Large EU Economies Show Some Inflation Cooling

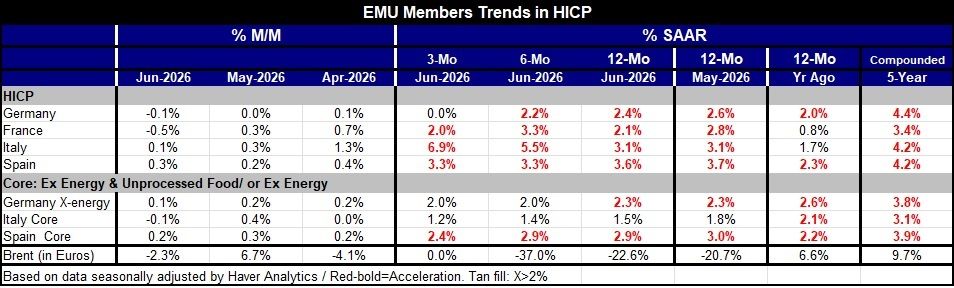

Some inflation progress, but not enough: The headline HICP in June for the largest monetary union economies have largely broken lower, with the exception of Spain. The German headline HICP fell by 0.1% in June after being flat in May. In France, the price index fell by 0.5% in June after growing by 0.3% in May. In Italy, the June index rose by 0.1% after rising by 0.3% in May. In Spain, June brought a 0.3% increase after a 0.2% increase in May.

Core or ex energy (Germany): The core inflation readings are available for Germany, Italy, and Spain. In the case of Germany, it's an index excluding energy only. June brought a 0.1% increase for the German index, a - 0.1% decline for Italy's core, and a 0.2% increase for the core in Spain. On balance these are a good collection of results from the standpoint of the ECB that has an inflation target of 2% for the whole of the European Monetary Union, but no guidance for individual countries.

Sequentially: Sequentially the headline inflation rate shows progress in Germany and France while excesses are stubborn in Italy and Spain. Over 12-months, all the inflation rates are excessive, but France is only technically excessive, and probably acceptable at 2.1% year-over-year. Germany's increase over 12-months is 2.4%, Italy's is 3.1%, and Spain’s is 3.6%. The progression of inflation from 12-months to 6-months to 3-months shows accelerations over 6-months compared to 12-months for France and for Italy with decelerations in Germany and Spain. But Spain's 6-month inflation rate is still 3.3%, Germany has dropped down to 2.2%, France is at 3.3% with Italy jumped up to 5.5%. Over 3-months the German headline inflation rate is zero, and in France it's down to 2% but in Italy the headline pace is up to 6.9% and Spain is at 3.3%. These are all compounded rates of change over three months.

Three-month trends are mixed: And none of this is really surprising since oil prices have been surging over the period oil is only starting to decline. Over 12-months the oil price is down by 22%, over 6-months it’s down by 37% at an annual rate and over three months the oil price is flat. Much of this price action is still very recent. And this is for Brent crude measured in euros. Over three months we see German inflation is flat for the headline HICP while, in France, the inflation rate is down to 2%. In Italy, the 3-month pace is 6.9%; in Spain it’s at 3.3%. Headline inflation still has a somewhat erratic performance over 3-months although it's quite acceptable in Germany and France and quite not acceptable in Italy and in Spain.

Core inflation is lower but still too high: Core inflation shows a lot more moderation because the behavior of energy prices leaves core inflation largely unaffected. If the core is affected, it's only after a more substantial. When there have been knock on effects from other industries German x-energy inflation it's 2.3% over 12-months and then settles down to a 2% pace at an annual rate over 6-months and 3-months. Italian core inflation is golden on all three periods at 1.5% over 12-months, down to 1.4% over 6-months, and down to 1.2%, over 3-months Spain's core inflation is excessive and while it is making progress toward something that is more agreeable from a European standpoint over 12-months Spain’s core inflation is 2.9%, it sticks at 2.9% over 6-months, then drops to a 2.4% annual rate over 3-months.

Policy: The ECB has already started to raise rates and warned that there could be more ahead, depending on circumstances. However, we are seeing signs here that inflation is beginning to behave particularly for the core, and we could see the headlines improve more dramatically if oil prices continue to drop as they have been. Growth in the European area has been mixed on the continent; in the United Kingdom growth is showing signs of weakening as the inflation rate in the UK has dropped rather sharply.

Outlook: The outlook is still guarded. There continues to be a war in Ukraine unsettled conditions in the Middle East including concern over the Strait of Hormuz where Iran continues to say that it wants to be in control of traffic through the Strait, something that doesn't seem to be likely to be palatable to the US although time will tell what kind of deal if any emerges from that conflict. Inflation developments are going to depend importantly on what happens with oil and how open the strait becomes. As we can see here Germany and Italy already present relatively controlled core inflation rates. The rest of the monetary union should follow suit as all prices should continue to behave and follow oil prices lower. It has been a long period with inflation misbehaving. The core and X-energy inflation statistics show us that over the last five years Germany has had a compounded X-energy inflation rate of 3.8%, Italy 3.1%, and Spain 3.9%. These are readings excluding energy and over that five-year period. Oil and energy are not the only price concerns. Energy prices had a compounded annual rate increase of 9.7% over the last five years. Monetary policy has gotten far behind where it's supposed to be and has allowed prices to rise far more than they should have. Central banks have got to pay a little more attention to hitting their inflation targets in the future; they can't keep missing to this extent and convince anybody that they have a viable credible inflation target at 2%.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Asia

Asia