Norway: Output Advances in January

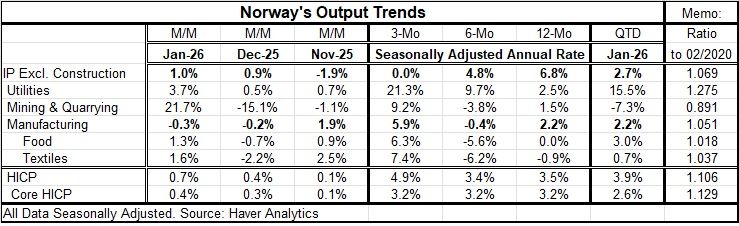

Industrial output in Norway rose by 1% in January after gaining 0.9% in December. Utilities output rose briskly, mining and quarrying output rose extremely sharply, while manufacturing output showed its second decline in a row.

The sequential growth rates show that the headline series for industrial production is decelerating, with nearly 7% growth over 12 months, nearly 5% growth over six months, and the growth over three months is down to zero.

On that same progression, utilities output has accelerated from 12 months to six months to three months, while mining and quarrying has a more complicated pattern—rising 1.5% over 12 month, falling at a 3.8% pace over six months, then rising at a 9.2% annual rate over three months.

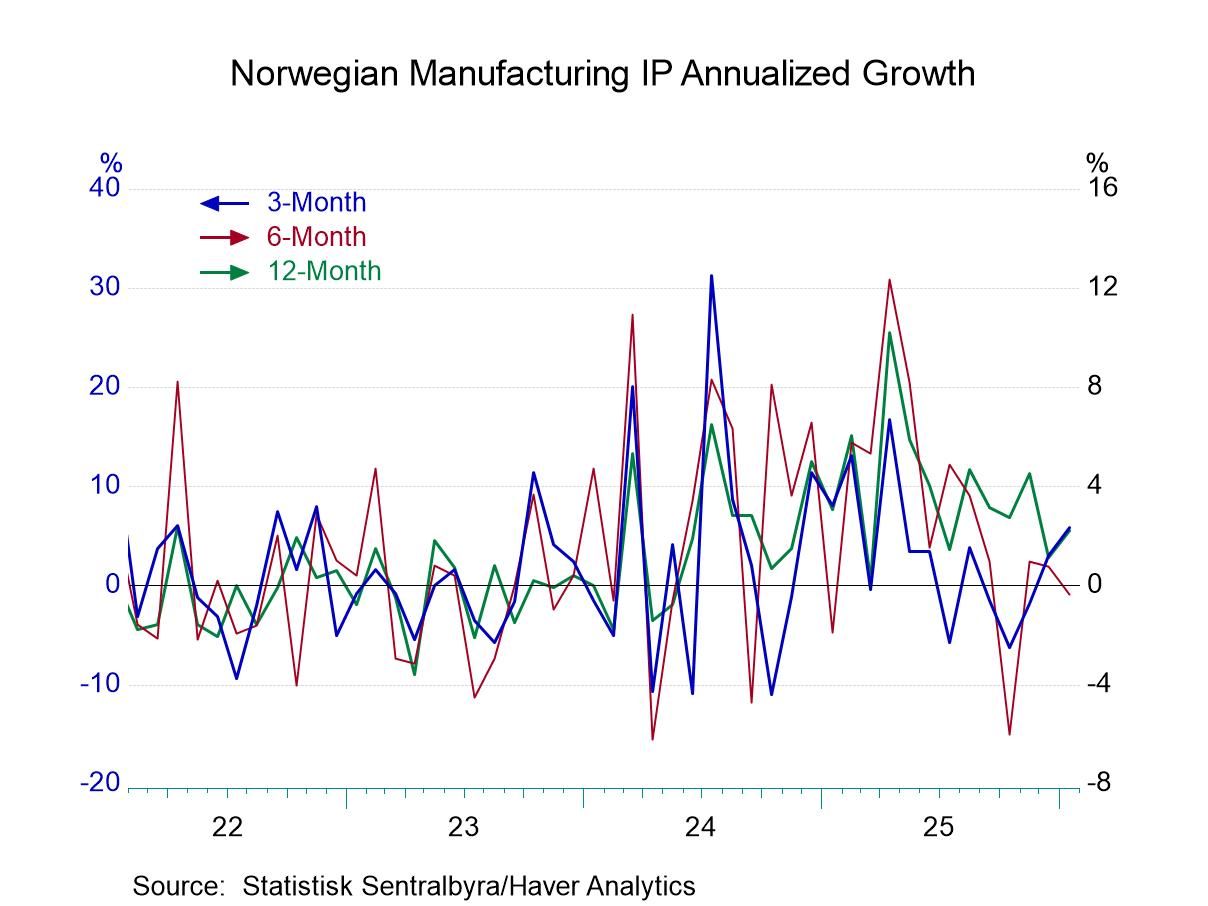

In manufacturing, the trends are also complicated but with an upbeat ending. Manufacturing output is up by 2.2% over 12 months; the growth rate shows a decline, falling at a 0.4% annual rate over six months, with output then picking up and growing at a 5.9% annual rate over three months. Despite the setback in the middle, manufacturing has a positive year-over-year growth rate and shows strength over three months. This pattern is followed by food and also by textiles, with the exception that textiles are still showing a year-over-year decline of 0.9%. However, textile output is now growing briskly at a 7.4% annual rate over three months.

Norway is also experiencing a pickup in inflation. Its HICP inflation rate is 3.5% over 12 months, stays pretty much there with a 3.4% annual rate over six months, and then jumps up to a 4.9% annual rate over three months. However, that acceleration is tempered by a core inflation rate that is unchanged at 3.2% in each horizon. These growth rates are still excessive, with the central bank having a target of 2%; however, the inflation rate isn't getting any worse.

The industrial pattern for Norway is somewhat complicated by the fact that the headline measure for industrial production is showing a clear deceleration, while manufacturing is showing a more complicated pattern with some near-term acceleration over three months.

And for the quarter to date, which is a nascent comparison since the data are only available through January, we have overall industrial production growing at a 2.7% annual rate and manufacturing growing at a 2.2% annual rate. The quarter also shows inflation flying at a 3.9% annual rate, although core inflation is more tempered at a 2.6% annual rate pace.

Policy Choices Norway's policy choices are a little bit complicated, with inflation being undesirable, manufacturing showing growth pushing ahead but perhaps not in a strong enough fashion to be dependable, while overall industrial output is showing a tendency to slip. With global economic conditions being touch and go given the new developments in the Middle East and a likely push-up in inflation from oil prices, it will be important to watch the central bank and see what choices it makes—and whether it thinks it can look through the oil price increase that we're going to experience or whether it's time to put the hammer down on inflation.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global