History Rhymes – The Siren Song of Core Inflation

|in:Viewpoints

The concept of “core” inflation, that is, a measure of inflation excluding food and energy prices, came into fashion in 1973. In 1972, there was an El Nino weather phenomenon, which decimated the sardine school off the coast of Peru. Sardines were ground into fishmeal, which, in turn, was used as animal feed. The dearth of sardines resulted in an increase in the price of land-animal protein in 1973. Energy prices soared in late 1973 as a result of the OPEC oil embargo in the aftermath of the Yom Kippur War between Israel and its neighbors. (It has been argued that the catalyst for the OPEC oil embargo was the decline in the foreign-exchange value of the US dollar. OPEC nations were being paid in US dollars, which reduced their purchasing power for goods and services sold in other currencies). The chairman of the Federal Reserve at that time was the venerable Arthur Burns – he who must be obeyed. Burns argued that the increases in food and energy prices being experienced in 1973 were not the result of the current stance of monetary policy, but were caused by exogenous factors. Therefore, according to Burns, monetary policy decisions should be based on some concept of the underlying rate of inflation, not price increases resulting from exogenous factors.

Let’s fast forward to today. Energy prices have shot up in the past week or so coinciding with the US and Israel shooting up Iran. Less reported, El Nino is once again plaguing Peru. I have not read that El Nino has adversely affected the sardines, but it is producing severe flooding in Peru, which is playing havoc with Peruvian agriculture. I bet you didn’t know that Peru is a major world exporter of blueberries, grapes, avocados, coffee and asparagus. Neither did I until I started writing this commentary. We do not know how long this military “excursion” into Iran will last and, therefore, how long the resulting increase in energy prices will last and/or how high they will go. But I suspect that we will hear Fed policymakers and financial media talking heads say that Fed policy should be guided by the current and expected behavior of core inflation. That is, the inflation rate excluding the prices of food and energy items because the current increases in food and energy items have not been caused by monetary policy and might be transitory. I’ll bet that at least one Fed policymaker whose term has been extended (and whose initials are SM) will argue that monetary policy should be eased because of the negative effects these food and energy price increases will have on real economic growth.

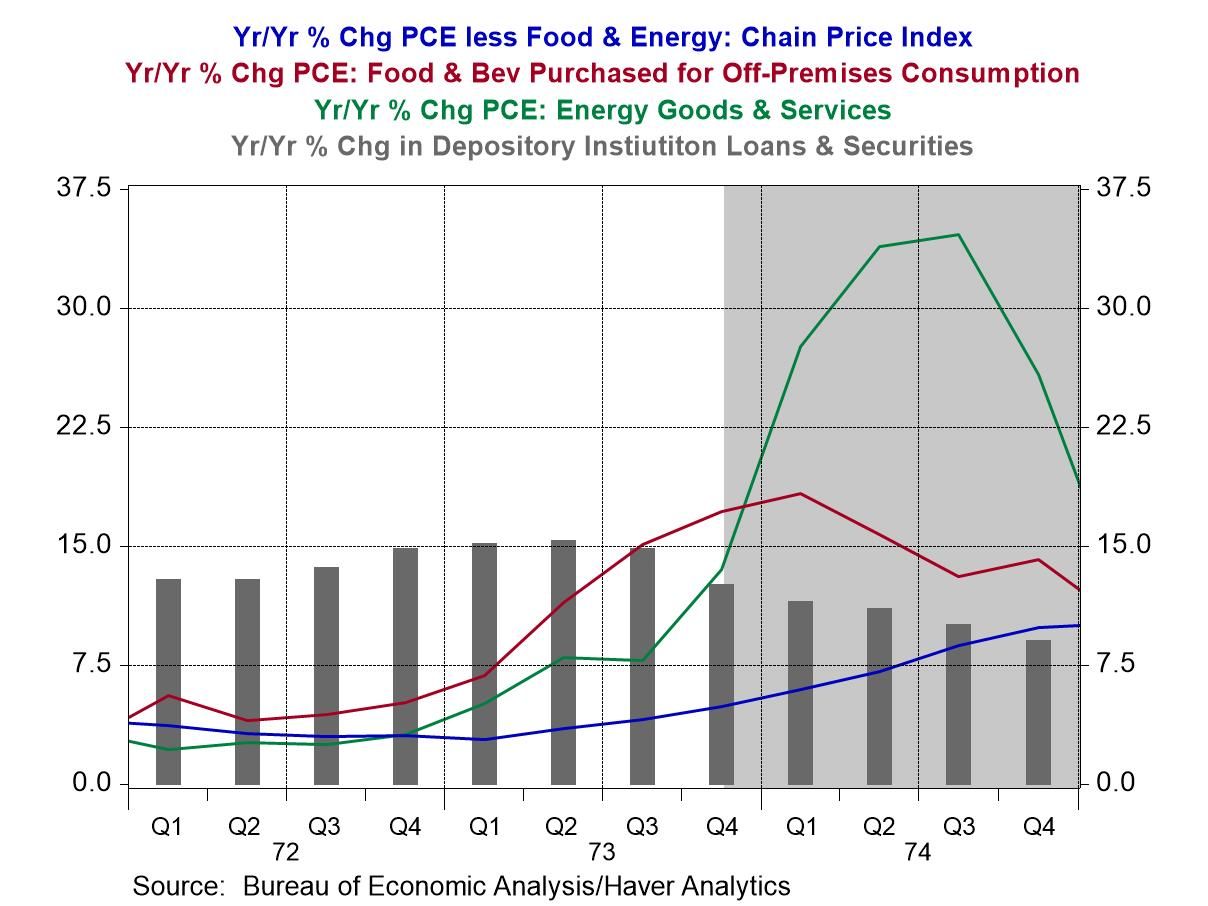

Let’s look at what happened to core inflation in the early 1970s when food and energy prices flared higher (see Chart 1). In 1972:Q4, year-over-year core Personal Consumption Expenditures (PCE) inflation was 3.05%, food inflation 5.14% and energy inflation was 3.10%. By 1974:Q4, year-over-year core PCE inflation was 9.84%, food inflation was 14.10% and energy inflation was 25.80%. So, during this period, not only did food and energy price inflation soar, so, too, did core inflation.

Chart 1

If the prices of food and energy increase and nominal personal income remains constant, then a household will have less nominal income to spend on “core” goods and services after having to allocate a greater portion of its nominal income on food and energy items. All else the same, this would put downward pressure on the prices of core goods and services. But if nominal personal income is allowed to increase along with the increases in the prices of food and energy goods and services, then the household can maintain its purchases of core goods and services, which will not result in downward pressure on the prices of core goods and services. If nominal income increases enough, there can be upward pressure on the prices of core goods and services.

Notice the gray bars in Chart 1. They represent the year-over-year percent changes in the sum of loans and securities held by depository institutions. This is a narrower version of my (and Austrian economists) thin-air credit. The median growth in this version of thin-air credit from 1972:Q1 through 1974:Q4 was 12.87%. Just for reference, the median growth rate of this version of thin-air credit from 1955 through 2025 is 6.9%. So, in the early 1970s, there was relatively rapid growth in this version of thin-air credit.

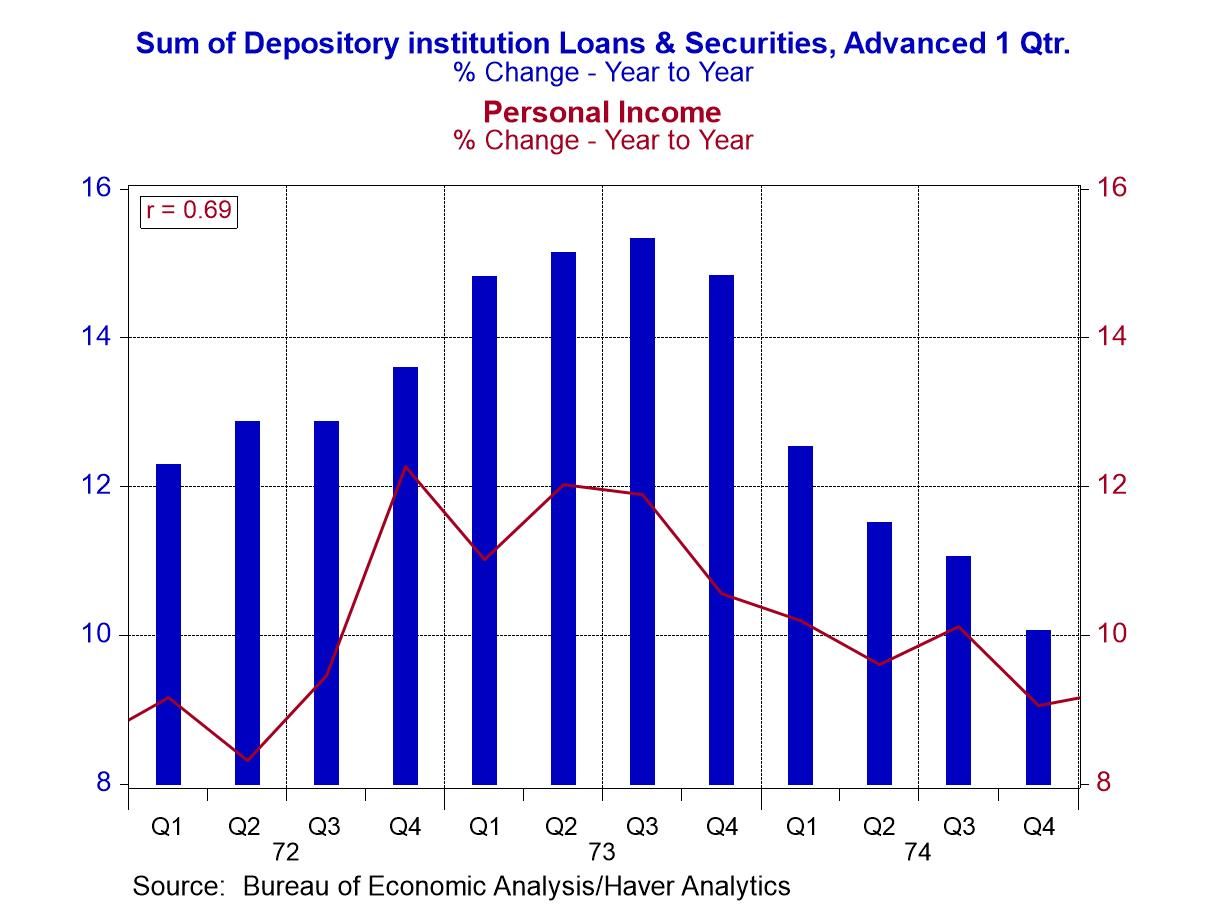

But I digress. I was discussing the effect on core inflation from increasing food and energy inflation depending on the behavior of nominal personal income growth. I posited that an increase in nominal income growth could result in an increase in core inflation. Chart 2 shows that there was a relatively high correlation, 0.69, between growth in the sum of depository institution loans and investments, advanced one quarter, and nominal personal income growth.

Chart 2

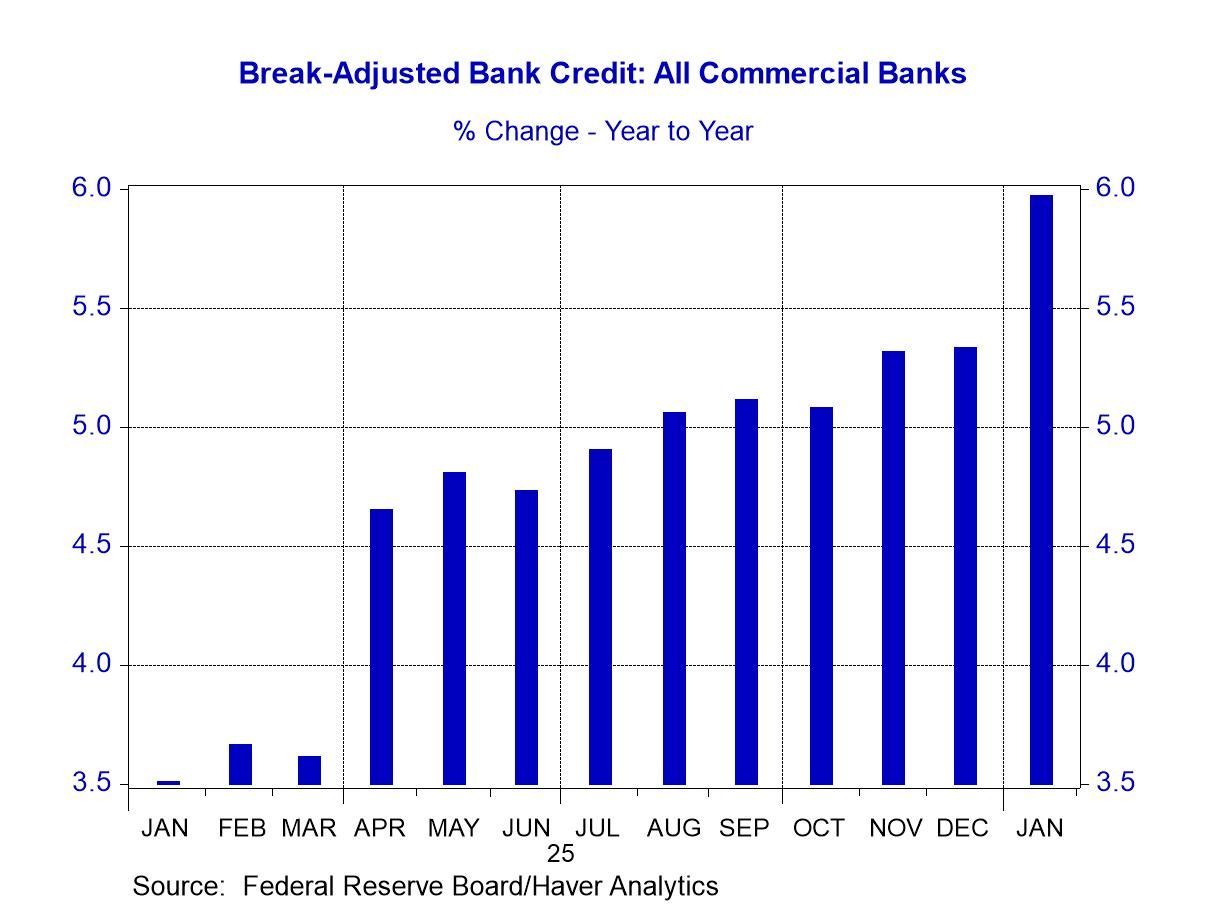

So, in order to prevent exogenous increases in the prices of certain goods and services from increasing the “core” price index, the Fed should try to prevent the rate of growth in thin-air credit from increasing. Chart 3 shows that the rate of growth of an even narrower version of thin-air credit, bank credit, has gradually been increasing over the 12 months ended January 2026. Year-over-year growth in bank credit in January 2026 was 5.97%, not too rapid or too slow. At a given level of the federal funds rate, I would expect that if the energy inflation we have experienced in the past week or so were to persist, this would put upward pressure on the demand for nominal bank credit. If the Fed were to allow bank credit growth to increase in the face of higher energy inflation, it would run the risk of promoting an increase in the core rate of inflation.

Chart 3

Paul L. Kasriel

AuthorMore in Author Profile »Mr. Kasriel is founder of Econtrarian, LLC, an economic-analysis consulting firm. Paul’s economic commentaries can be read on his blog, The Econtrarian. After 25 years of employment at The Northern Trust Company of Chicago, Paul retired from the chief economist position at the end of April 2012. Prior to joining The Northern Trust Company in August 1986, Paul was on the official staff of the Federal Reserve Bank of Chicago in the economic research department. Paul is a recipient of the annual Lawrence R. Klein award for the most accurate economic forecast over a four-year period among the approximately 50 participants in the Blue Chip Economic Indicators forecast survey. In January 2009, both The Wall Street Journal and Forbes cited Paul as one of the few economists who identified early on the formation of the housing bubble and the economic and financial market havoc that would ensue after the bubble inevitably burst. Under Paul’s leadership, The Northern Trust’s economic website was ranked in the top ten “most interesting” by The Wall Street Journal. Paul is the co-author of a book entitled Seven Indicators That Move Markets (McGraw-Hill, 2002). Paul resides on the beautiful peninsula of Door County, Wisconsin where he sails his salty 1967 Pearson Commander 26, sings in a community choir and struggles to learn how to play the bass guitar (actually the bass ukulele). Paul can be contacted by email at econtrarian@gmail.com or by telephone at 1-920-559-0375.

Global

Global