Global| May 04 2026

Global| May 04 2026Global MFG PMIs Sweep Higher: Damn the Torpedoes!

You may recognize the excerpted headline quote as ‘borrowing’ from U.S. Admiral David Farragut. It is a famous quote from a U.S. Civil war battle in which he charged ahead in his ship regardless of the risk. This month the global manufacturing PMIs themselves are charging ahead regardless of the rise of inflation, the war in Ukraine, the war in Iran, the closure or impedance in the Strait of Hormuz, and the mucking up of oil and nonoil supply lines. Full speed ahead!

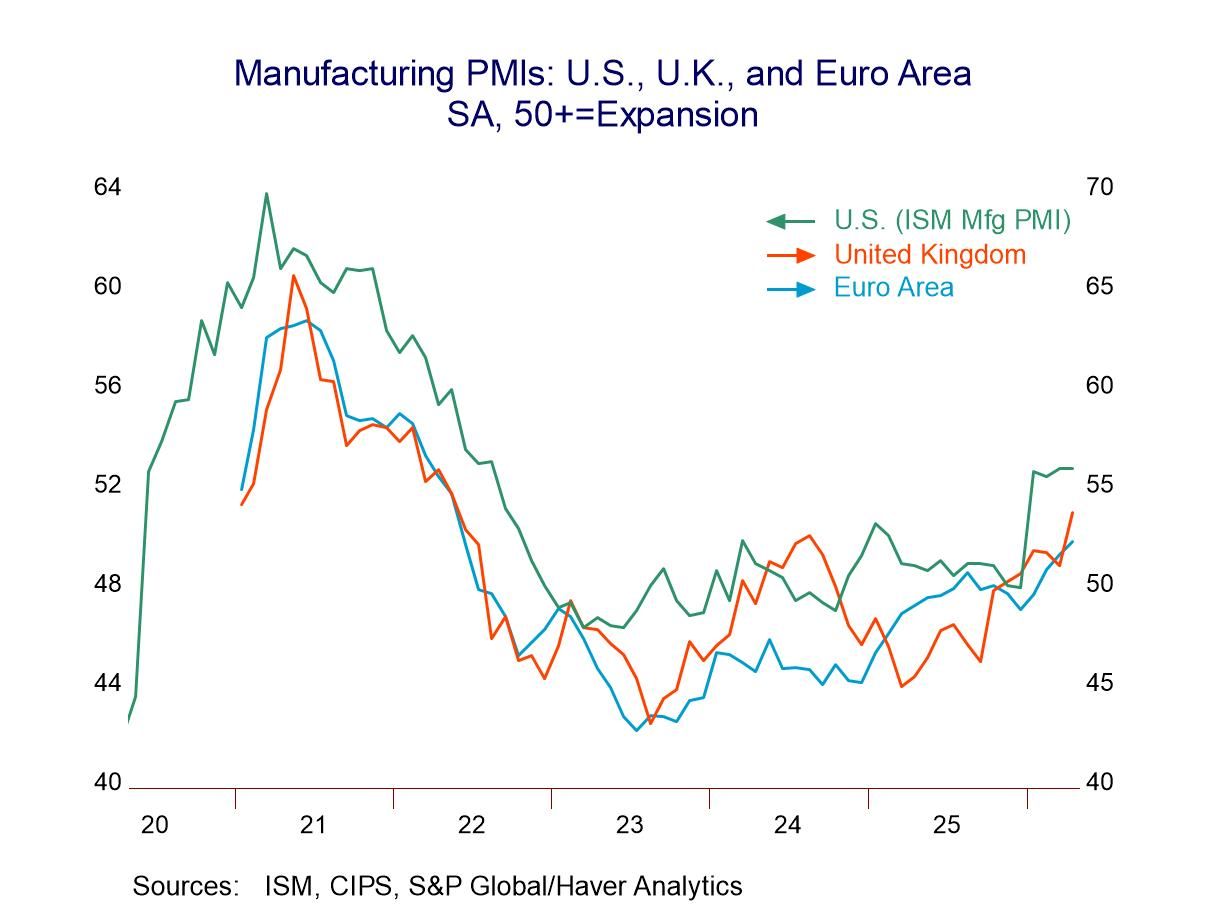

Trend... The chart shows an ongoing recovery in manufacturing. It also shows that conditions are only ‘better’ and not ‘strong.’ Yet when we rank these individual PMIs against their historic results back to January 2022, the median rank across these 18 reporters is 90.8%, signaling that they have been higher less than 10% of the time back to 2022. Of course, 2022-2023 represented low points for manufacturing after COVID. There was a strong recovery from COVID and then the sucker-punch from the invasion of Ukraine by Russia. Nonetheless, on that timeline, recovery is still in progress and—so far—not even the war in the Middle East and other geopolitical turmoil, including a real donnybrook within NATO, has sidetracked it, despite the impact on oil prices. That may not last, but it is the current situation.

A test for central banks With inflation rising, central banks are being put to the test. They failed the post-COVID test and waited too long to hike rates. We did get recovery but inflation, too. Will they do that again? Or will they hike rates sooner? Will they try not to make the same mistake and make, instead, a new mistake by getting too tight too soon? Markets simply do not know. But in the U.S. and U.K., there are five years of missing monetary inflation targets, and in other key countries the inflation targets also have been broadly missed, even if headline inflation recently had dipped into the target range in the last few months or so. Central banks are facing a challenge after their last challenge was not met with success and after a relatively long period—a solid legacy—of missing on the promises they made to the public on inflation.

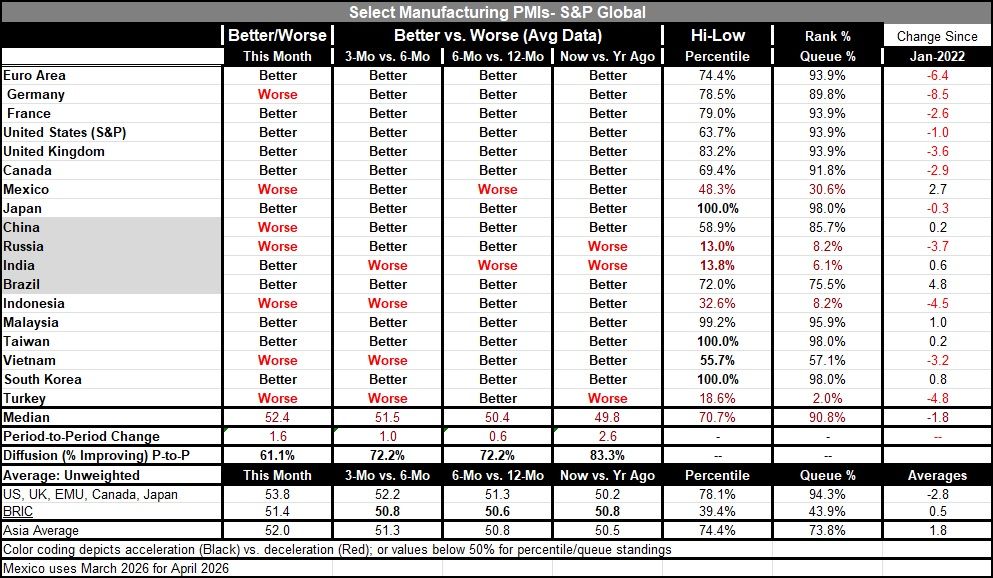

Solid PMI trends: The sequential, as well as the current, monthly data show how widespread change has been tilted in a positive direction. While conditions are broadly better, the current month’s median reading is only at a PMI value of 52.4. So, manufacturing conditions are only slightly above breakeven (a PMI of 50), but they have been weak for so long that this is an exceptionally strong reading compared to the last four and half years of results.

Some examples: The weak manufacturing readings on the month by ranking are for Turkey, Russia, India, and Indonesia. However, these are own-PMI comparisons, and India is one of the strongest readings in April on a cross-section basis (compared to other countries in April, rather than to its own history) having the third strongest manufacturing reading in April. Malaysia, South Korea, Taiwan, and Japan each have the strongest readings (or nearly so) since January 2022; as a result, Taiwan and Japan also rank one and two among 19 reporter readings in April. South Korea ranks sixth. But Malaysia has been so weak; it still ranks only 11th despite a 99.2% high-low standing.

In Sum: The bottom line is that recovery has not been derailed—yet. But this is only an April report. Given time, this rebound could be untracked. It is only a rebound from the lows. So, the expansion is still at risk, even with global labor markets still tight based on unemployment readings. Economic growth is a slippery slope; the trend is only your friend until it turns on you.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief