Semiconductors, Reform and Re-Rating: The Korean Opportunity

|in:Viewpoints

Korean equities, alongside Japan, Taiwan and US technology stocks, were identified at the outset of the Iran conflict as some of the most compelling investment opportunities. All have outperformed the MSCI World Index, but Korea has emerged as the clear standout.

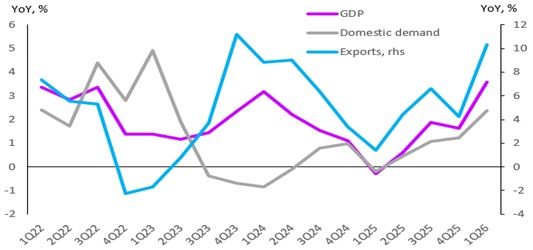

The story extends beyond the stock market. The economy has strengthened markedly, supported by both domestic and external demand. GDP growth accelerated from 1.6% year-on-year in 4Q25 to 3.4% in the first quarter of 2026, driven by robust consumption and non-residential investment spending. Exports have also rebounded strongly, leaving Korea firing on all cylinders (Figure 1).

Figure 1: Economic activity

Source: Haver Analytics & Westbourne Research

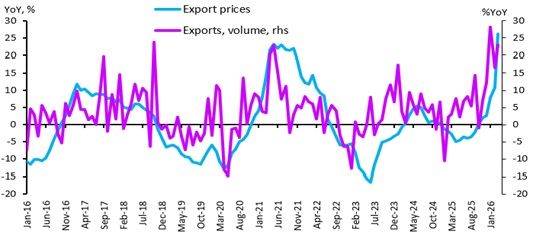

A key factor underpinning this performance is the flexibility of Korean exporters. During weaker periods they have historically protected market share by reducing prices, before rebuilding margins as demand recovers. This strategy is once again paying dividends. As Korea benefits from the global semiconductor upcycle, both export volumes and export prices are rising strongly (Figure 2).

Figure 2: Korean export volumes and prices

Source: Haver Analytics & Westbourne Research

Domestic demand is also strengthening. Korean consumers are spending more freely and remain optimistic despite a weak property market. The government has spent the past two years deliberately cooling housing activity, particularly in the Seoul metropolitan area. Additional measures introduced this year include plans to expand housing supply, utilise public land more efficiently, reform property taxation and reinstate capital gains tax surcharges on owners of multiple properties.

The policy tightening is having its intended effect. Mortgage lending growth has slowed from 9.2% year-on-year in June 2025 to 6.8% in March, while housing transactions have softened and inventories of unsold homes have risen. Real construction spending has been contracting on an annual basis since mid-2024.

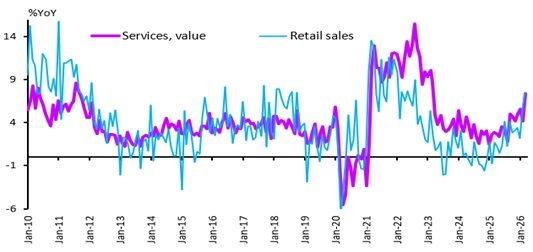

Ordinarily, a weaker housing market would dampen consumer spending, particularly on durable goods. That has not happened. Instead, consumption growth has accelerated (Figure 3), supported by solid wage gains of around 4% year-on-year and declining debt-servicing costs. Lower real lending rates and falling household leverage have improved household finances considerably. Household debt has fallen from 99% of GDP in late 2022 to 87% today, freeing up income for discretionary spending.

Figure 3: Consumer spending

Source: Haver Analytics & Westbourne Research

The combination of stronger domestic demand and recovering exports is lifting manufacturing activity. Capacity utilisation is rising, inventory-to-shipment ratios are falling and production is increasing, particularly in export-oriented industries such as semiconductors, ICT and electrical equipment (Figure 4).

Figure 4: Inventory to shipment ratio

Source: Haver Analytics & Westbourne Research

Corporate profitability remains healthy and business surveys point to further gains in production and investment. New orders, output and business activity continue to expand at a robust pace. The main risks stem from rising input costs and supply-chain disruptions, which have pushed delivery times higher and lifted both input and output prices to multi-decade highs.

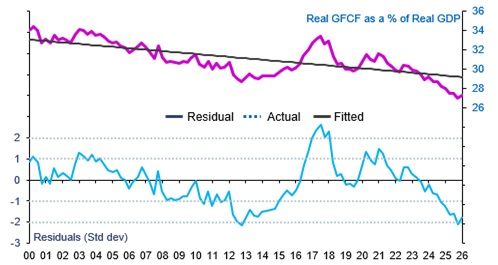

Not everything is improving. The construction downturn continues to weigh on the broader investment cycle, which remains in a downswing (Figure 5). Capital spending is currently concentrated in semiconductors and intellectual property products, while investment in transportation, shipping, machinery and other non-IT sectors remains subdued. Even so, these areas are expected to recover gradually as economic momentum broadens.

Figure 5: Investment cycle

Source: Haver Analytics & Westbourne Research

Why Invest?

The fundamental investment case remains compelling. South Korea's corporate profit cycle is in a clear upswing, economic growth is accelerating and the country sits at the centre of the global AI and semiconductor investment boom.

Equally important, Korea is undergoing a profound transformation in corporate governance and capital markets.

At the heart of these reforms is the Corporate Value-Up Programme, often described as Korea's equivalent of Japan's corporate governance revolution. Introduced in 2024 to address the long-standing "Korea discount", the programme seeks to improve transparency, strengthen shareholder returns, enhance capital efficiency and raise corporate valuations.

The reforms target many of the structural weaknesses that have historically deterred investors, including excessive control by founding families, cross-shareholdings, weak capital allocation practices and limited focus on shareholder returns.

Companies are increasingly being encouraged to articulate clear strategies around return on equity, price-to-book ratios, capital expenditure, dividends and share buybacks. Although participation remains voluntary, investor pressure is already changing corporate behaviour.

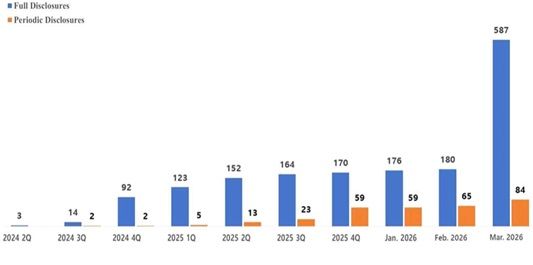

The results are becoming increasingly visible. By March, 490 companies had disclosed Value-Up plans, representing more than 70% of KOSPI market capitalisation and almost 80% of KOSDAQ market capitalisation (Figure 6). In addition, 99 companies announced treasury share cancellations while more than 500 qualified as high-dividend firms.

Figure 6: Accumulated number of firms that disclosed Corporate Value-up Plans

Source: KRX

Dividend growth has been particularly impressive. Total cash dividends reached a record KRW35.1trn in FY2025, up 15.5% from the previous year. The average dividend yield rose to 2.63%, surpassing the government bond yield, while payout ratios increased significantly.

Companies participating in Value-Up programmes are leading the change. Collectively they account for almost 90% of dividends paid by listed firms and are returning more than half of earnings to shareholders on average.

The message is clear: Korean companies are becoming more shareholder-friendly, more disciplined in their use of capital and increasingly focused on maximising corporate value.

The reform agenda extends beyond corporate governance. Korea is also seeking to regain a place on the MSCI Developed Markets Watch List and ultimately graduate from emerging market status.

To support this objective, authorities have introduced a 24-hour foreign exchange market, offshore settlement mechanisms, streamlined reporting requirements, enhanced market infrastructure and easier access for foreign investors. Restrictions surrounding short-selling and derivatives markets are also being reviewed.

These capital-market reforms coincide with the government's broader "Major Economic Leap" strategy, which focuses on scaling national strategic industries including semiconductors, defence, biotechnology and content industries. Additional support is being directed toward venture capital, start-ups and regional development initiatives.

A particularly noteworthy proposal is the creation of a Korean-style sovereign wealth fund designed to channel long-term capital into domestic equities and strategic industries, further reinforcing the government's commitment to supporting capital markets and innovation.

Bottom Line

The Korean equity market is undergoing a broad-based re-rating. This is no longer simply a semiconductor or AI story.

Strong economic growth, an improving corporate profit cycle, healthier household balance sheets and a powerful programme of capital-market reform are combining to create one of the most attractive investment environments in Asia.

The KOSDAQ has benefited disproportionately from the global AI investment boom, but the opportunity is now broadening across the wider market. As the Korea discount narrows and the prospect of a Korea premium emerges, the case for remaining overweight Korean equities remains compelling.

Sharmila Whelan

AuthorMore in Author Profile »The founder of Westbourne Research (www.westbourne-research.com), Sharmila Whelan is a seasoned Global Geopolitical-Macro Strategist with nearly three decades of experience advising buy-side clients on multi-asset investment strategies and asset allocations. Her career has been defined by her differentiated thinking, a deep understanding of the intricate connections between global geopolitics, macro and policy dynamics, and the Austrian business cycle approach to economic analysis. She has counseled governmental bodies such as the CIA, the US State Department, the British High Commission, DFID, and China’s NDRC.

Sharmila has held prominent roles in both London and Hong Kong, serving as Managing Director at Aletheia Capital, Director at Merrill Lynch Bank of America, Senior Economist at CLSA, and Asia Regional Economist at BP Plc. In 2022, Bloomberg recognised her as one of the UK's "12 New Expert Voices." She is a frequent media commentator on Bloomberg TV and radio, BBC World Business News, and CNBC, and is a sought-after speaker at high-profile events such as the Financial Times Wealth Summit and CFA UK & India conferences. Sharmila also contributes opinion pieces to Financial Times Professional Wealth Management and the Economist Group’s EIU.