Supply and Constraint

by:Andrew Cates

|in:Viewpoints

The Middle East crisis and the limits of the global economy

For three decades, macroeconomics has leaned on a simple idea: that demand management can stabilise the system. In reality, that framework has been fraying for years. The latest escalation in the Middle East doesn’t just reinforce the point—it sharpens it. This is not another cyclical shock, but a reminder that the global economy is increasingly governed by supply-side constraints that policy cannot easily offset.

Even with tentative signs of de-escalation emerging this week, the episode has brought into much sharper focus a theme I have been returning to repeatedly: the global economy is no longer primarily demand-constrained. It is increasingly shaped—and at times paralysed—by supply-side limits.

From Local Shock to Global System

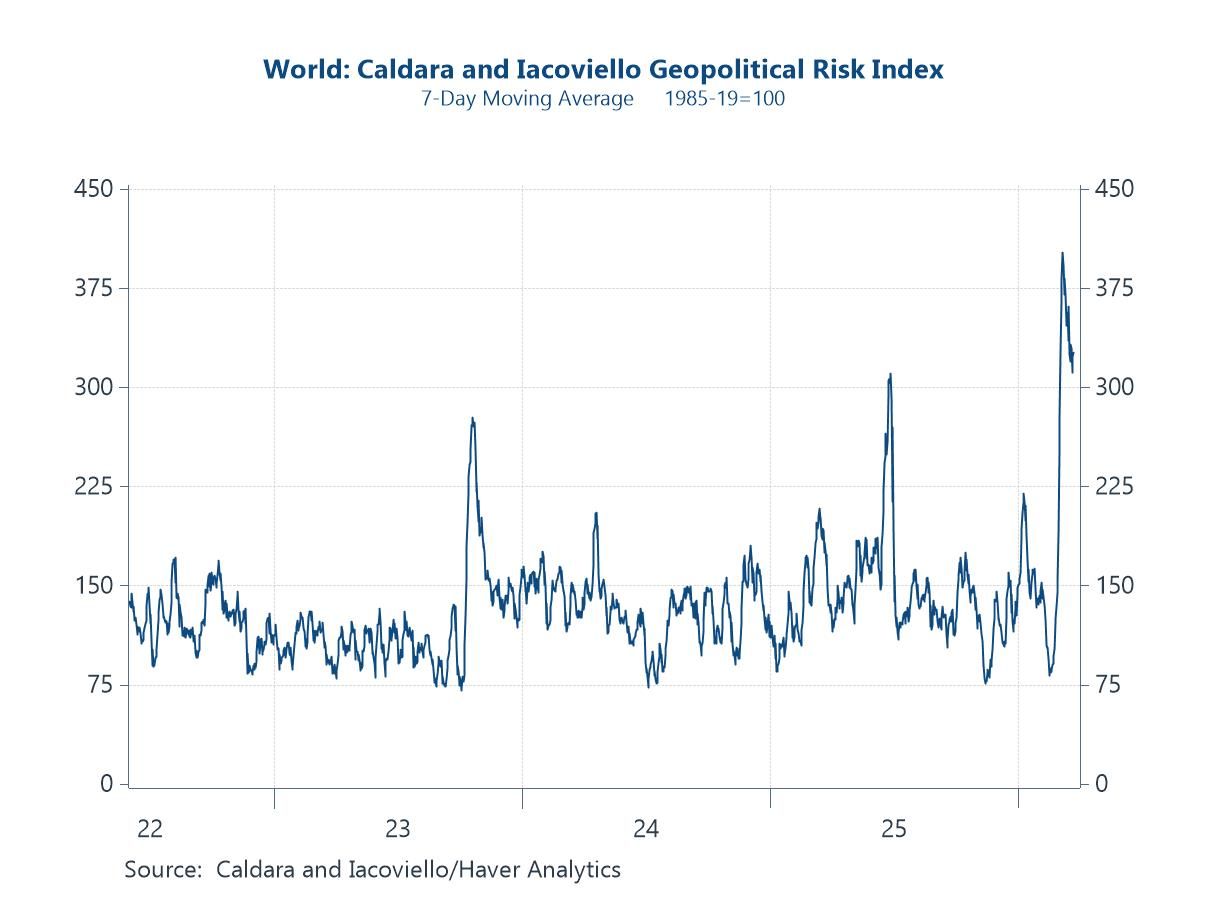

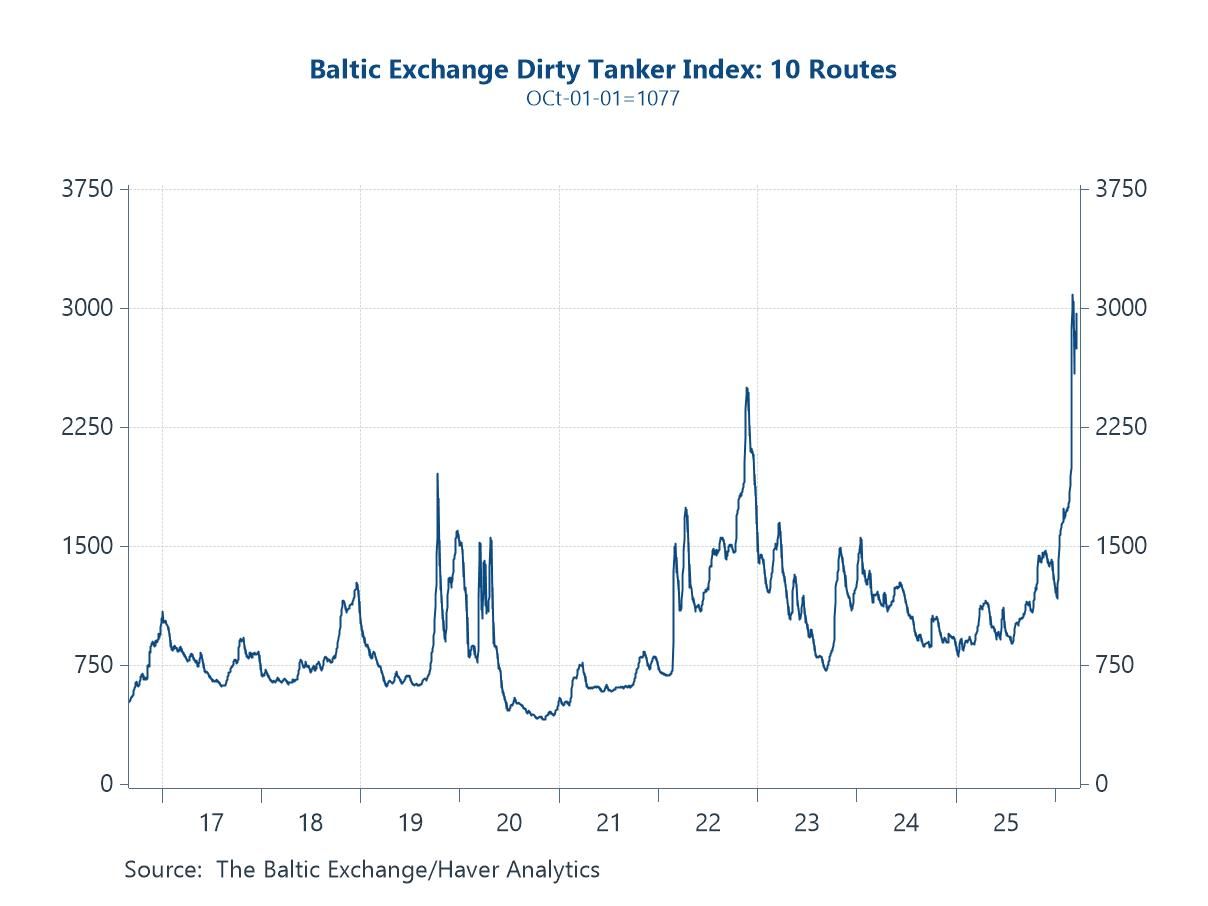

The initial market reaction was familiar. Oil prices surged, shipping costs rose, and geopolitical risk indices spiked. But as many observers have been at pains to stress, focusing only on oil risks missing the broader story. The Middle East is not simply an energy supplier; it is a central artery in the global trading system. Disruptions to the Strait of Hormuz reverberate across a wide range of supply chains: • liquefied natural gas (LNG), critical for electricity generation across Asia and Europe • petrochemicals, which feed into plastics, manufacturing inputs and pharmaceuticals • fertilisers, with direct implications for global food production • metals and refined products moving between Asia, Europe and the Gulf • containerised trade flows that rely on predictable and secure maritime routes

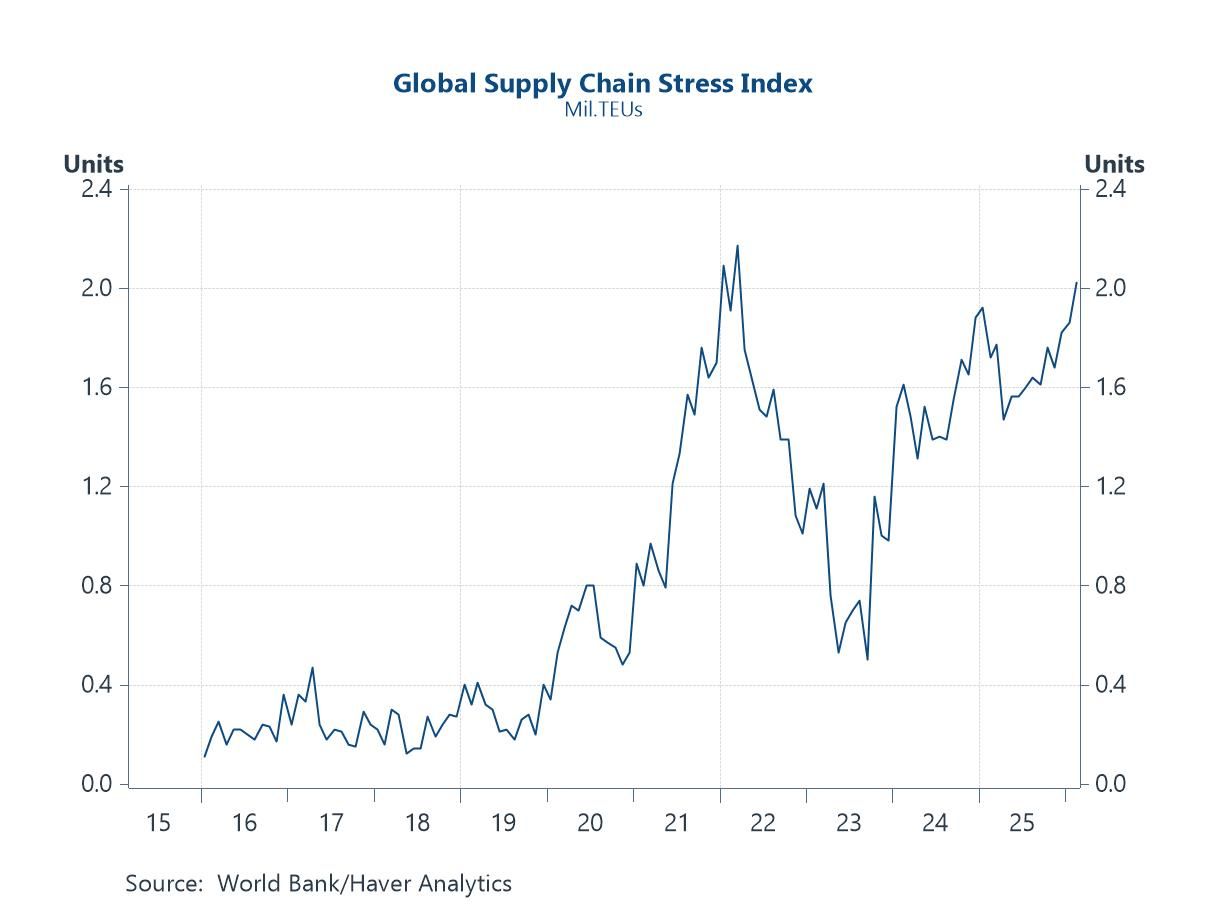

This is not a marginal shock. It is systemic. Higher LNG prices feed into power costs. Fertiliser shortages raise agricultural input costs. Shipping delays disrupt just-in-time production models. Insurance premia rise, increasing the cost of trade even where physical flows continue. And these effects cascade. What begins as a geopolitical event rapidly becomes a multi-channel supply shock, with second- and third-round effects that are both diffuse and persistent.

The Constraint Economy Revealed

This matters because the global economy was already operating in a more constrained state than many models assume. Over the past decade, a series of structural shifts have gradually eroded excess capacity: • underinvestment in energy production • tighter environmental and regulatory constraints • demographic pressures in advanced economies • increasing geopolitical fragmentation of trade • and the gradual exhaustion of some forms of “cheap” globalisation

The result is a world economy that is less able to absorb shocks. In such a system, disruptions do not dissipate quickly. They accumulate, interact and amplify. The Middle East crisis has not created this environment. It has exposed it.

Uncertainty as a Constraint

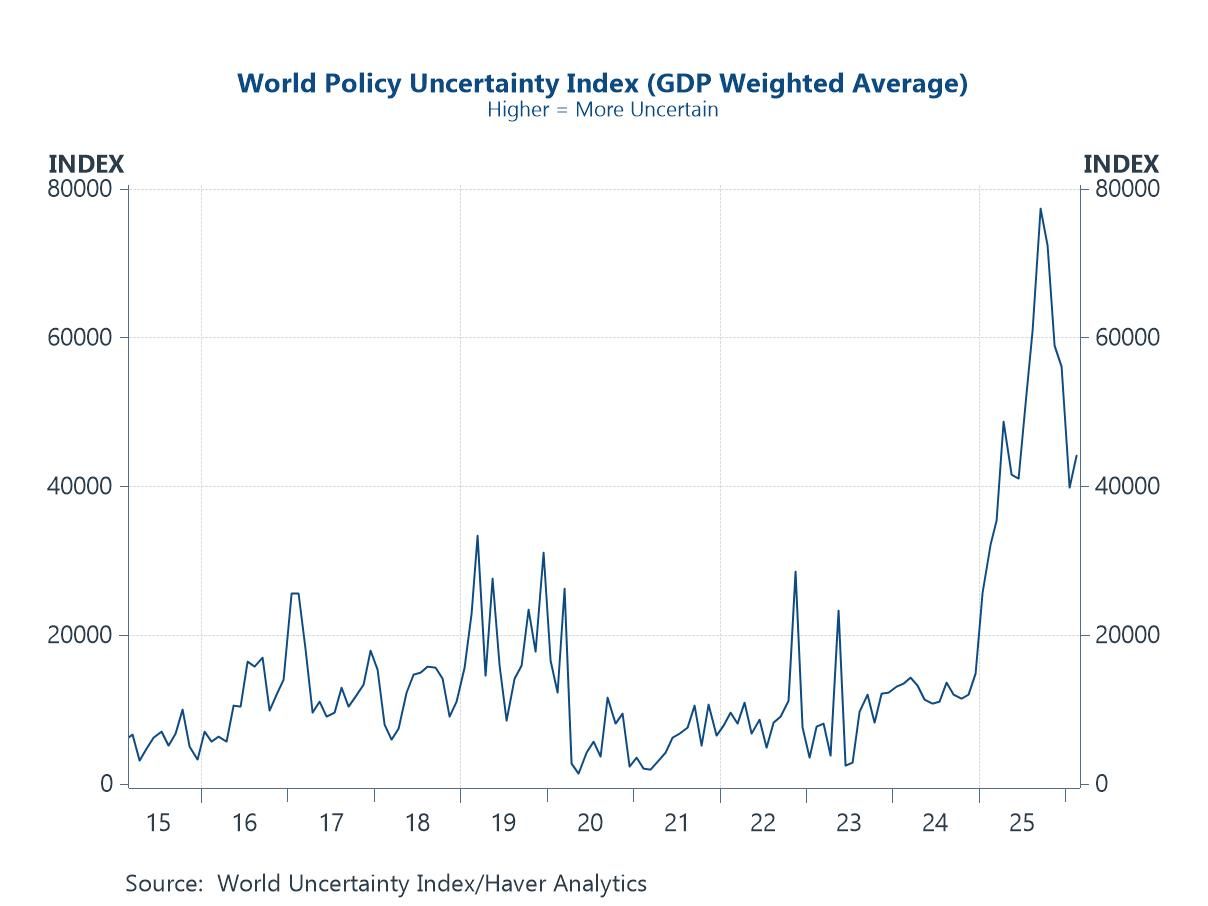

One of the most immediate effects of the crisis has been a sharp rise in uncertainty. But this is not simply a cyclical spike in volatility. It is becoming a structural feature of the global economy.

Firms facing uncertain input costs, unreliable logistics and shifting geopolitical risks are less likely to invest in capacity or commit to long-term projects. Instead, they delay, diversify, or retreat. This has important macroeconomic implications.

Uncertainty does not just affect demand. It constrains supply. It reduces investment, slows productivity growth and reinforces the very bottlenecks that make the system vulnerable in the first place. In this sense, uncertainty itself becomes a binding constraint.

The Inflation Risk Premium Returns

Financial markets are beginning to internalise these dynamics. Central banks such as the Federal Reserve and the Bank of England have paused their easing cycles, and in some cases markets are now pricing in a degree of renewed tightening. That shift reflects not so much a sharp deterioration in current inflation, but a growing recognition that the distribution of outcomes has widened. In a world of recurring supply shocks—energy disruptions, geopolitical tensions and fragmented supply chains—inflation is becoming less predictable and more persistent.

This matters for asset pricing. It points to higher inflation risk premia, more volatile yield curves and a reduced willingness to assume a smooth return of inflation to target. For monetary policy, the challenge is profound. Central banks can influence demand—borrowing costs, credit conditions and expectations—but they cannot increase the supply of energy, resolve geopolitical conflicts or repair disrupted supply chains.

Policymakers are increasingly caught between competing risks: tightening into a supply shock risks deepening a slowdown, while easing could risk entrenching higher inflation. This is no longer the familiar demand-driven trade-off, but a far more uncomfortable reality in which policy tools are poorly matched to the problem.

The Expectations Problem

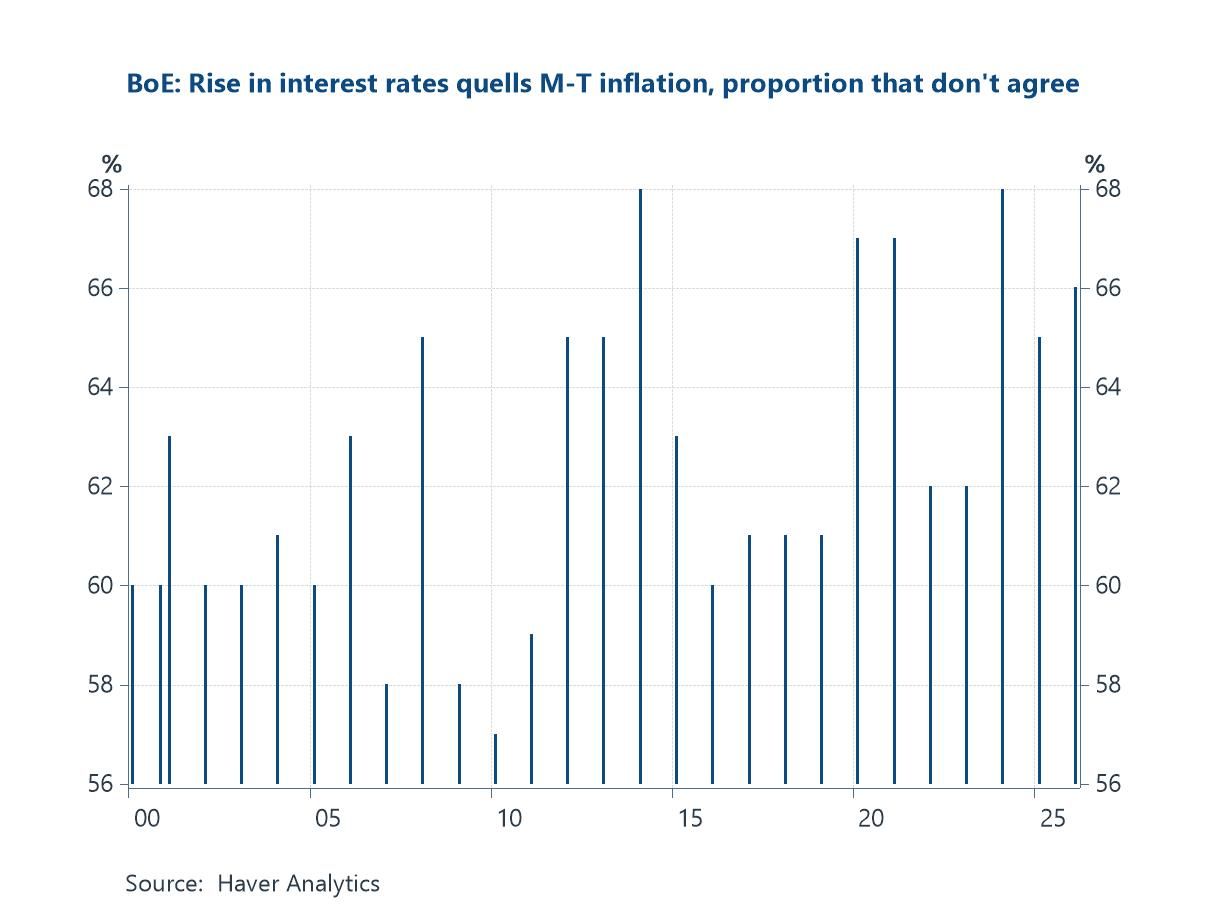

Compounding this challenge is the way households form inflation expectations. A growing body of evidence—particularly from the ECB and recent academic work—suggests that expectations are driven less by monetary policy and more by lived experience: energy prices, food costs, rents and mortgages. In that context, higher interest rates are not always perceived as disinflationary. Instead, they can be seen as part of the inflationary environment—raising borrowing costs and reinforcing the perception of rising prices.

The point is not just theoretical. As the chart shows, a consistently large share of respondents to the Bank of England’s survey—typically around 60–65%—do not agree with the proposition that raising interest rates will reduce medium-term inflation. If anything, that proportion has edged higher over time. In other words, for a majority of households, the core mechanism underpinning monetary policy is either not understood or not believed.

The implication is that the transmission mechanism of monetary policy may be weaker, slower, and at times even partially inverted. Central banks, in other words, are attempting to manage expectations in a world where those expectations are increasingly shaped by forces outside their control—and where policy itself may, at the margin, be reinforcing the very dynamics it is trying to contain.

AI: A Countervailing Force—or Another Constraint?

Set against this backdrop is another major supply-side force: artificial intelligence. In principle, AI offers a potential escape from some of these constraints. By enhancing productivity, automating tasks and reducing labour bottlenecks, it could expand effective supply and ease inflationary pressures over time. But the reality is more nuanced.

In the near term, AI is itself highly resource-intensive. It requires: • vast amounts of energy • significant capital investment • specialised infrastructure (data centres, semiconductors)

This creates a paradox.

AI may ultimately alleviate supply constraints, but in the short to medium term it may intensify them—particularly in energy markets. The surge in data centre demand, for example, is already contributing to upward pressure on electricity consumption and investment needs. Moreover, the labour market effects of AI are uncertain. While it may boost productivity, it could also disrupt income dynamics, particularly for mid-level white-collar workers. That, in turn, has implications for consumption and demand. In other words, AI is not a simple solution. It is another layer of complexity in an already constrained system.

A More Fragile Equilibrium

Put all of this together and a picture emerges of a global economy that is fundamentally different from the one that prevailed in the decades prior to the pandemic. It is: • more constrained in its supply capacity • more exposed to geopolitical shocks • more uncertain in its outlook • and more difficult to manage using traditional policy tools

The Middle East crisis has not changed this trajectory. But it has accelerated it—and made it visible in a way that is hard to ignore.

Andrew Cates

AuthorMore in Author Profile »Andy Cates joined Haver Analytics as a Senior Economist in 2020. Andy has more than 25 years of experience forecasting the global economic outlook and in assessing the implications for policy settings and financial markets. He has held various senior positions in London in a number of Investment Banks including as Head of Developed Markets Economics at Nomura and as Chief Eurozone Economist at RBS. These followed a spell of 21 years as Senior International Economist at UBS, 5 of which were spent in Singapore. Prior to his time in financial services Andy was a UK economist at HM Treasury in London holding positions in the domestic forecasting and macroeconomic modelling units. He has a BA in Economics from the University of York and an MSc in Economics and Econometrics from the University of Southampton.