ISM Index: The Manufacturing Sector Continues to Struggle

Summary

- The production and employment components registered gains.

- But new orders disappointed.

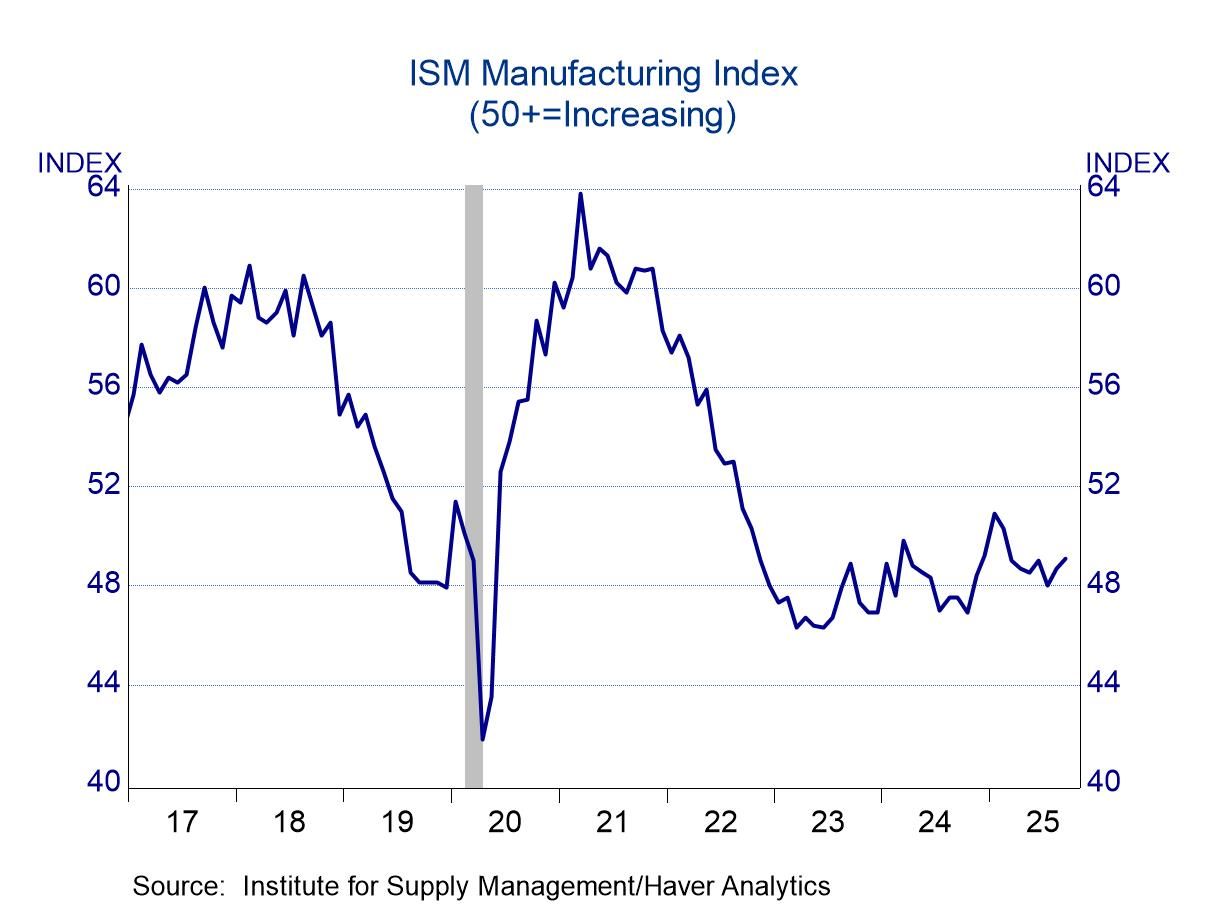

The index of manufacturing activity published by the Institute for Supply Management rose 0.4 percentage point in September to 49.1%. With 50% representing the dividing line between expansion and contraction, the latest reading signaled slow activity in the factory sector, continuing a pattern that has been in place since late 2022. September marked the seventh consecutive month with a sub-50% reading and the 33rd soft result in the past 35 months.

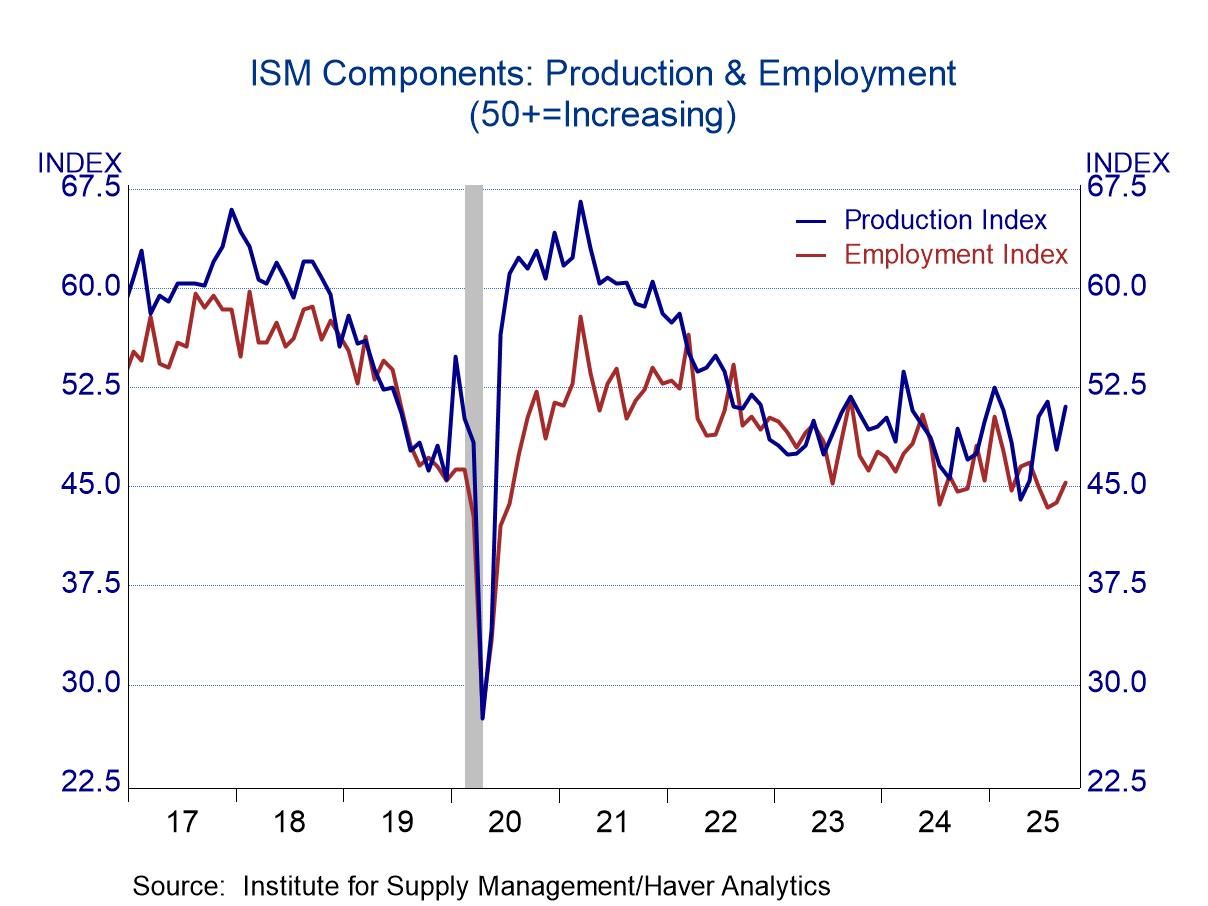

The production and employment components accounted for most of the advance in the headline index, with the production index increasing 3.2 percentage points to 51.0% and the employment gauge rising 1.5 percentage points to 45.3%. These increases, however, do not seem to signal revival in manufacturing activity. The production index has been bouncing on either side of 50% for almost three years, leaving a decidedly flat trend. The increase in the employment index was not firm enough to interrupt the downward drift that has unfolded over the past three years.

The improvements in production and employment were partially offset by a drop of 2.5 percentage points in the new orders component to 48.9%. The latest reading followed two consecutive increases which pushed the August tally to 51.4%. The drop in September, though, suggested that the advances in the prior two months represented normal volatility rather than the beginning of an upward trend.

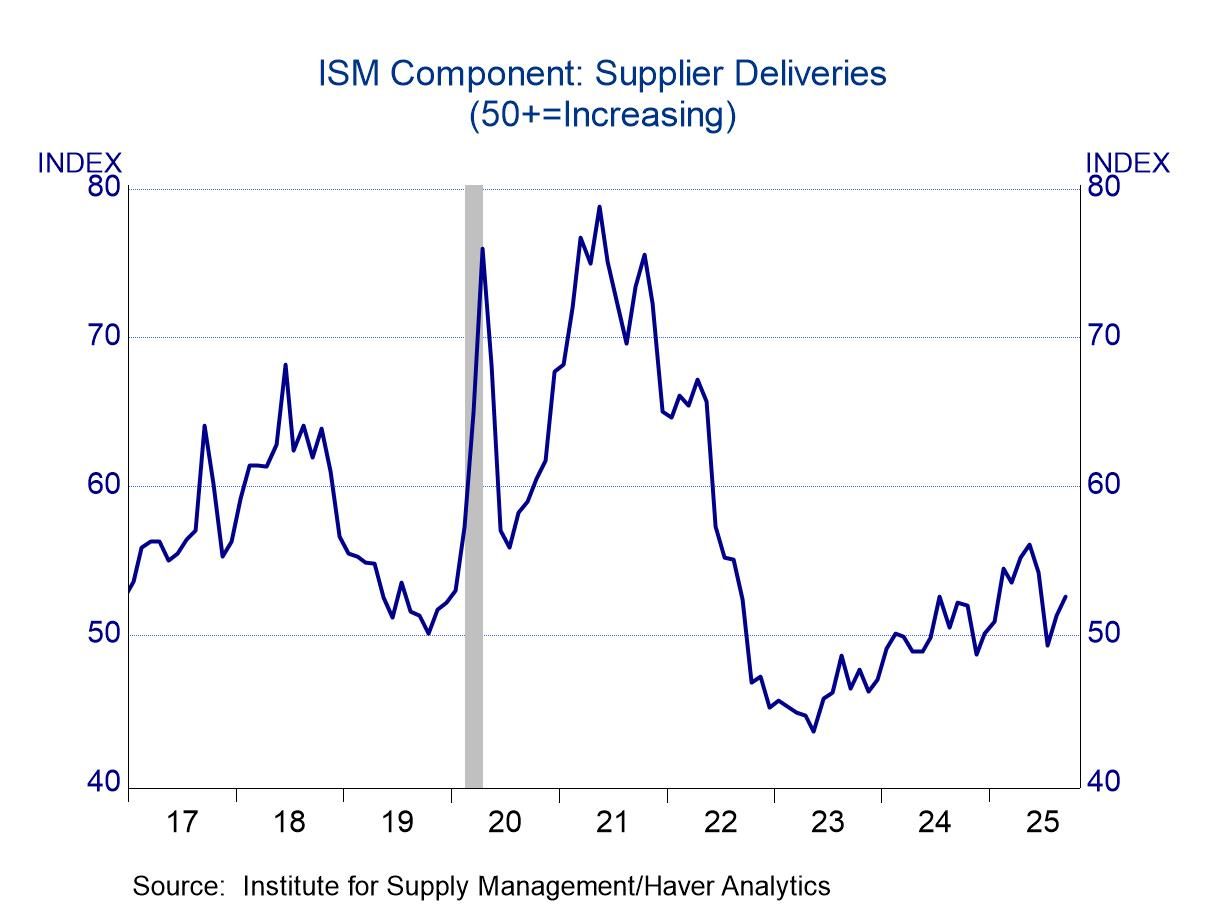

While the trends in the headline index and most components are sideways or downward, the supplier delivery index has moved higher in the past few years and has been above 50% in eight of the nine months this year. However, there was one notably soft month this year (a drop of 4.9 percentage points in July to 49.3%), and thus the latest level is not especially impressive.

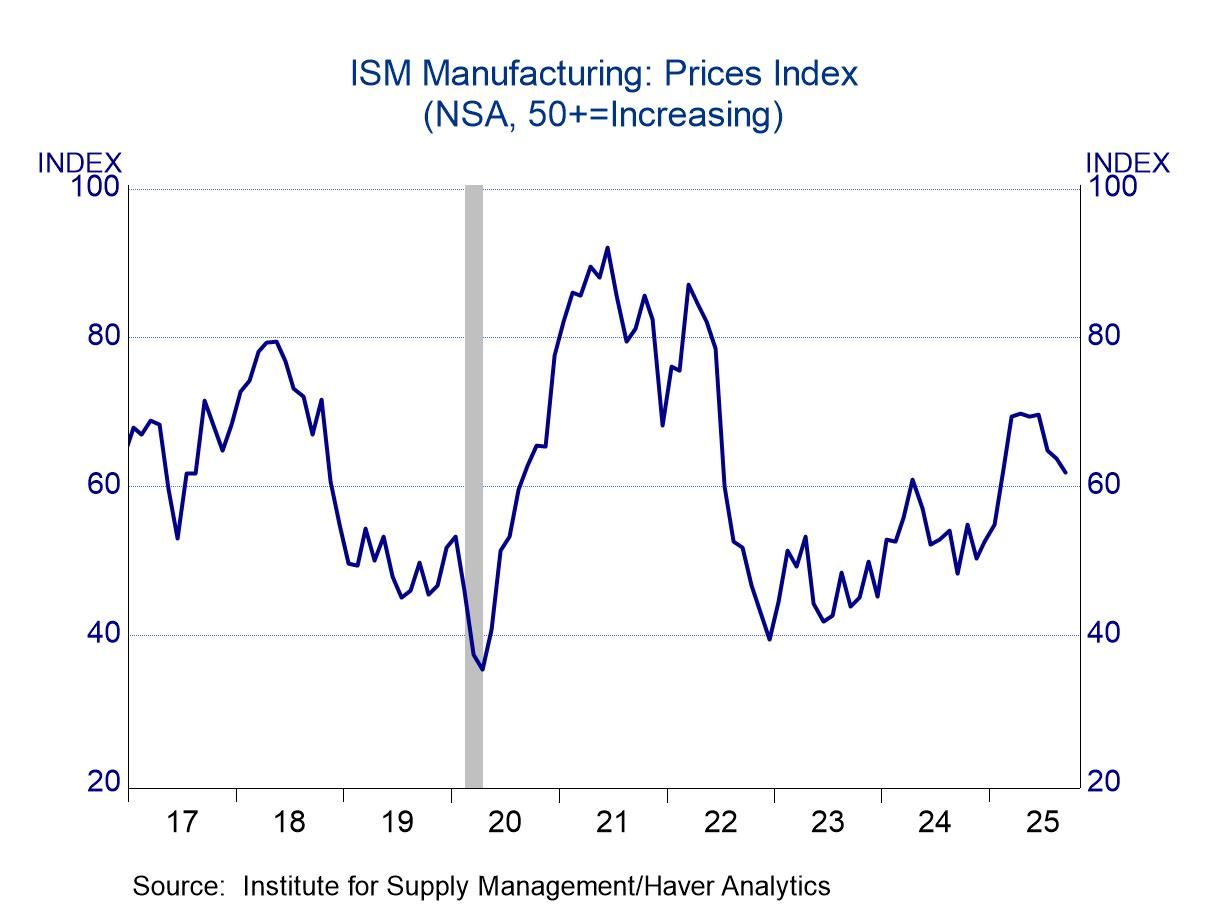

The prices index, which is not seasonally adjusted and is not a component of the headline measure, fell 1.8 percentage points in September, marking the fourth decline in the past five months and moving to 61.9%, 7.9 percentage points below the recent high of 69.8% in April. The measure remains well above the critical 50% threshold, but it also is well shy of readings above 80% in 2021 and 2022, when inflation had climbed to a troublesome rate.

The ISM index is signaling soft activity in the manufacturing sector, and this view is confirmed by the industrial production index published by the Federal Reserve. This measure has shown little net growth in the past few years, declining slightly during 2023 and 2024 and inching only a tad higher so far this year. The level of production in August (latest available) was still 0.3% shy of the cyclical high in October 2022.

The ISM figures are based on responses from over 400 purchasing and supply executives from 18 industries, which are weighted according to each industry’s contribution to GDP. These data are diffusion indexes where a reading above 50 indicates expansion; below 50 indicates contraction. The ISM Manufacturing PMI is a composite index based on the diffusion indexes of five of the indexes (seasonally adjusted) with equal weights: New Orders, Production, Employment, Supplier Deliveries, and Inventories. The figures from the Institute for Supply Management can be found in Haver’s USECON database; further detail is found in the SURVEYS database. The expectations number is available in Haver’s AS1REPNA database.

Michael J. Moran

AuthorMore in Author Profile »Before joining Haver Analytics in 2025, Michael J. Moran was the chief economist of Daiwa Capital Markets America Inc. He was responsible for preparing the firm’s economic forecast and interest rate outlook. He traveled frequently to visit the clients of Daiwa Capital Markets and wrote weekly economic commentary. Mr. Moran also was involved in the flux of financial markets, as he spent a portion of each day on Daiwa’s trading floor interpreting economic statistics and Federal Reserve activity for traders and salespeople. Mr. Moran is quoted frequently in the financial press, and he appears regularly on cable news shows. He also has published articles in several journals and periodicals. Before joining Daiwa Capital Markets America, Mr. Moran worked as an economist at the Federal Reserve Board in Washington, D.C. where he analyzed a broad range of issues dealing with the financial sector of the economy and regularly briefed the Board of Governors. He was on the faculty of Pennsylvania State University from 1979 to 1980 and taught on a part-time basis at George Washington University from 1980 to 1987.

Mr. Moran received his Ph.D. in economics from Pennsylvania State University in 1980 and a B.S. in business administration from the University of Bridgeport in 1975. He was a CFA charter holder from 2002 until 2016.

More Economy in Brief

Asia

Asia