Japan: A Resilient Cycle Amid Structural Change

|in:Viewpoints

We remain overweight Japanese equities and view the recent market correction as a buying opportunity. The macro backdrop remains constructive: business cycle indicators are firm, corporate profitability is strong, and there are no major systemic risks. Any economic slowdown is likely to be temporary and should be looked through rather than feared.

Business cycle signals reinforce this view (Figure 1). Profit and investment cycles are clearly in an upswing, while borrowing costs remain well contained. The two-year real lending rate, though rising, sits comfortably within its historical range, indicating that the cost of capital is not restrictive. Credit growth is broadly aligned with economic expansion, with signs of strengthening private sector demand. The only soft spot is money supply growth, but even here the recent acceleration reflects a rebound from low levels rather than a structural concern. Overall, the Bank of Japan (BoJ) expects real GDP growth of around 1% annually over the next three years—well above its estimated potential rate of 0.5%.

Figure 1: Japan business cycle indicator assessment

Source: Westbourne Research. Note: Green = positive, blue = neutral, and maroon = negative. The direction the arrows point denote momentum – rising, falling and stable.

Corporate Strength and Investment Momentum

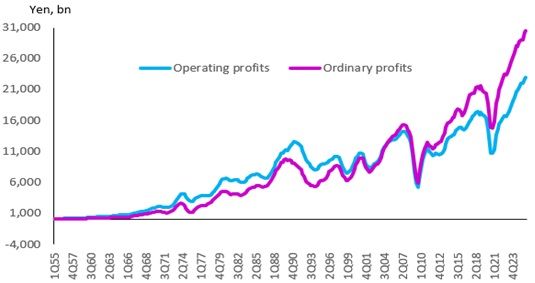

Corporate Japan is in robust health. Profitability across sectors and firm sizes has risen sharply, supported by strong demand and improved pricing power. Operating and ordinary profits are at record highs, with broad-based gains across manufacturing and non-manufacturing industries (Figure 2). Compared to the pandemic trough in late 2020, operating profits have more than doubled, reflecting both cyclical recovery and structural improvement.

Figure 2: Corporate operating and ordinary profits

Source: Japan Ministry of Finance & Westbourne Research

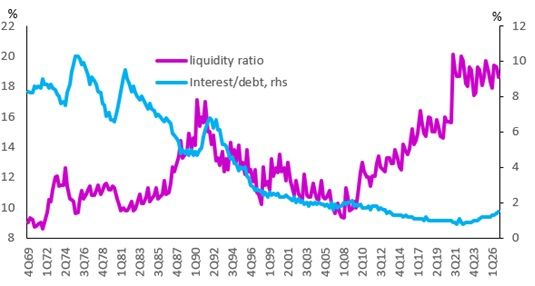

Importantly, corporate balance sheets remain exceptionally strong (Figure 3). Liquidity levels—measured by liquid assets relative to short-term liabilities—are near multi-decade highs, providing a significant buffer against external shocks. While debt-servicing costs are rising, they are doing so from historically low levels, highlighting how underleveraged Japanese firms remain.

Figure 3: Corporate liquidity and interest to debt ratios

Source: Japan Ministry of Finance & Westbourne Research

This is a crucial distinction: unlike other economies that experienced credit-fuelled excesses, Japan’s prolonged period of accommodative monetary policy did not lead to widespread overborrowing. Even at its most accommodative point, real borrowing costs never reached the deeply negative levels seen elsewhere. As a result, corporate balance sheets are well positioned to absorb higher interest rates as policy normalisation continues. With the policy rate still below estimates of the neutral rate, borrowing costs are unlikely to become a binding constraint in the near term.

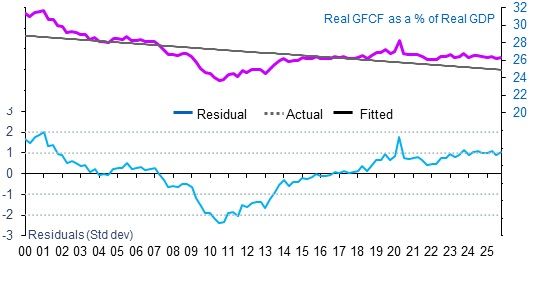

This financial strength is translating into sustained investment. Private domestic fixed investment has been growing steadily, supported by rising profits and improving demand conditions. While some moderation may occur in the near term, the broader investment upcycle remains intact (Figure 4).

Figure 4: Japan investment cycle

Source: Haver Analytics & Westbourne Research

Two structural drivers underpin this outlook. First, the rapid adoption of artificial intelligence and digital technologies is accelerating investment in software and IT infrastructure. Second, demographic pressures—specifically a shrinking and ageing workforce—are forcing firms to substitute capital for labour. These forces are reinforcing each other, creating a durable foundation for continued capital expenditure.

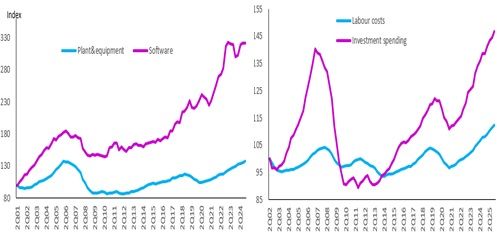

Rising labour costs further support this trend (Figure 5). Personnel expenses have increased significantly in recent years as policymakers push for wage growth to achieve sustained inflation. In response, firms are investing heavily in automation and productivity-enhancing technologies to preserve margins. This shift is evident across sectors, from manufacturing to services, and reflects a broader transformation in Japan’s economic structure.

Figure 5: Corporate capex and labour costs

Source: Japan Ministry of Finance & Westbourne Research

A Changing Economic Landscape

Japan today is markedly different from the economy of the past. Digital adoption has accelerated, payment systems have modernised, and businesses are increasingly integrated into global technological trends. These changes, while gradual, are meaningful and reinforce the case for sustained productivity gains.

The combination of strong corporate fundamentals, structural reform, and technological adoption suggests that Japan is not merely experiencing a cyclical recovery but undergoing a deeper transformation.

Households and Consumption: A Gradual Strengthening

Turning to households, the outlook for consumption has improved. While growth is unlikely to match that of emerging markets, spending should expand steadily as the business cycle broadens.

A more accurate measure of consumption than retail sales is the BoJ’s consumption activity index, which closely tracks national accounts data. This index indicates that household spending is stabilising and gradually improving (Figure 6).

Figure 6: Bank of Japan consumption activity index

Source: Haver Analytics & Westbourne Research

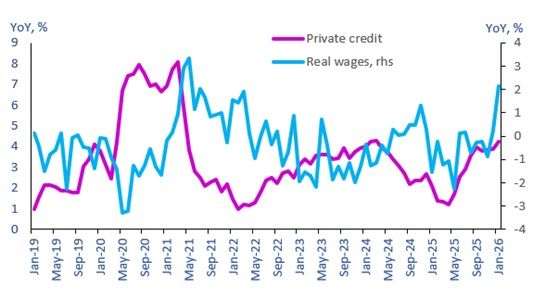

Leading indicators support this trend (Figure 7). Real wage growth has turned positive after a brief decline, supported by easing inflation and rising nominal wages. The labour market remains tight, with policymakers expecting steady wage increases in the coming years. There is also potential for stronger-than-expected gains if labour shortages intensify further.

Equally important is the recovery in private credit demand. As households become more confident, borrowing is beginning to rise, signalling a shift toward the expansion phase of the business cycle. This dynamic—where spending grows faster than income—is typical of an upswing and reflects improving risk appetite.

Figure 7: Private credit and real wages

Source: Haver Analytics & Westbourne Research

Tailwinds and Headwinds

Several factors will shape the trajectory of consumption. On the positive side, higher interest rates are improving returns on savings—an important consideration in a country with a large retired population. Fiscal policy also provides support, with stimulus measures expected to disproportionately benefit households.

There are also discussions around reducing the consumption tax, although implementation is likely to be delayed due to legislative constraints. If enacted, such measures would provide an additional boost to spending.

However, there are headwinds to consider. Rising mortgage costs and higher energy prices could weigh on disposable income and discretionary spending. Conventional economic theory suggests that ageing societies are more vulnerable to such pressures, as fixed incomes limit the ability to absorb rising costs.

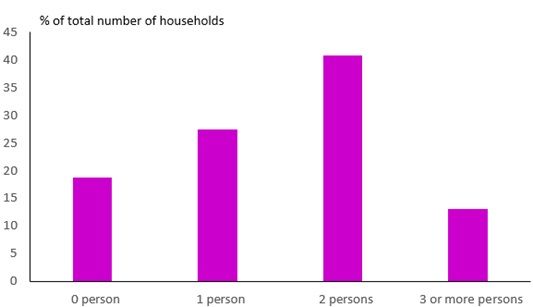

Yet Japan challenges this assumption. Labour force participation among older individuals remains remarkably high (Figure 8). A significant majority of households aged 60 and above still have at least one income earner, reflecting longer working lives and a more flexible labour market; nearly 70% of households aged 60 and above have at least one wage earner. For those aged 60–69, the figure rises to 88%, while it is 60% for the 70–79 age group and 42% for those aged 80 and above. This mitigates the negative effects typically associated with ageing populations.

Figure 8: Employment by household

Source: Japan e-stat & Westbourne Research

Moreover, while incomes tend to decline with age, this is partially offset by accumulated wealth and lower expenditure. Many older households have paid off mortgages and face reduced spending on education, transportation, and other variable costs. These factors help sustain consumption even as demographics shift.

Housing illustrates this dynamic clearly. A large majority of Japanese households own their homes outright, with only a minority still servicing mortgages. This contrasts with other advanced economies, where debt burdens remain higher and more persistent.

Conclusion

Japan’s economic outlook is underpinned by a combination of cyclical strength and structural change. Corporate profitability is robust, balance sheets are healthy, and investment is supported by both technological innovation and demographic necessity. At the same time, household consumption is gradually strengthening, aided by rising wages and resilient labour force participation.

While risks remain—particularly from higher energy prices and rising interest rates—the overall picture is one of resilience. The current market correction should therefore be seen not as a warning sign, but as an opportunity.

Sharmila Whelan

AuthorMore in Author Profile »The founder of Westbourne Research (www.westbourne-research.com), Sharmila Whelan is a seasoned Global Geopolitical-Macro Strategist with nearly three decades of experience advising buy-side clients on multi-asset investment strategies and asset allocations. Her career has been defined by her differentiated thinking, a deep understanding of the intricate connections between global geopolitics, macro and policy dynamics, and the Austrian business cycle approach to economic analysis. She has counseled governmental bodies such as the CIA, the US State Department, the British High Commission, DFID, and China’s NDRC.

Sharmila has held prominent roles in both London and Hong Kong, serving as Managing Director at Aletheia Capital, Director at Merrill Lynch Bank of America, Senior Economist at CLSA, and Asia Regional Economist at BP Plc. In 2022, Bloomberg recognised her as one of the UK's "12 New Expert Voices." She is a frequent media commentator on Bloomberg TV and radio, BBC World Business News, and CNBC, and is a sought-after speaker at high-profile events such as the Financial Times Wealth Summit and CFA UK & India conferences. Sharmila also contributes opinion pieces to Financial Times Professional Wealth Management and the Economist Group’s EIU.