Global| Aug 19 2025

Global| Aug 19 2025Powering Prosperity: Why the UK Has Been Falling Behind

by:Andrew Cates

|in:Viewpoints

Energy is not just another input into an economy — it is the foundation on which productivity, competitiveness, and long-term growth rest. The capacity to generate abundant, reliable, and affordable electricity underpins industrial strength, attracts investment, and enables technological transformation. Where these conditions are met, economies flourish; where they are absent, the result is stagnation.

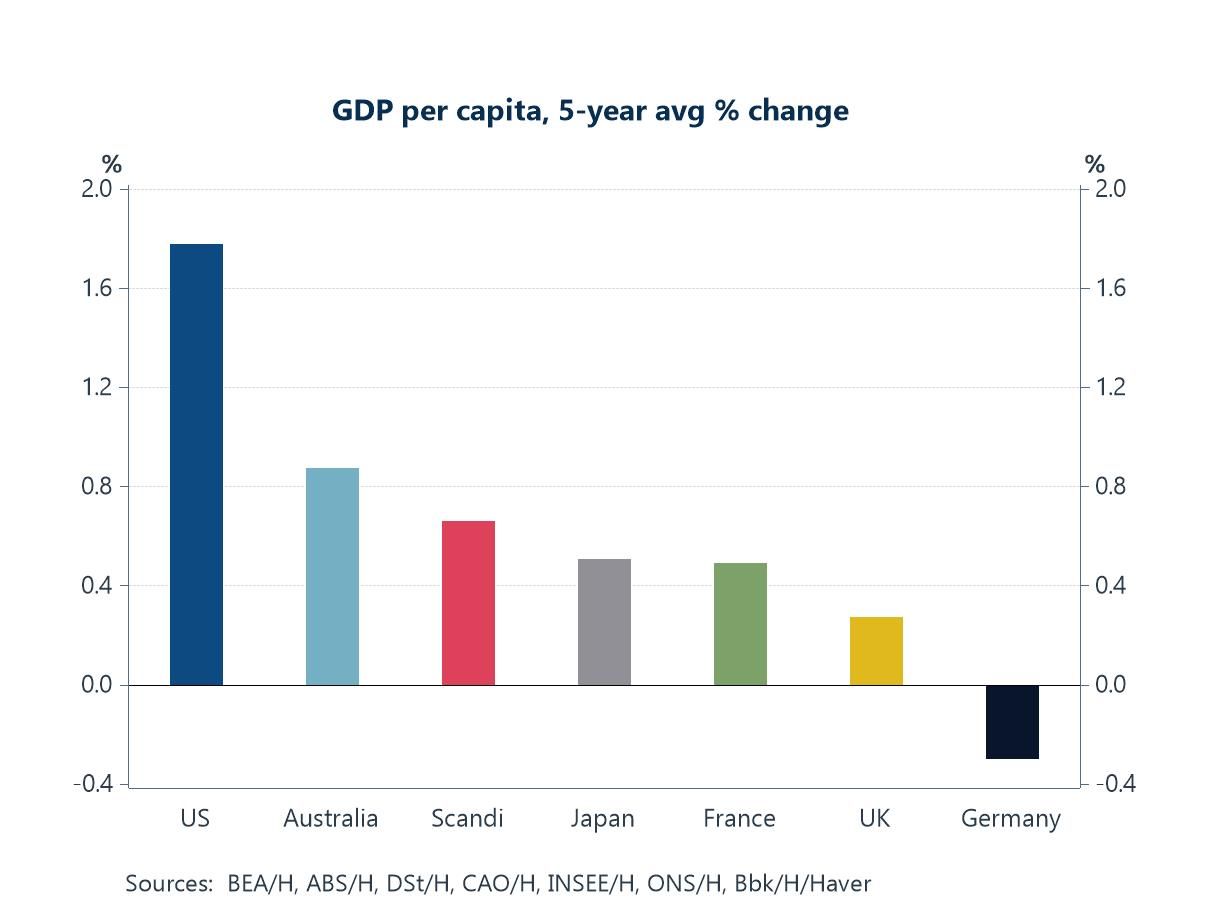

That is why the UK’s dismal record on per-capita GDP growth over the past five years — one of the weakest among advanced economies — cannot be understood without reference to its electricity system. High prices, declining per-capita generation, and an energy mix that has failed to replace retiring firm capacity with equally reliable low-carbon alternatives have eroded competitiveness. By contrast, the United States has combined low electricity prices with high and stable per-capita generation, giving it a structural advantage in attracting energy-intensive industries and supporting the AI- and manufacturing-led investment boom.

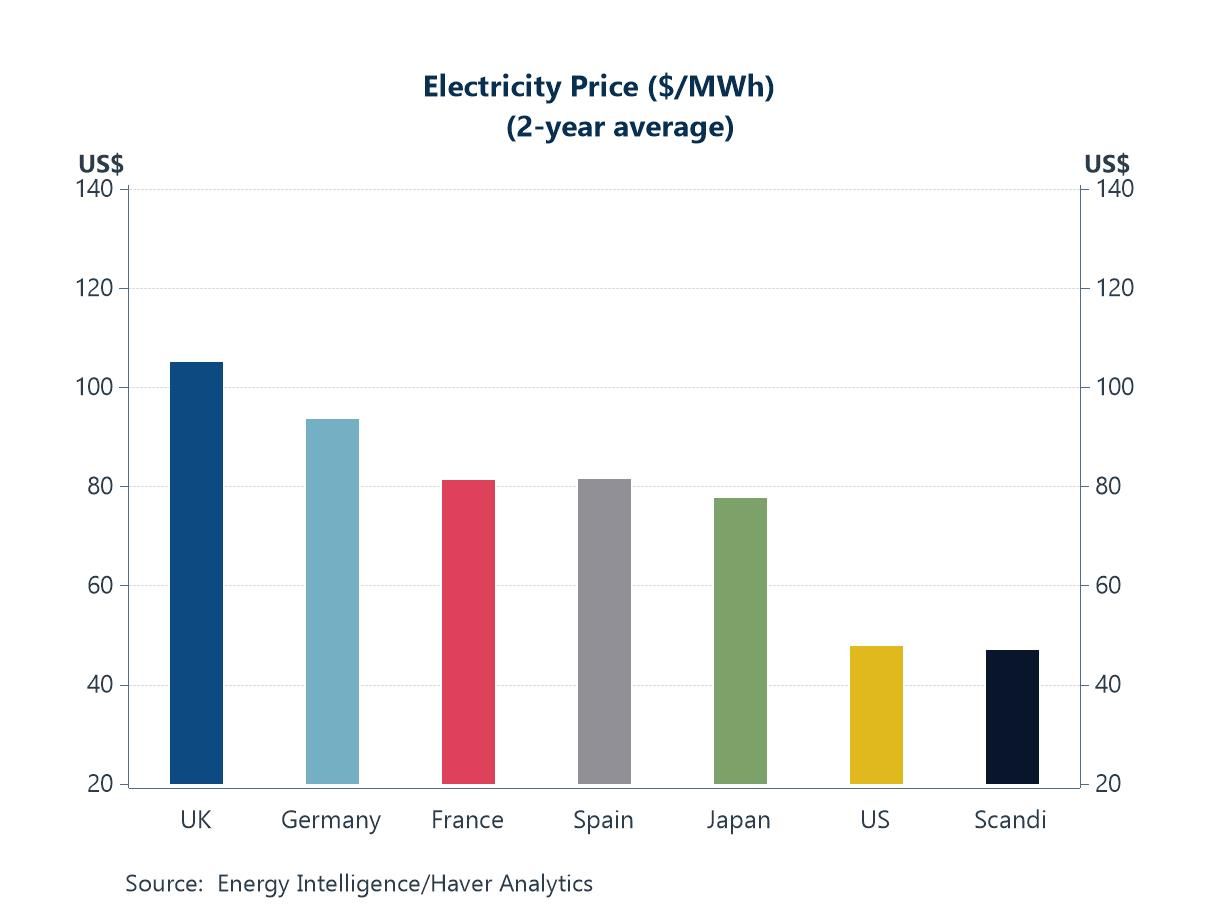

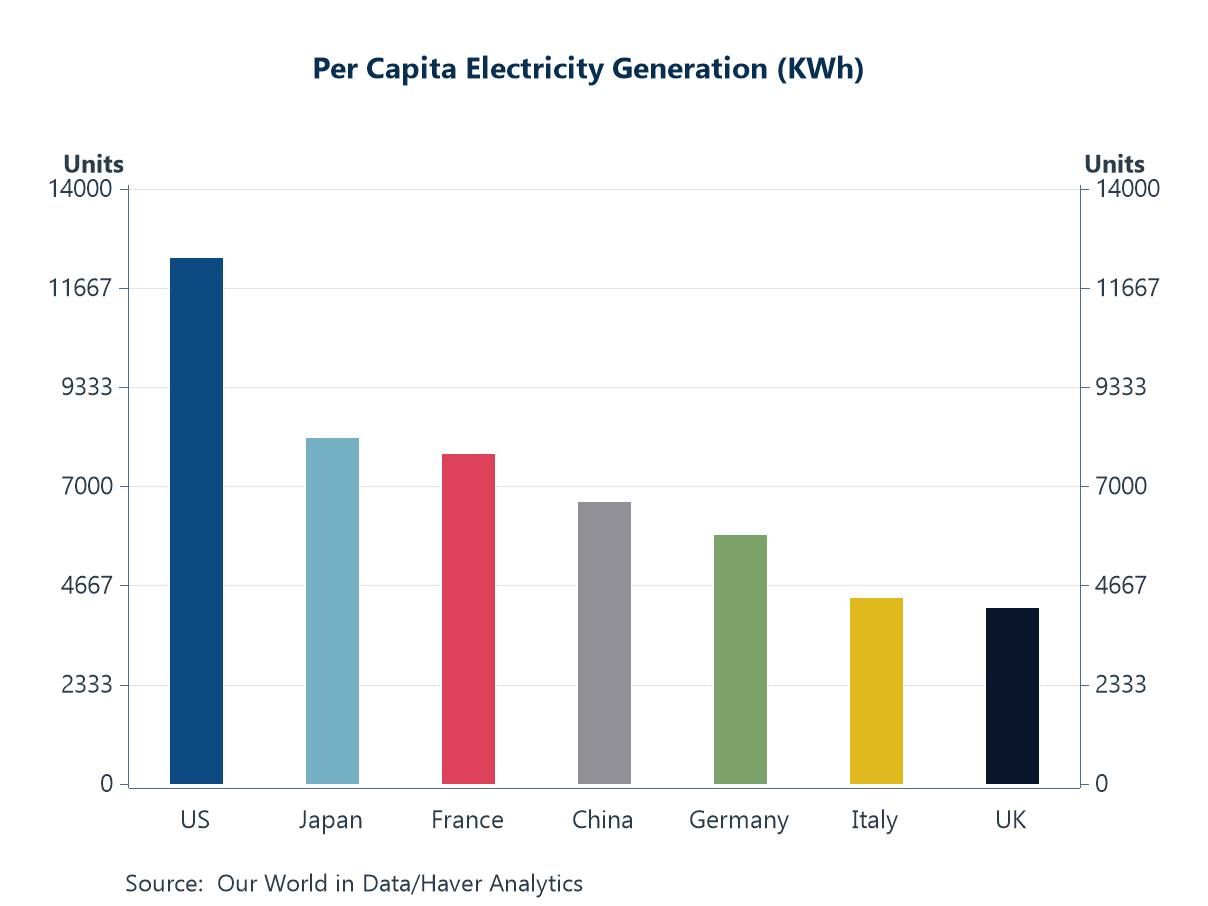

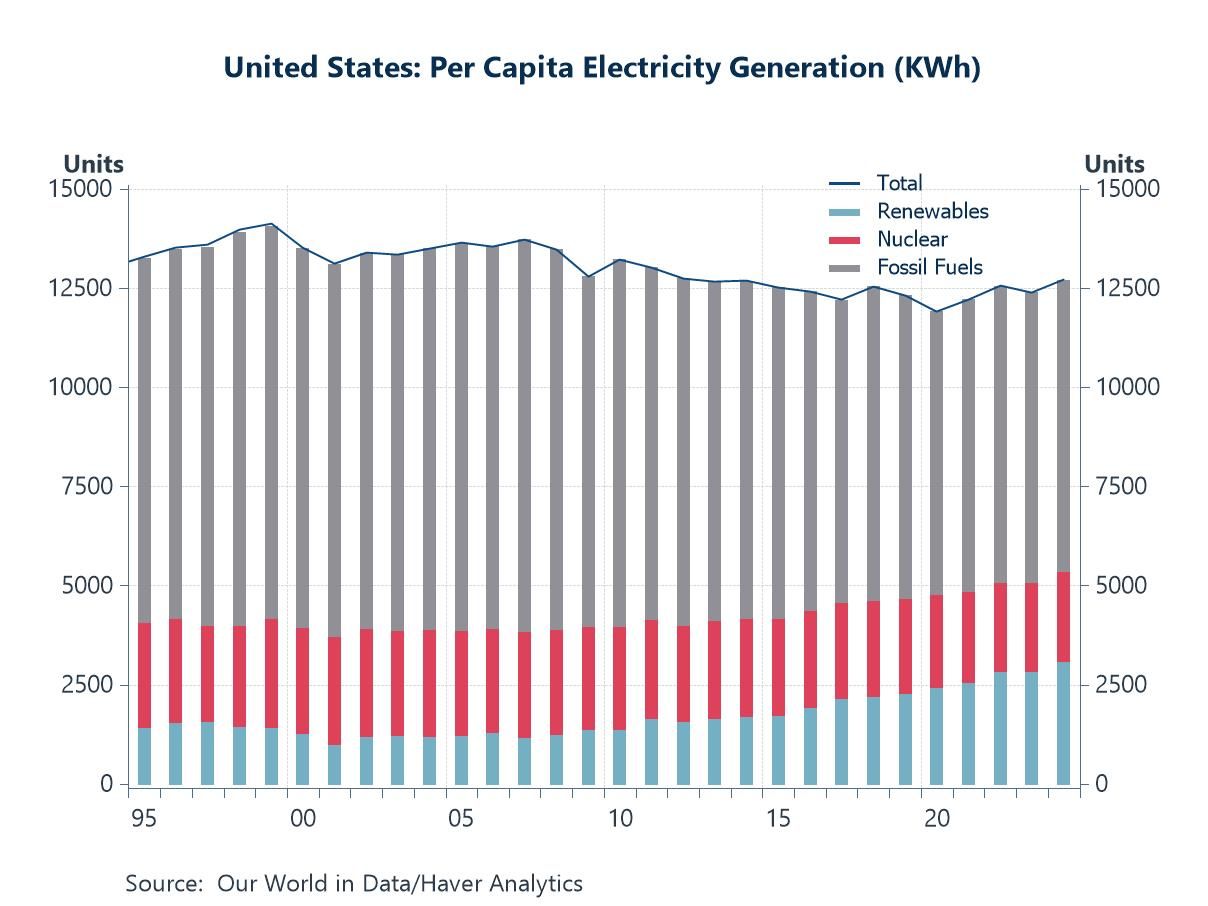

The evidence in the numbers Recent data show the UK languishing near the bottom of the G7 for per-capita GDP growth, while the US leads comfortably. Electricity prices tell part of the story: in the UK, wholesale prices have averaged among the highest in the developed world over the past two years, while US prices are less than half as high. The gap in per-capita generation capacity is equally stark — US output per person is nearly three times higher than the UK’s.

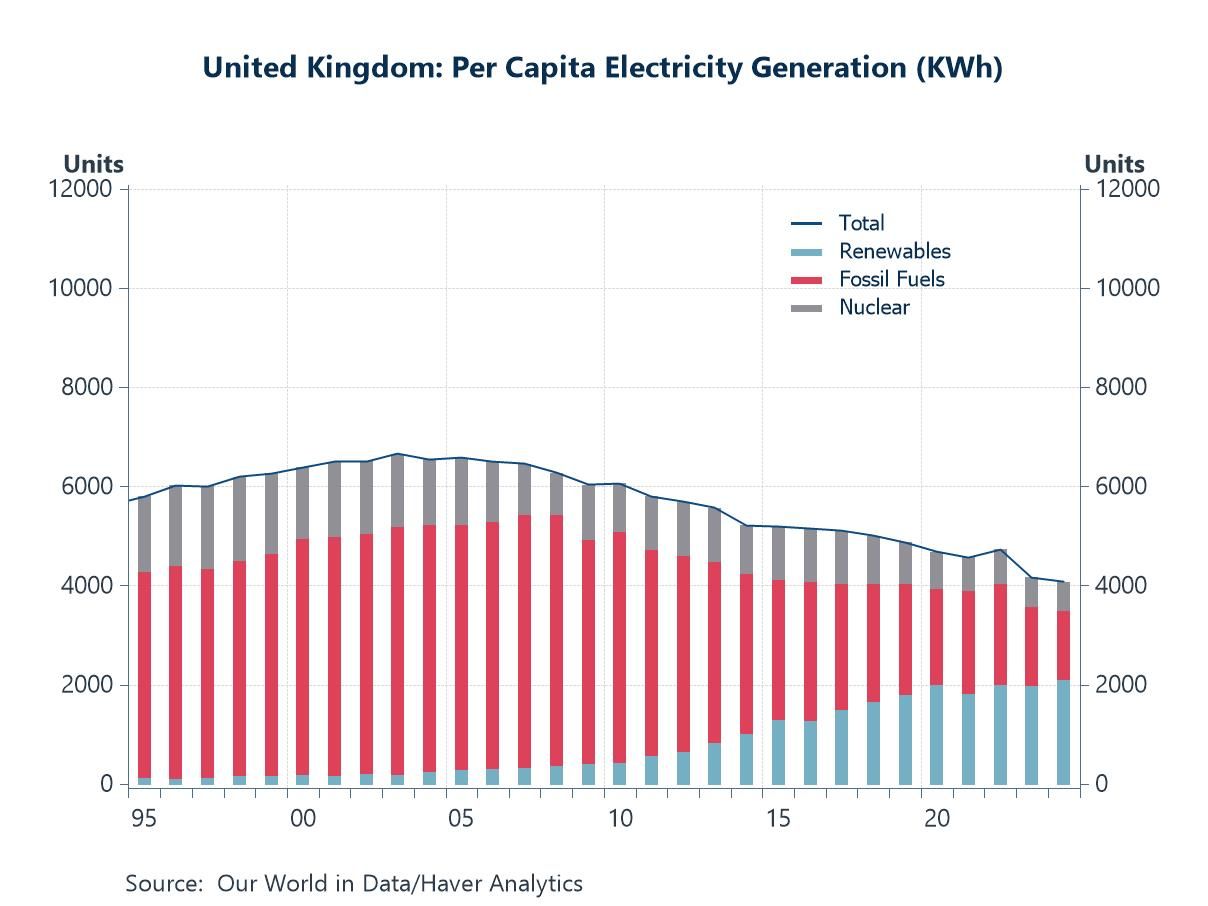

These differences reflect deep-seated structural weaknesses in the UK system. Domestic generation per capita has been in steady decline since the early 2000s. Ageing nuclear plants have been retired without timely replacements; the coal exit has removed dispatchable baseload; and although renewables have expanded rapidly, they lack sufficient firm low-carbon backup or storage to guarantee supply. Grid constraints, planning delays, and policy inconsistency have compounded the problem, pushing up costs for households and industry alike.

The consequences go beyond manufacturing. In AI, for example, the US leads in hyperscale data-centre capacity and high-performance computing installations — both voracious electricity users. This creates a powerful feedback loop: abundant, affordable energy supports technological leadership, which in turn attracts further investment and strengthens long-term competitiveness.

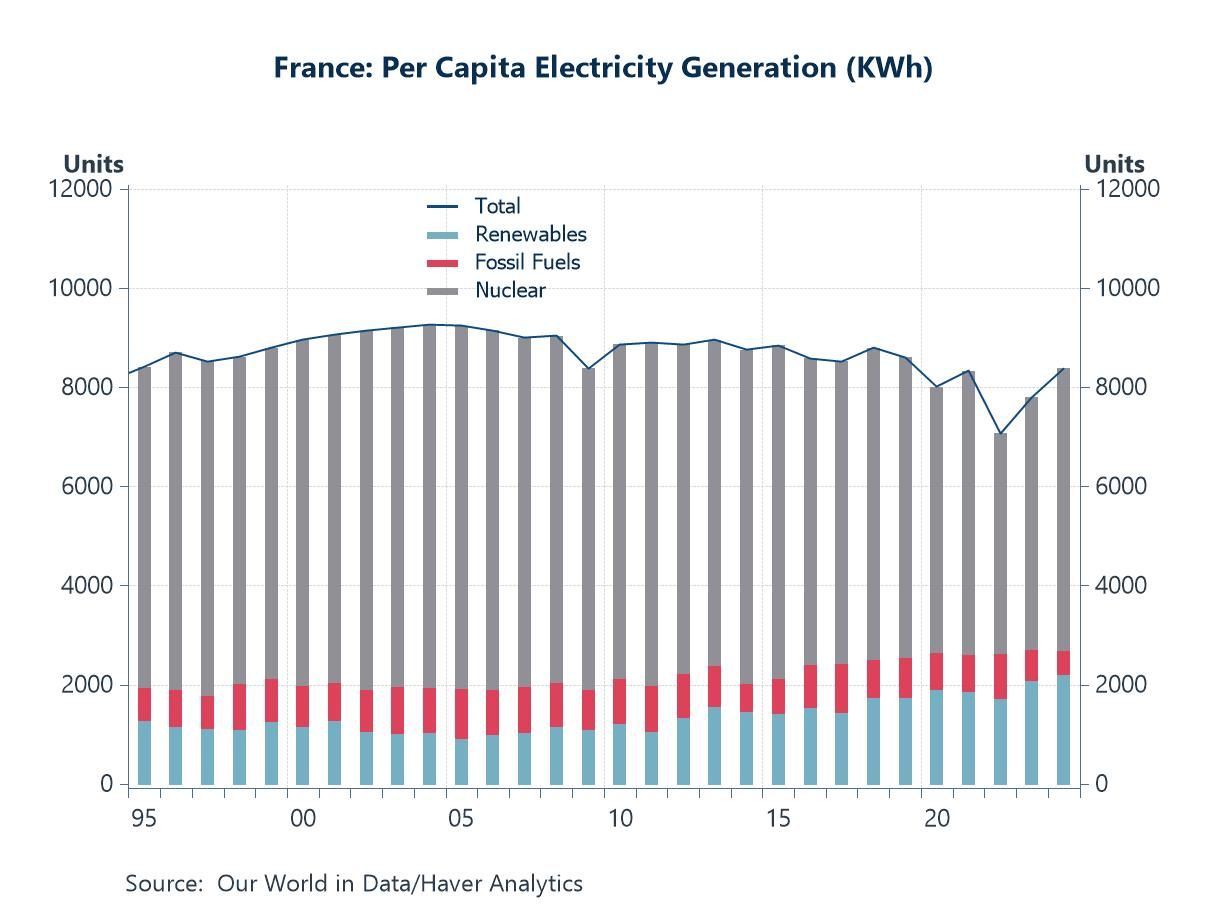

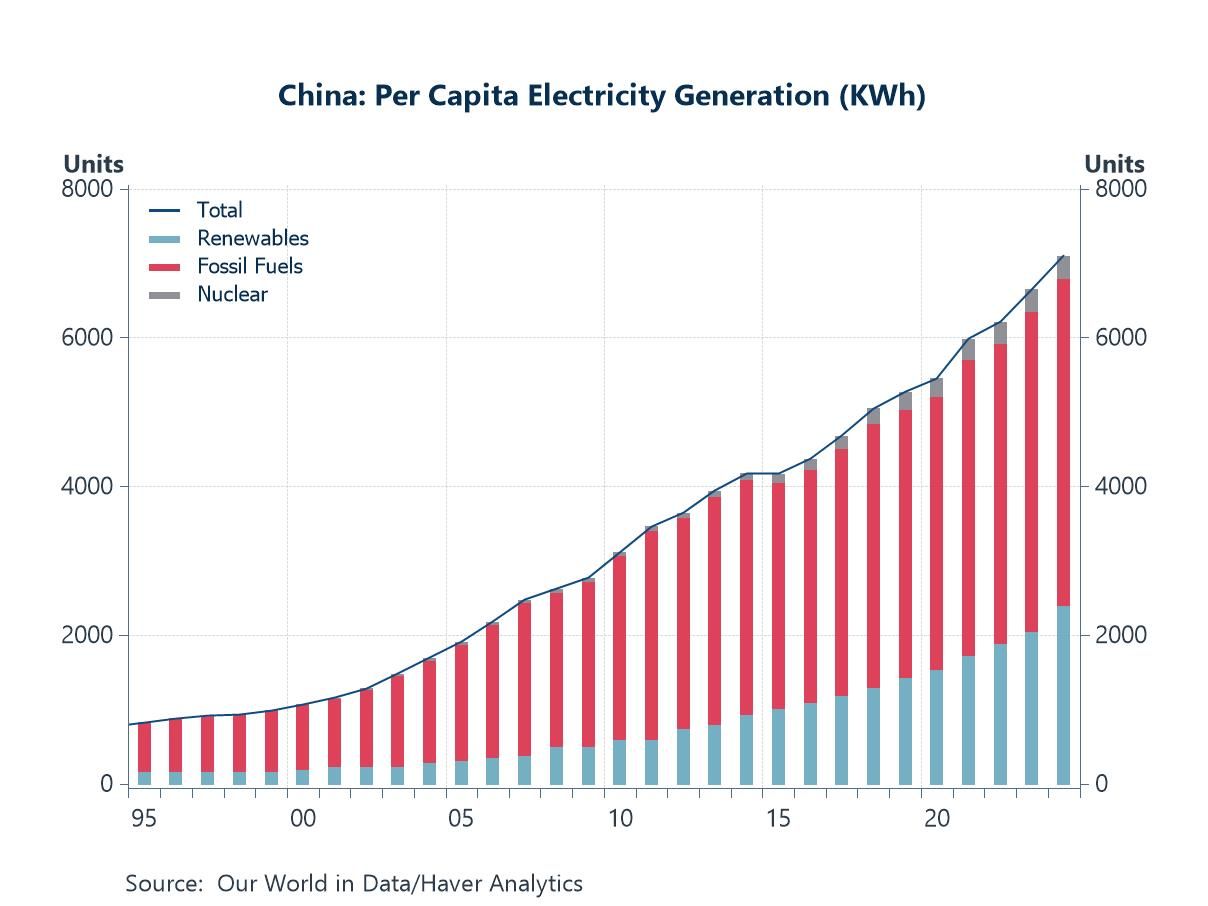

Contrasts abroad United States: The US benefits from a large, diverse generating fleet — nuclear, renewables, and abundant domestic gas — that keeps prices low and capacity high. This underpins the economics of data centres, semiconductor fabs, and electrifying industry. Long-dated incentives under the Inflation Reduction Act and state-level reforms have encouraged private capital to expand capacity further. The result is not just energy security but an enduring cost advantage that strengthens the country’s relative growth position. France: A high share of nuclear generation delivers firm, low-carbon power at scale. Outages have been a temporary drag, but the system remains one of Europe’s most competitive, offering a template for combining decarbonisation with reliability. China: Policy has prioritised overbuilding capacity — fossil and renewable — to ensure electricity is never a binding constraint on growth. Large-scale transmission build-out and rapid renewable deployment are reshaping the mix while sustaining industrial momentum. Germany: A cautionary tale. The nuclear exit, over-reliance on imported gas, and rapid renewables expansion without adequate backup have produced high prices and reduced competitiveness.

The UK’s competitiveness challenge The UK’s combination of high prices and declining capacity is more than an energy problem — it is an economic strategy problem. Energy-intensive industry faces a structural disadvantage. The digital economy, from AI to electrified transport, is constrained by a system that is neither as reliable nor as cost-effective as its global peers. Without a decisive shift in policy — prioritising firm low-carbon generation, accelerating grid investment, and reducing volatility in industrial energy costs — the UK risks further entrenching its underperformance.

Conclusion The charts make the relationship between energy and growth hard to ignore: the US leads on both, the UK trails on both. Electricity is not a sector in isolation; it is the backbone of economic competitiveness. Countries that ensure abundant, affordable, and low-carbon power will lead the next phase of global growth. Those that fail to do so will be left explaining — as the UK is now — why their economies are stuck in the slow lane.

Andrew Cates

AuthorMore in Author Profile »Andy Cates joined Haver Analytics as a Senior Economist in 2020. Andy has more than 25 years of experience forecasting the global economic outlook and in assessing the implications for policy settings and financial markets. He has held various senior positions in London in a number of Investment Banks including as Head of Developed Markets Economics at Nomura and as Chief Eurozone Economist at RBS. These followed a spell of 21 years as Senior International Economist at UBS, 5 of which were spent in Singapore. Prior to his time in financial services Andy was a UK economist at HM Treasury in London holding positions in the domestic forecasting and macroeconomic modelling units. He has a BA in Economics from the University of York and an MSc in Economics and Econometrics from the University of Southampton.