Global| Mar 02 2026

Global| Mar 02 2026S&P Manufacturing PMIs Show Improvement

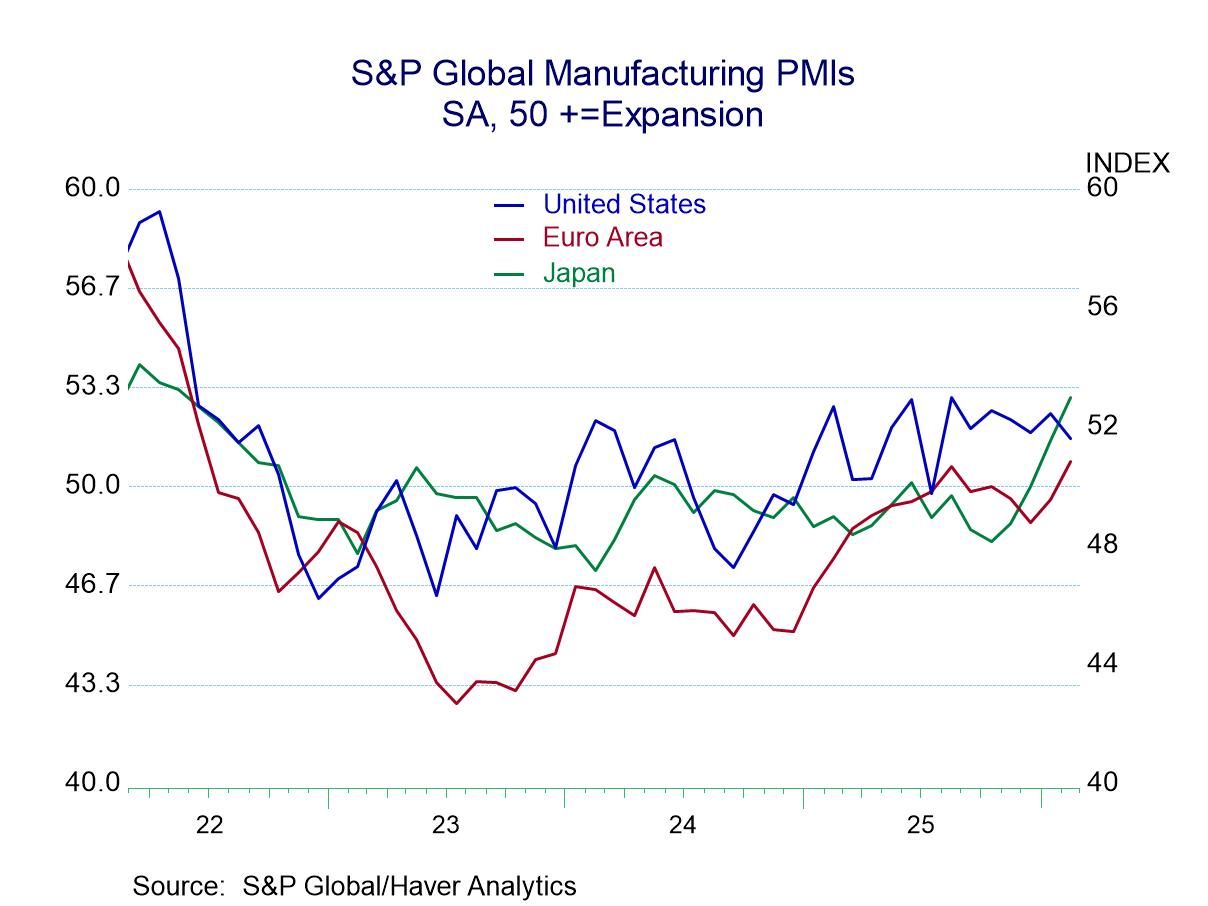

The S&P manufacturing PMI readings for February 2026 continued to show improvement, particularly on a sequential basis.

The chart shows a clear upward tendency for the United States, Japan, and the European Monetary Union where the manufacturing PMIs have been on an increasing track for some time. Japan just surpassed the U.S. this month where the manufacturing PMI reading surged above 50. The U.S. has been steady at that level for a number of months; Japan has just moved up while the euro area reading is starting to show some upward trend.

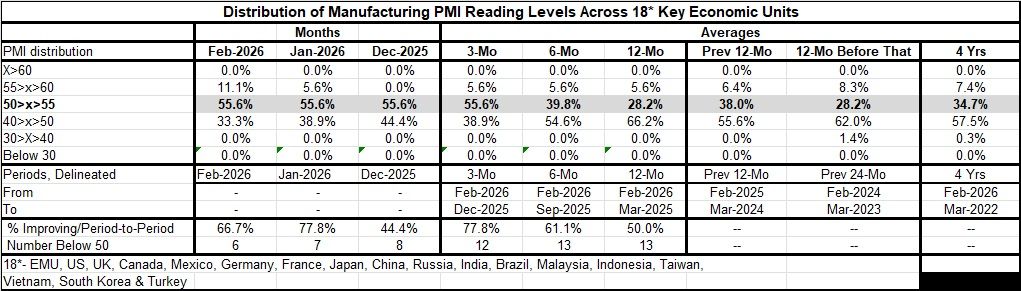

The table takes the underlying diffusion levels reported by these 18 early reporters and shuffles them into six different cohorts to summarize their performance over different periods.

In February, we see twice as many reporters in the cohort between 55 and 60 as we saw in January; that proportion moved up to 11.1% from 5.6%. The proportion in the 50 to 55 diffusion category (mild improvement) was unchanged at 55.6%; the proportion showing mild below median performance declined to 33.3% in February from 38.9% in January. The other cohorts showed no membership.

If we look at the data grouped into sequential categories of three-months, six-months, and 12-months, we see the neutral to mildly positive category of 50% to 55% moving from 28.2% of total membership over 12 months to 39.8% of membership over 6 months to 55.6% membership over 3 months. This is a clear improvement in performance over this timeline for the category indicating moderate expansion. The stronger expansion category of 55 to 60 shows a membership of 5.6% for all three-time horizons. The category showing weak declines in the 40 to 50 range for diffusion declined steadily from 66.2% over 12 months to 54.6% over 6 months to only 38.9% over 3 months. Over the last three months, fewer than 40% of the reporters were showing mild declines, 55% of the reporters were showing unchanged-to-moderate increases, while relatively larger increases have been posted by 5.6% of the reporters.

Looking back to the right of the table, we can compare the recent 12-month figures to the previous 12-months and to the 12-months before that to get a sense of the smoothed trend. There what we see is the 50 to 55 category three years ago was at 28.2% of the reporting membership; it moved up to 38% of the membership over just a year ago whereas over the past year that membership had slipped to 28% in an environment where tariffs were imposed. Although, as we see from the sequential data, it has over the shorter periods of six months and three months been seeing an increase in membership in that category.

Over the earlier years, there was also stronger membership in the stronger growth category of 55 to 60 percentile. Three years ago, it registered 8.3%, then fell to 6.4% and now sits at 5.6% over the recent 12 months. Over the recent shorter periods of three months and six months, there has yet to be an improvement in that category. As for the weaker category the cohort from 40 to 50%, we see 62% of the membership in that category three years ago, and two years ago that had fallen back to 55.6%, but then over the past year it had moved up to average 66% of the membership: fully 2/3 of the reporting membership over the last year has been in the 40 to 50 the diffusion category though that membership proportion has been falling over the last six and three months.

The grouped statistics show that there is general progress in place and in line with what we see reported in the chart. In addition, we track the number of reporters That are improving period to period. From 12 months to six months to three months, we see that percentage of reporters showing higher diffusion readings steadily improving from 50% to 61.1% to 77.8%. We also track the number of reporters with diffusion below 50 (that is those that are showing contraction) and that number hasn't changed very much; it's at 13 over 12 months and over 6 months while falling only to 12 over 3 months.

However, if we step away from averaging and we look at the raw scores for the last three months, we see the number of countries reporting output that's contracting at 8 in December, at 7 in January and at 6 in February, a clearer sense of progress. Meanwhile, on the monthly timeline, there's also a sense of improvement - not in a monotonic sense – but there is a hint of better general tendency for the percent of reporters that are showing the tendency for higher diffusion to be reported to rise.

The diffusion statistics are up to date, and they basically describe the proportion of the reporters that are seeing activity improve or decline in the reporting area. Diffusion data don’t tell us how strong that improvement is, just whether it's present. Diffusion data tend to be sensitive. They tend to quickly be able to identify changes in trends and right now we're seeing an uptick, an improvement, in the levels of diffusion being reported in this 18-country sample for manufacturing. The results are not decisive, but they are encouraging.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief