Home Prices, OER and Rental Costs: Positive News for Inflation in 2026-2027

|in:Viewpoints

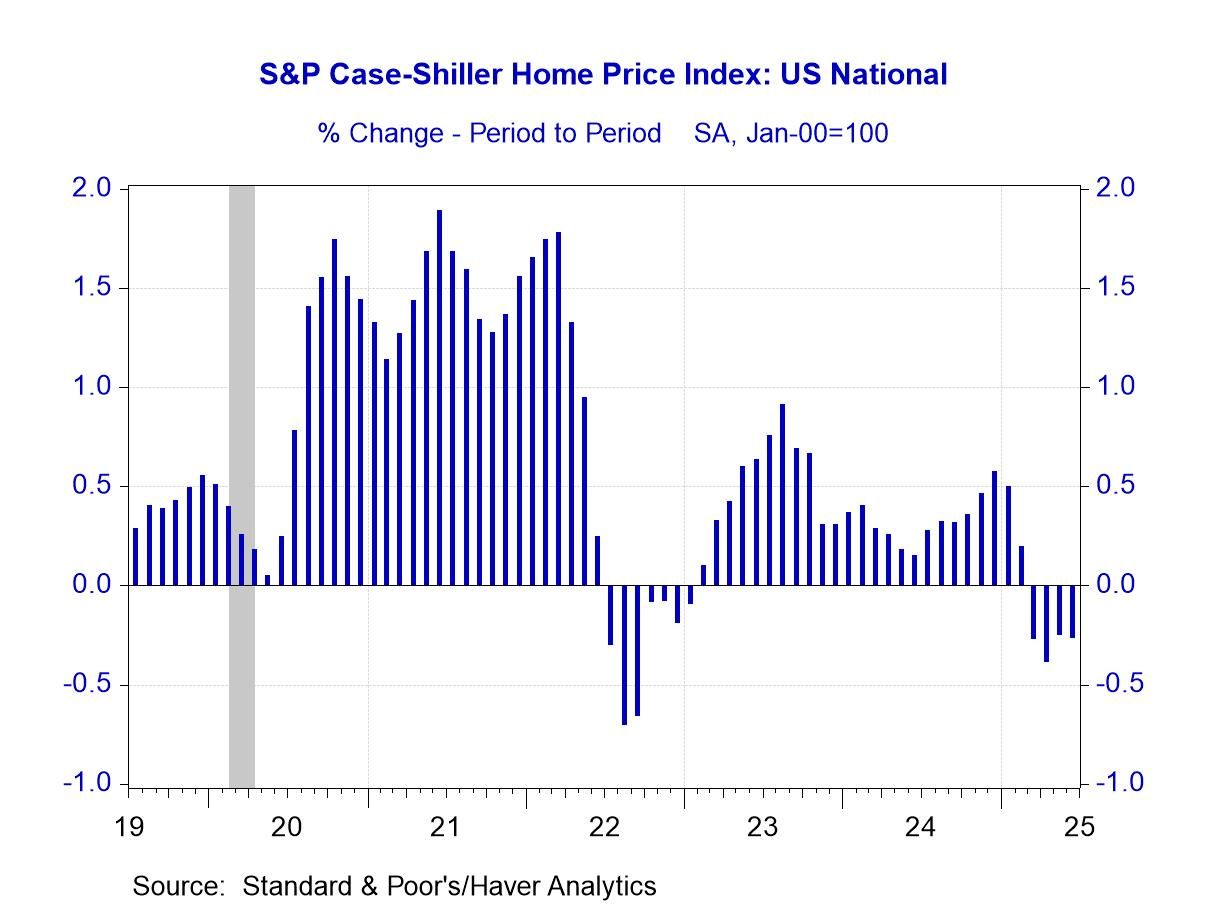

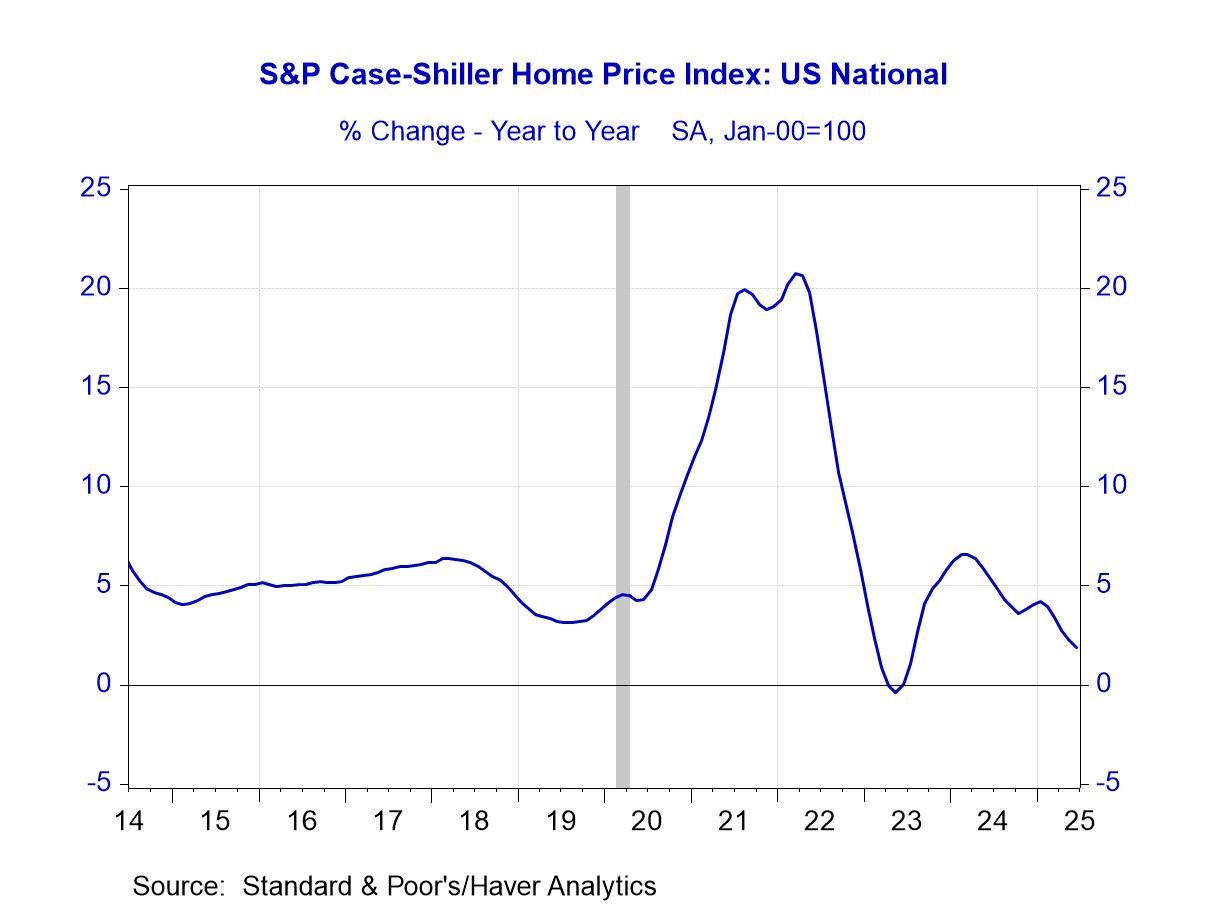

The Case Shiller Home Price Index fell 0.3% in June, its 4th consecutive monthly decline, lowering its yr/yr increase to 1.9% from 6.6% in February 2024 (Charts 1 and 2).

The flattening of home prices reflects slower demand for home sales and a moderation of transactions. This has resulted from the surge in home prices--the Case Shiller Home Price Index surged 38.9% from mid-2020-mid-2022 and until recently it has continued to rise--combined with higher mortgage rates. The home affordability index hovers near an all-time high. The current fundamentals in housing suggest that the Case Shiller Home Price Index will continue to be flat-to-down in the next year.

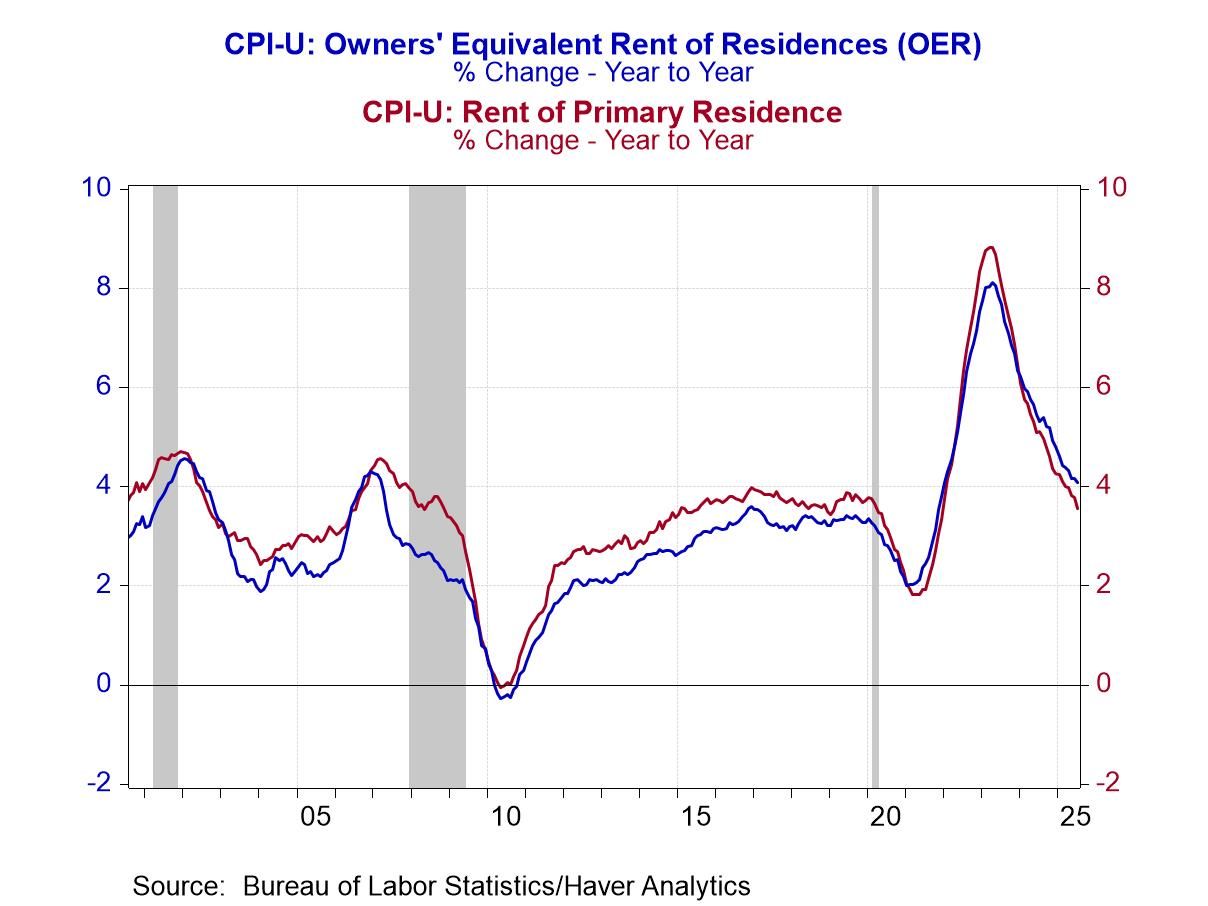

The recent consecutive monthly declines in home prices have potentially important implications for overall inflation. Rental costs and OER (Owners’ equivalent rent of residences) are the largest combined components of the CPI and PCE Price Index. OER and rental costs comprise 33.6% of the CPI (OER, 26.2%; rental costs, 7.4%) and somewhat less in the PCE price index. PCE inflation (the PCE inflation reflects the prices of all goods and services consumed, while the CPI excludes consumption that is financed by third party payers, including Medicare, Medicaid and employer-financed health insurance), which results in a higher weight for health care costs and a lower weight for the shelter components.

Through July, rental costs were up 3.5% yr/yr, down from 5.1% a year earlier and OER is up 4.0% yr/yr, down from 5.3% yr/yr. (Chart 3). Both OER and rental costs are derived by the Bureau of Labor Statistics from the trend in home values. A historical note: prior to May 1983, the CPI included direct measures of mortgage rates. This measurement presumed that homeowners bought their homes at current mortgage rates each month. Beginning win May 1983, the BLS shifted its measure of inflation and replaced the mortgage rate with measures of OER and rental costs. Since then, there have been modest modifications.

Model-based predictions of rental costs and OER. By summer 2021, the Fed had lowered rates to zero and engaged in massive purchases of Treasuries and MBS, and the government had increased deficit spending by a whopping 25% of GDP. Inflation had just begun to accelerate, and Case Shiller Home Price index was soaring. Along with my former colleague Mahmoud AbuGhzalah, I estimated a model that predicted changes of OER and rental costs based on the Case Shiller Hole Price Index. The model proved prescient, as described below. Based on that model, I now predict the OER + rental costs will continue to moderate sharply in the next year to yr/yr increases close to one-half their current pace. And if the Case Shiller Home Price Index continues to be flat-to-down a touch—which seems likely based on their current lofty prices and soft housing demand, the monthly changes in rental costs and OER will subtract from inflation, and their yr/yr increases will head toward zero in 2027.

Our model was a VAR (vector auto regression) with three variables, the Case Shiller Home Price Index, rental costs and OER in which all variables are regressed on their lagged values. This allows the model to estimate the impacts of a shock to one of the variables. Most importantly, it estimates the lagged impacts of a change in the Case Shiller Home Price Index on OER and rental costs. We estimated the model using monthly data going back to 1983 when the BLS changed its method of calculating the CPI to include OER and rental costs.

The model provided a robust statistic fit, with percentage changes in OER and rental costs optimally following the Case Shiller Home Price Index by 12 months and more. In Summer 2021, the model predicted that OER and rental costs, which at the time were rising 3.25%-3.5% yr/yr, would soar and contribute to very high inflation. That’s exactly what happened. This increase in housing inflation somehow came as a surprise to the Fed. When inflation and the shelter component soared in the second half of 2021 and 2022, the Fed began measuring inflation excluding this important sector. When OER and rental cost increases reached 7.5% while the increases in Case Shiller had begun to ebb, we re-estimated the model and it predicted OER and rental costs would recede. They did.

The four recent consecutive monthly declines in Case Shiller (April-July 2025, when its monthly change averaged -0.3%) and its rapidly declining yr/yr increases now predict a continued deceleration in OER and rental costs. Based on the moderating increases of the Case Shiller Home Price Index to date, the monthly and yr/yr increases in OER and rental costs should continue to decelerate significantly further, and subtract from inflation. I expect the Case Shiller index to remain negative to flat for many months to come, and for its yr/yr to eventually decline toward zero. This will contribute to lower inflation, more so in the CPI than the PCE, and will likely be reflected in lower inflationary expectations. As that unfolds, the Fed can be expected to drop its measure of inflation that excludes the housing component.

Chart 1. Case Shiller Home Price Index, mo/mo %chg

Chart 2. Case Shiller Home Price Index, yr/yr %chg

Chart 3. OER and Rental Costs %chg yr/yr

Mickey D. Levy

AuthorMore in Author Profile »Mickey Levy is a macroeconomist who uniquely analyzes economic and financial market performance and how they are affected by monetary and fiscal policies. Dr. Levy started his career conducting research at the Congressional Budget Office and American Enterprise Institute, and for many years was Chief Economist at Bank of America, followed by Berenberg Capital Markets. He is a Visiting Fellow at the Hoover Institution at Stanford University and a long-standing member of the Shadow Open Market Committee.

Dr. Levy is a leading expert on the Federal Reserve’s monetary policy, with a deep understanding of fiscal policy and how they interact. He has researched and spoken extensively on financial market behavior, and has a strong track record in forecasting. Dr. Levy’s early research was on the Fed’s debt monetization and different aspects of the government’s public finances. He has written hundreds of articles and papers for leading economic journals on U.S. and global economic conditions. He has testified frequently before the U.S. Congress on monetary and fiscal policies, banking and credit conditions, regulations, and global trade, and is a frequent contributor to the Wall Street Journal.

He is a member of the Council on Foreign Relations and the Economic Club of New York, and previously served on the Panel of Economic Advisors to the Federal Reserve of New York, as well as the Advisory Panel of the Office of Financial Research.

Dr. Levy holds a Ph.D. in Economics from University of Maryland, a Master’s in Public Policy from U.C. Berkeley, and a B.A. in Economics from U.C. Santa Barbara.