Global| Mar 04 2026

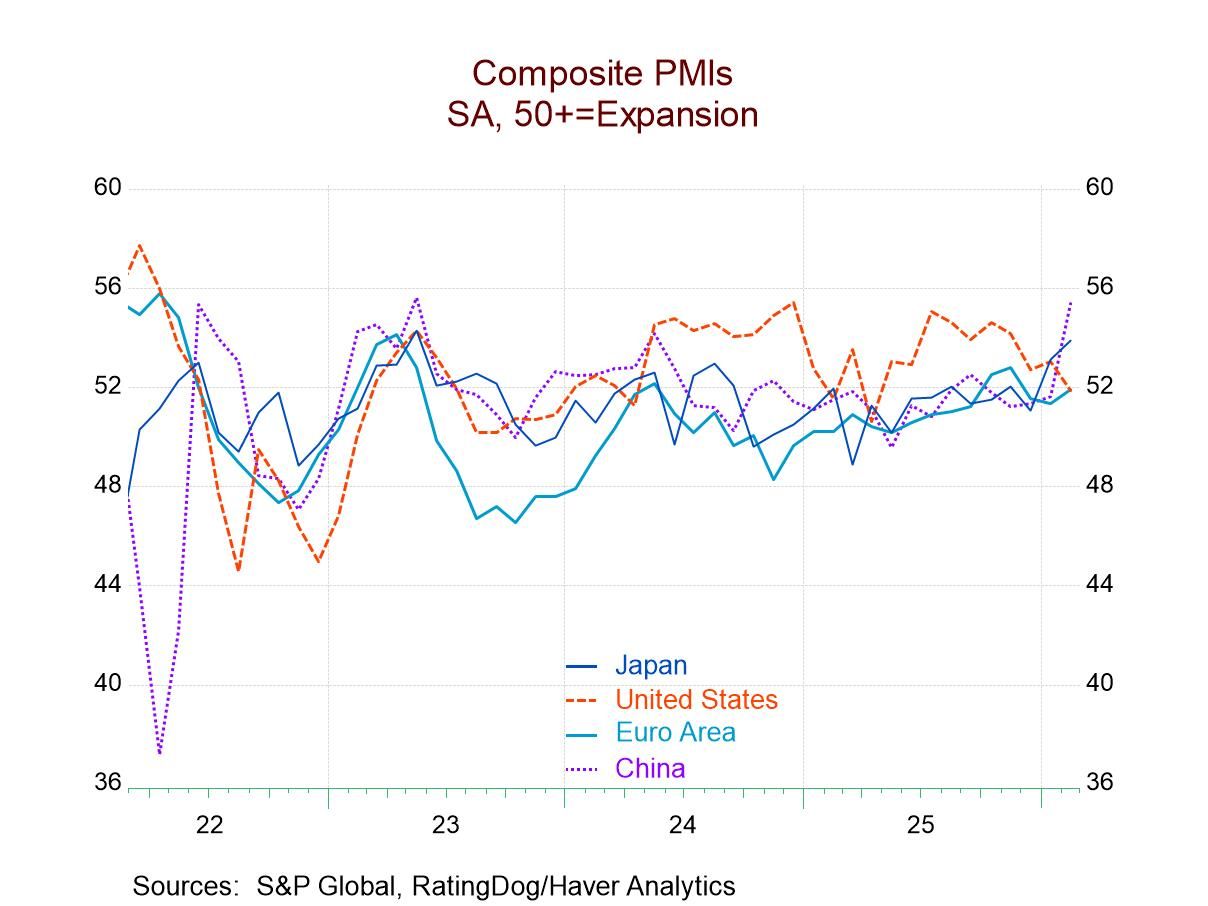

Global| Mar 04 2026S&P Composite PMIs Show Recovery Progresses

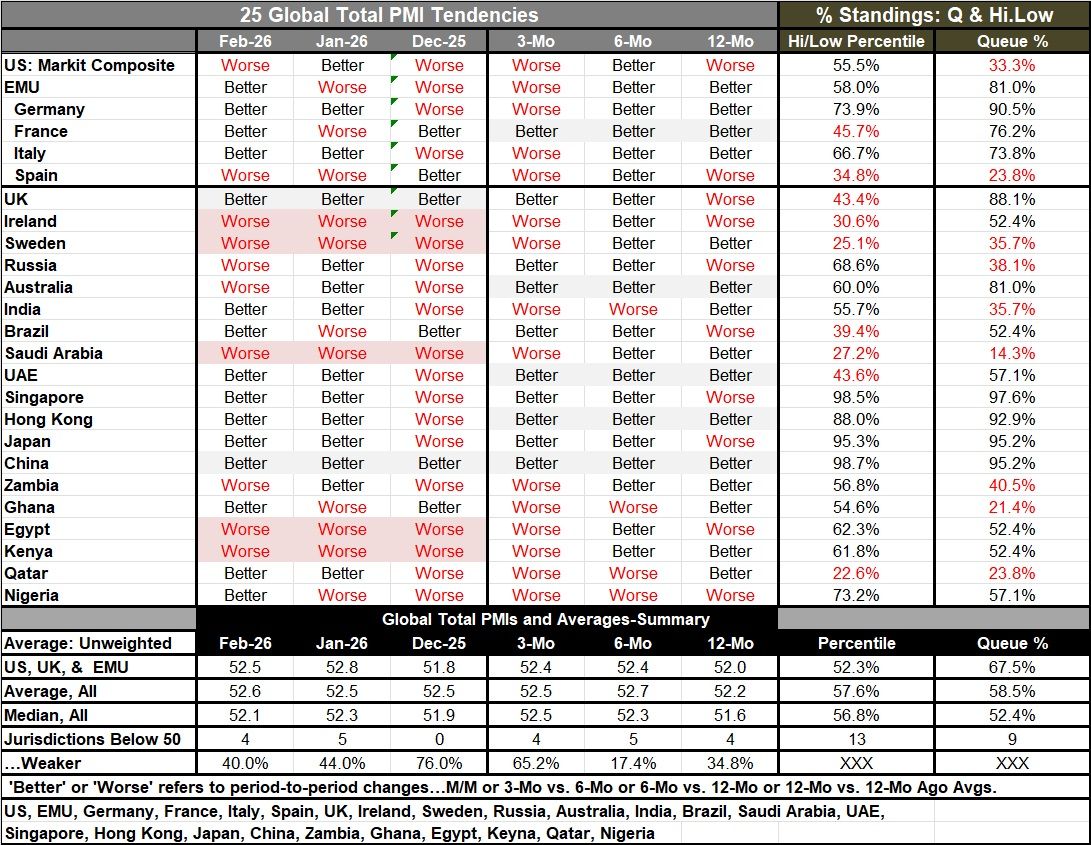

The composite PMIs showed modest increases on their full sample average and a modest step-back in the full sample median calculation in February. However, the number of areas below 50 fell to 4 in February; that count was only 5 in January, and there were none showing declines in December, so there's a great sense of progress in place. The proportion of reporters in February that were getting worse was only 40%, compared to 44% in January and 76% in December. So there has been a change for the better in terms of the proportion of these 25 reporters who are registering better growth month to month in the last two months, in particular.

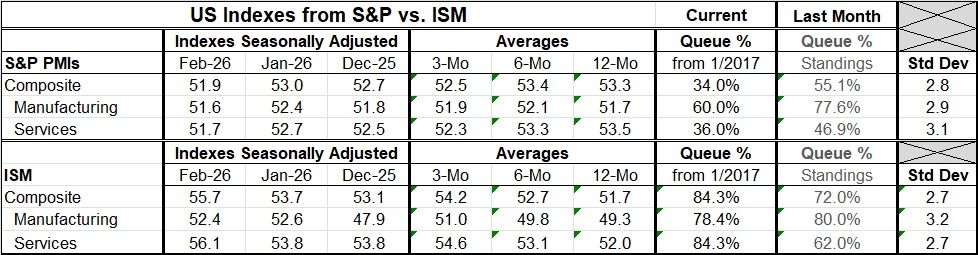

U.S. data are a curve ball to this month’s readings However, the United States, the largest economy globally, also issued a competitor report in the last few days, the ISM. Its manufacturing sector reading made a small step-back in February but is still on a rising trend. The U.S. ISM services index was up strongly in February, a very different reading from that in the S&P (see the comparisons below).

S&P Global data Beyond the monthly data, the sequential data show the full-sample averages getting better from 12 months to 6 months and then slightly weaker from 6 months to 3 months. However, the all-sample median shows an improvement in 6 months compared to 12 months, and another small improvement in 3 months compared to 6 months.

The bottom line on this is that there's a lot of mixed performance, and conditions are broadly in flux; in terms of better or worse, overall conditions are not particularly changed from 12 months to 6 months to 3 months. The monthly data show a better sense that there's progress underway, and this is perhaps a very interesting phenomenon, especially because these are data through February, before the attack on Iran was consummated.

War Intrudes on Economics The execution of war generally isn’t good for economies; however, in this case, the strike was quick, and although there had been a buildup in U.S. armaments—which, in some sense, meant it was expected—the specific timing of the attack was a surprise. It caught Iran completely off guard and made the strike exceptionally successful. Since Iran had lost most of its air cover and its previous war with Israel, its facilities were pretty well laid bare and very quickly the U.S. and Israel claimed air superiority. They have used that to continue to advance their attacks on strategic targets in an effort to achieve the results that the U.S. has said it wants which are (1) to stop Iran's nuclear program, (2) to stop its development of long and intermediate range missiles, and (3) to stop Iran in its role as a sponsor of terror in the Middle East. It may well be that none of these objectives can really be achieved by an air war, and it's not clear that there are any plans to put boots on the ground. However, the air attacks are also aimed at degrading the hold of the ruling party over its citizenry, making it possible for them to rise up and replace the government with one of their choice.

An Untried Strategy This strategy is, as far as I can tell, completely untested. In the past, when a major power interfered in the affairs of a country, it would generally sweep in with the ground attack, make sure that the existing government was fragmented, and basically install the government of their choice even though they would also characterize it as ‘the government of the people.’ This does not seem to be the strategy this time, and it follows more or less the script that the U.S. put in place for Venezuela, where it seized the president who had been sought for various crimes in America and pulled him out of the country. After a brief attack that was necessary to make that capture successful, the U.S. simply left Venezuela behind to settle its own affairs.

Market impact is muted As a result of this unusual tactic, we see some increase in oil prices, but they have not spiked tremendously, and the U.S. is currently offering to provide protection for ships that pass through the Strait of Hormuz. Newspapers report how there is a broadening of the conflict, but I don't see it that way, because it's hard to imagine a war of this nature in the Middle East that wouldn't draw most of the Middle East participants into it as at least collateral damage. What we are seeing is that Iran is desperately trying to shoot at any of its Arab neighbors in an effort to harm them and get them to put pressure on the U.S. to stop its attack. Most recently, Iran launched an ‘attempted attack’ on Turkey, which is a NATO member. But there doesn't seem to be much chance that the actual hostilities are spilling out of the Middle East or that Iran has much of a reach to do more than what it's been doing; its capabilities seem to be narrowing every single day.

Where the PMI Data Stand The PMI data for February also showed that only nine of the twenty-five members have queue percentile standings of their composite indexes that are below the 50% mark, indicating there was economic contraction in play. Quite a number of countries are showing queue percentile standings of their composite PMIs that are above their 70th percentiles. And we want to take these totals with a grain of salt partly because the U.S. has just reported out such strong data.

Summing up On balance, it appears that the war being conducted in Iran has caught the global economy on a bit of an economic upswing, and we'll have to see to what extent that is affected or interrupted by the conduct of war, especially since this combat appears to be so well contained. A number of analysts talk about how this war is increasing uncertainty in the area. In my opinion, this is a knee-jerk improper reading of the situation. It seems to me that a successful attack that successfully reduces the impact of Iran in the Middle East as a sponsor of terror, as the developer of a nuclear program, and as a possessor of long range and intermediate range missiles—and that creates the potential for a different civilian government to take over—has actually increased certainty - and the prospect of peace - quite a lot. The view that uncertainty has been elevated is an extremely short-term view that I think will quickly be dominated by the notion that uncertainty has actually been reduced and that world conditions have been improved.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief