Global| Mar 03 2026

Global| Mar 03 2026Inflation in Europe Picks Up – Ahead of Hostilities

Inflation in the European Monetary Union picked up in February, ahead of the beginning of new hostilities in the Middle East. The increase in the harmonized index of consumer prices moved up to 0.3% in February from 0.1% to January. Progression on the annual rate of price increase moved up to 1.9% over 12 months, to a 2.1% annual rate over six months, and to a 2.4% annual rate over three months.

This is a modest acceleration and not something to get particularly excited about, except that with new hostilities in the Middle East, oil prices have begun to rise significantly, and there will be apprehension about how much more there is to come. However, the initial oil price reaction was muted, and the follow-up price reaction has also been relatively muted so these will translate into a nontrivial impact on inflation and in the harmonized index for consumer prices in the monetary union, as well as in the key prices watched by central banks globally.

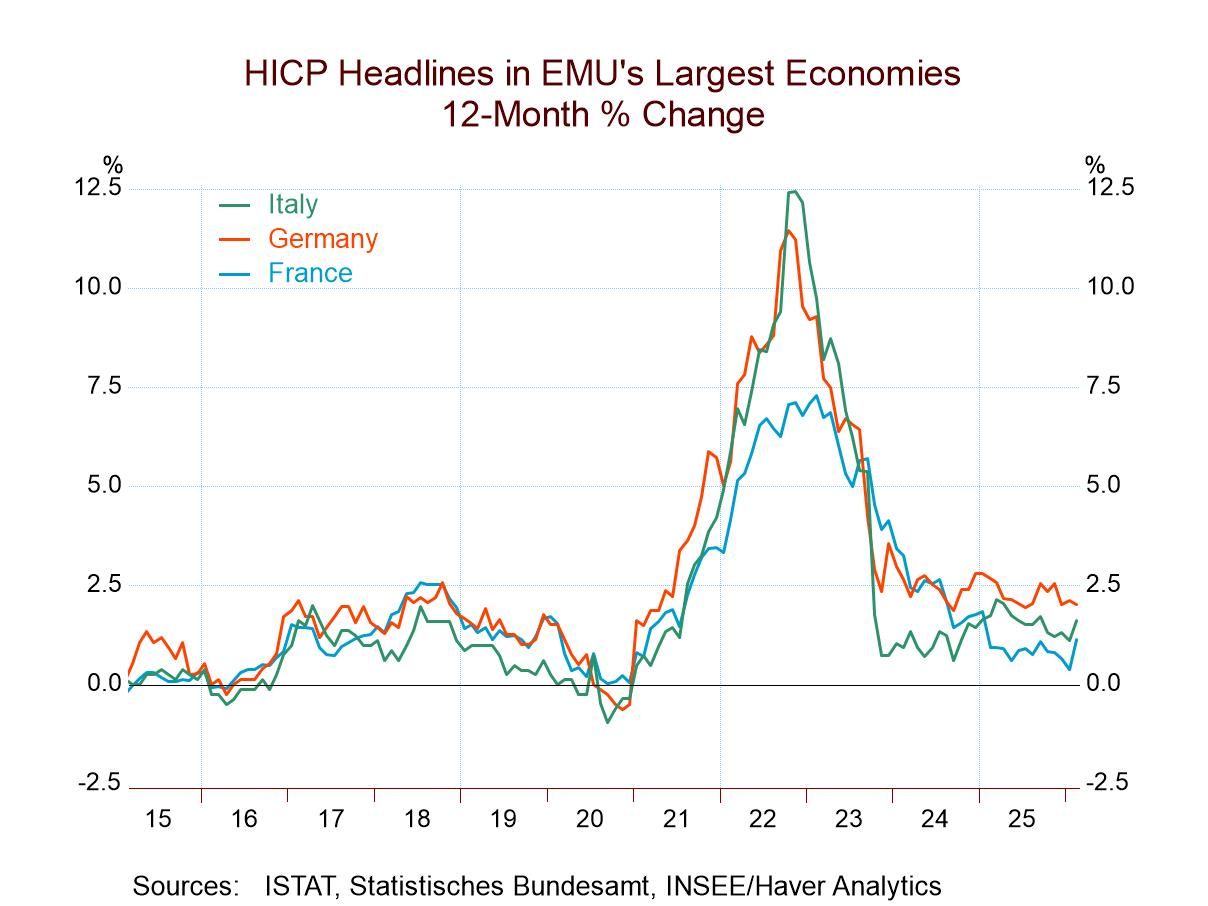

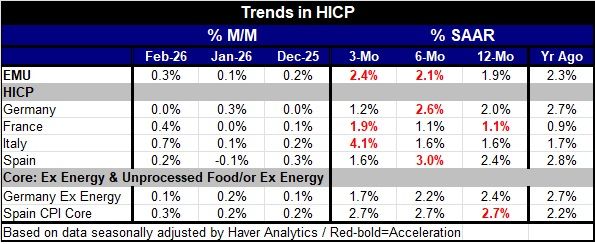

Big Four Economies The Big Four economies in the monetary union produced scattered results in February. Germany produced no increase in its February HICP. The HICP for France jumped by 0.4% month-to-month. Spain showed an increase of 0.2%; Italy reported an outsized increase of 0.7% in February. Still, the January and February data for this group of countries show prices mostly very well behaved. If we simply multiply these 12 increases (four countries over three months) together we get prices rising at a 2.2% annual rate across all the countries over the three months. That is close to target.

Annual and Sequential Big Four Inflation Inflation for the Big Four economies ranges from a top pace of 2.4% in Spain to the lowest pace of 1.1% in France with Italy's 1.6% and Germany's on-target 2% making up middle cases. Even the biggest price increase from Spain at 2.4% is not particularly frightening. Inside of 12 months looking at the six- and 3-month trends, Germany's trends move up to 2.6% over six months and then down to 1.2%. France's 6-month inflation remains at 1.1% over six months but then moves up to a 1.9% annual rate over three months. Italy's 12-month pace of 1.6% holds in place over six months, but then the 3-month inflation rate jumps to a 4.1% annual rate. For Spain, the 2.4% 12 month rate rises to a 3% annual rate over six months and then falls sharply to a 1.6% annual rate over three months.

Headline vs. Core Inflation Headline inflation rates, of course, are mercurial because of the impact of oil prices on them. Two early reporters gave us core inflation or ex-energy inflation rates. In the case of Spain, core inflation is stuck at 2.7% on all horizons. Germany's index excluding energy is at 2.4% over 12 months, but then Germany’s six-month pace falls to 2.2%, and its three-month pace falls again to 1.7%. In the case of Germany, 12-month ex-energy inflation is mildly acceptable, but progressing to the three-month horizon, the inflation rate drops back well into place. For Spain, the 2.7% 12-month inflation rate persists across all horizons and is unacceptably high.

Longer Trends Inflation is generally behaving and riding downtrends in the monetary union, with 12- month inflation generally lower than 12-month inflation was a year ago. That is true for all the major metrics in the table except two. The first exception is France when the 12-month inflation rate is 1.1% compared to 0.9% over 12 months a year ago (still, obviously very well behaved). In the case of Spain, core inflation moves up to 2.7% over 12 months after being at 2.2% just a year ago.

Events The inflation data this month show results we would more or less take in stride if it weren't for conflicts in the Middle East that are having a fresh upward effect on energy prices. We expect that to be reflected in next month’s inflation reports. Next month’s anticipated bad reaction will stack on top of this month when results came in worse than expected. For the most part, headline inflation is very close to its mark; however, core inflation shows signs of being stubborn and stuck at levels that are either slightly or more decidedly too high. This, of course, is a phenomenon we see in the United States with inflation stuck close to the 3% level, a percentage point above the Fed’s target. Europe’s situation is not unique.

Oil and War: A Nasty Combination Since we're mostly talking about oil, it's highly likely that the European Central Bank is not going to be very concerned about these numbers because they're coming out of a state of warfare, and because, generally speaking, the inflation numbers are relatively close to target. Moreover, GDP growth rates right now are not particularly impressive. Unemployment rates are low across the euro area despite weak growth; there's no problem with the employment side of the equation. Monetary policy in an environment like this is going to be the product of the discretion of central bankers who are going to show us what they're worried about most and whether they're worried about disturbing the already weak rate of growth in their economy. Or are they going to be more committed to getting inflation down to target, a target they've been at least mildly missing for some time? Having war as the active ingredient in the inflation mix may be the deciding factor to keep the central bank on the sidelines. However, central bankers also know that ignoring an upturn in inflation whether it's caused by commodity prices, oil or something else is not a recipe for good monetary policy. For that reason, markets should be on alert in the coming months.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief