Japan’s IP Is Fighting Off Weak Trends

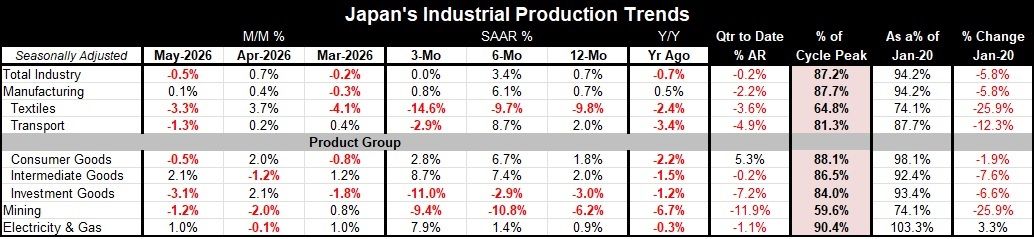

Industrial production in Japan fell by 0.5% in May after rising by 0.7% in April and declining by 0.2% in March. Manufacturing output rose by 0.1% in May after rising by 0.4% in April and declining by 0.3% in March. Total industrial output shows a 0.7% gain over 12 months, a 3.4% annual rate gain over six months, and zero change in output over three months. For manufacturing, 12-month output is up 0.7%; over six months, output is up at a 6.1% annual rate; and over three months, output is up by 0.8% at an annual rate.

These trends show that output continues to grow for manufacturing as well for total industry, but not by a great margin. In fact, there are still a number of industries still fighting off negative trends, such as textiles, where output falls over three months, six months, and 12 months, as well as investment goods and mining, both of which show declines over three months, six months and 12 months. One year ago, all of these sectors were showing year-over-year declines except for manufacturing, which was up by 0.5% over 12 months. Manufacturing output is now up by 0.7% year-over-year, with consumer goods up by 1.8%, intermediate goods output up by 2%, and investment goods falling by 3%. Japan is currently trying to fight off a legacy of weakness. The strength of the rebound is being borne by consumer goods and intermediate goods, with investment goods undergoing significant contractive effects.

Manufacturing is showing gains on all three sequential horizons. Utilities output is showing growth on each horizon, and actually shows gathering strength, rising by 0.9% over 12 months, at a 1.4% annual rate over six months, and at a very strong 7.9% annual rate over three months.

In the quarter-to-date (QTD) basis, most of these sectors are losing the battle against weakness, with most industry or sectors showing declines two months into the new quarter. Overall output declines at a 0.2% annual rate. Manufacturing output falls at a 2.2% annual rate, intermediate goods output falls at a 0.2% annual rate, and investment goods output falls at a 7.2% annual rate. The only exception is consumer goods output, which is rising at a solid 5.3% annual rate, but that's not strong enough to drag all of industrial output or even manufacturing into the plus column.

Manufacturing output currently is at about 87.7% of its past peak. Activity in electric and gas utilities are at 90.4% of their past peak, while mining is only at 59.6% of its past peak of activity. Comparing levels of output to where they were in January 2020, manufacturing is at 94% of that value, with total industry also at 94% of that value. Consumer goods are at 98% of that value, intermediate goods at 92%, and investment goods at 93%. Mining is only at 74% of its January 2020 value, while electric and gas utilities have moved beyond the January 2020 level and are 3.3% higher than they were and early 2020.

Since 2020, it has been a relatively difficult time for the global economy. The Japanese statistics show only one sector that has managed to create positive growth compared to its level in January 2020. The current month is a mix of plus-and-minus activity changes. Sequential trends generally show more positives than negatives, but there are still a lot of negatives in train that keep Japanese manufacturing from reaching clearly solid footing. When the Strait of Hormuz opened, it appeared that Japan would be in a position to build on its recovery, but now, with the failed peace agreement and failed ceasefire, the strait once again has been closed and the outlook is shrouded in negativity.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Asia

Asia