Global| Jul 01 2026

Global| Jul 01 2026Mixed but Broad Backtrack in Global Manufacturing in June

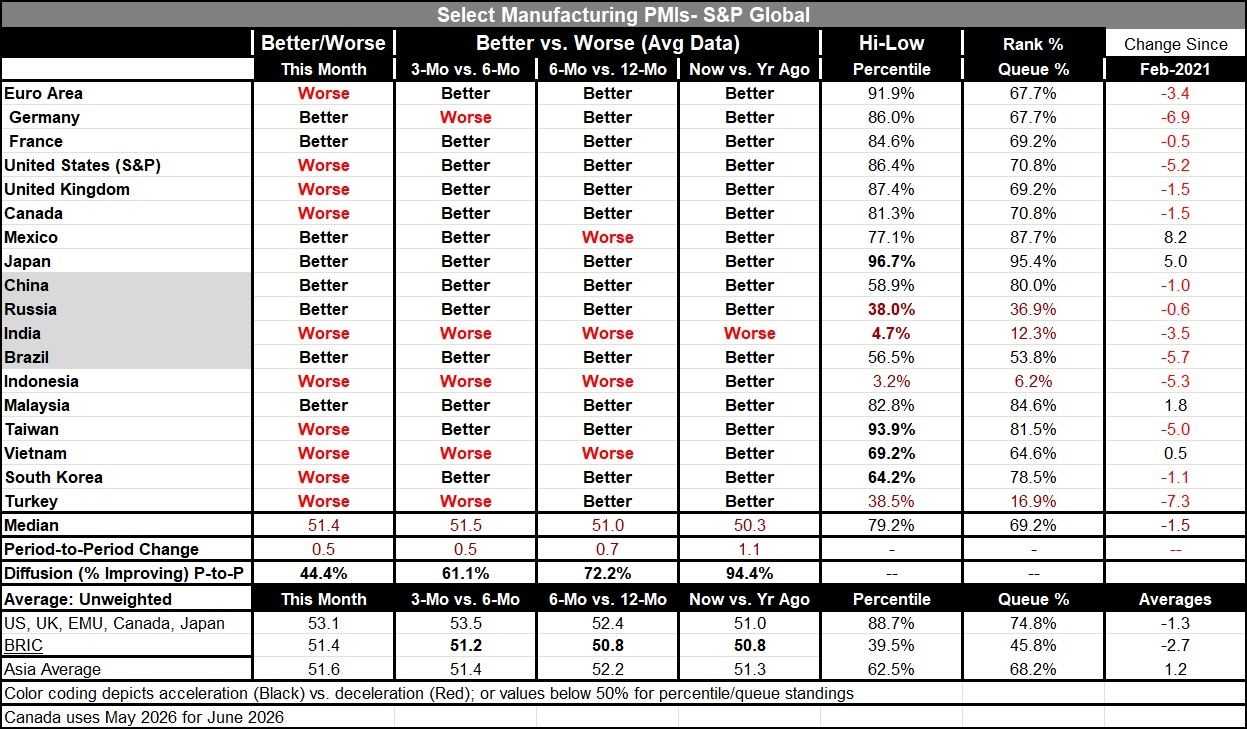

The manufacturing PMI values for June showed more worsening than improving, with 10 of 18 reporters showing conditions unchanged or getting worse on a month-to-month basis. However, taking into account the size of the changes across the various reporters, the median PMI rating for manufacturing in June improved to 51.4, an increase of 0.5 points from the month before. The month-to-month deterioration is relatively broad; however, it's also relatively mixed, and when taking the size of the changes into account, there's actually a monthly improvement.

The chart shows that manufacturing has been undergoing improvements generally since late last year, although in the last few months, there has been a topping, a capping, and in some cases a backtracking from the recent high readings. That action reflects the onset of hostilities between the United States and Iran and the on-again, off-again situation with the Strait of Hormuz being open or closed.

Over three months compared to six months ago, the average readings show deterioration in only 5 of 18 reporters. This clearly reflects what we see in the chart, which is a recent improvement over three months compared to six months. The next comparison of 6-month averages to 12-month averages finds that only four reporters are worse off over six months than they were over 12 months. Those four are Mexico, India, Indonesia, and Vietnam. Over 12 months compared to 12 months ago, conditions are better everywhere except in India.

In addition, we can evaluate the manufacturing performance by ranking the current month's observation in a queue of data back to January 2022, a period of about 4½ years. Viewed over that span, only four countries have readings in June below their period medians. Those are Indonesia, India, Turkey, and Russia. All the rest have readings above the 50th percentile, putting them above their historic medians. Japan has an exceptionally strong reading in June relative to its history, posting a 95.4 percentile standing. Mexico, China, Malaysia, and Taiwan also post strong standings, in their 80th percentile.

The median queue standing for the entire group is a 69.2 percentile standing, which is still quite strong. Other summary measures of sequential diffusion show that the proportion of reporters improving over 12 months is 94.4%, compared to 72.2% over 6 months and 61.1% over 3 months. The breadth of this improvement is shrinking over the near-term horizons; however, the tendency for improvement is unmistakable.

Average readings for certain groups at the bottom of the table show that the United States, the United Kingdom, EMU countries, Canada, and Japan, on an unweighted basis, have steady improvements in place from 12 months to six months to three months, with a one-month reading even stronger. The BRIC countries have readings that are marginally stronger but are staying in a tight low range around 50.8 to 51.5. The Asian average shows an improvement from 12 months to 6 months and then backtracking, with the current 3-month diffusion values just slightly above 51, around 51.5.

The global economy has shown some significant improvement recently in the manufacturing sector, and this has occurred despite the ongoing war in Ukraine and stepped-up hostilities involving Iran, including the on-again, off-again closure of the Strait of Hormuz. Oil prices have spiked and have since come down substantially. However, the outlook for peace remains clouded as both sides continue to talk positively about an agreement and a ceasefire, then turn around and violate near-term conditions they have set. This makes it very difficult to handicap the future.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief