European Retail Sales Dither While Auto Registrations Weaken

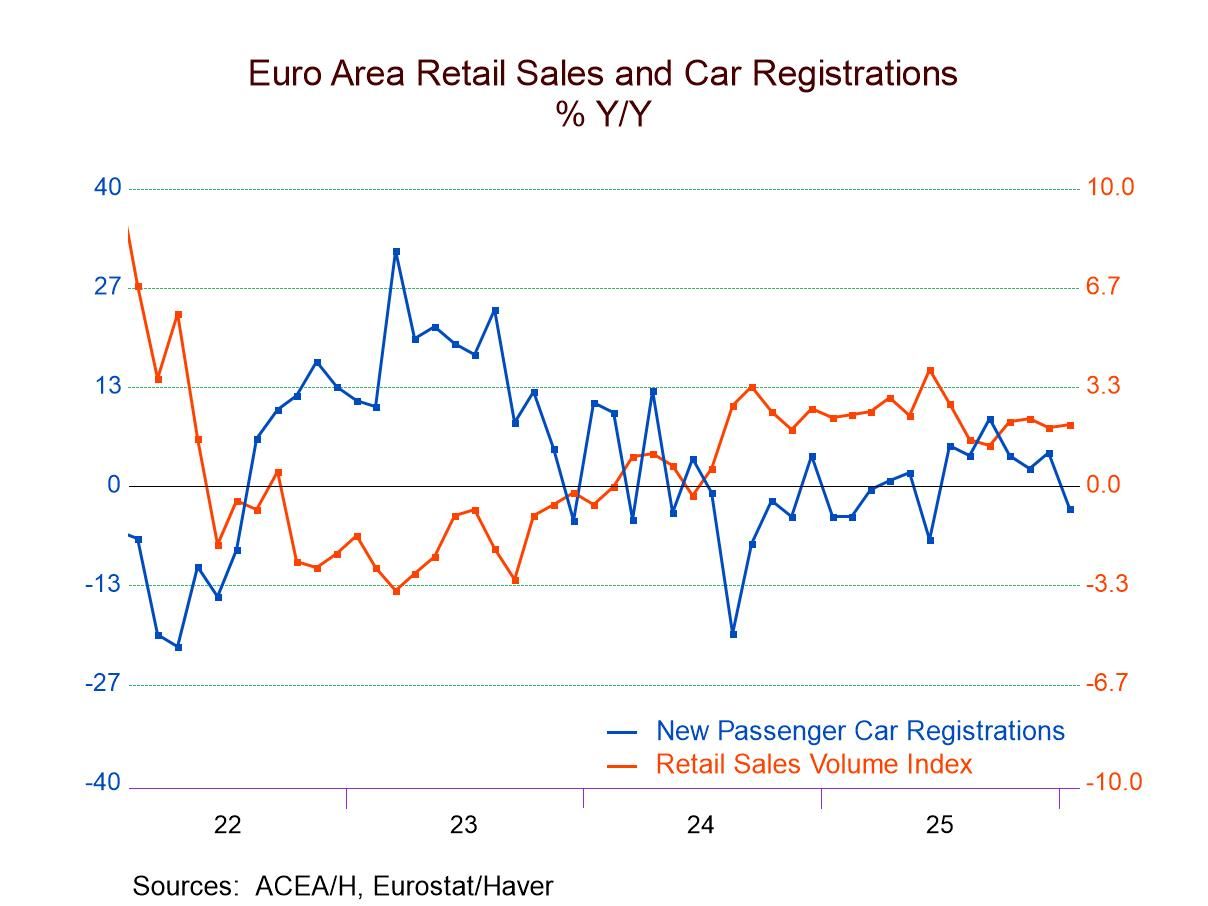

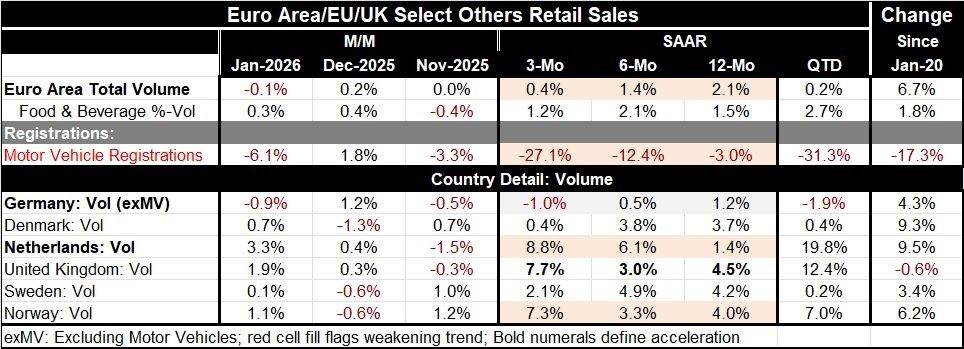

Motor vehicle registrations in January fell by 6.1%, while overall retail sales volume, a separate category, fell by 0.1%. Motor vehicle registrations are notoriously volatile; they increased by 1.8% in December and fell by 3.3% in November. Retail sales, however, have been more chronically flat, with no change in November, a 0.2% increase in December, and now a 0.1% decline in January. These numbers are quite weak because they're already inflation-adjusted, expressed in volume terms.

Sequentially volume sales are weakening in the EMU, with the growth rate slipping from 2.1% over 12 months to a 1.4% pace over six months to just a 0.4% annual rate gain over three months. Food sales have been more stable but have been somewhat more erratically weakened over this same period. Motor vehicle registrations have been imploding, falling by 3% over 12 months, dropping to a 12.4% annual rate over six months and plunging at a 27.1% annual rate over three months.

In the unfolding quarter to date, with one month's data in hand, first quarter retail sales are rising at a 0.2% annual rate; food sales are rising at a 2.7% annual rate. Motor vehicle registrations are declining at a 31.3% annual rate.

We can also inspect these data on a country by country basis. We have Germany and the Netherlands from the European Monetary Union, Sweden and Norway representing Northern Europe, the United Kingdom as a nonaligned former monetary union member, and lastly Denmark as an EU member.

Germany is the largest economy in Europe, and its sales fell in January. More disconcerting, sales in Germany are generally on a decelerating path, growing at a 1.2% pace over 12 months, at a 0.5% pace over six months, and contracting at a 1% annual rate pace over three months. The Netherlands, another monetary union member, is experiencing a very different trend, with sales rising by 3.3% in January and then accelerating from 12 months to six months to three months as growth rates have progressed from 1.4% to 6.1% to 8.8%, respectively. In Denmark, a European Union member but not a monetary union member, sales rose by 0.7% in January, while its sequential sales show growth rates of 3.7% over 12 months and 3.8% over six months, and then suddenly weaken to 0.4% over three months.

The United Kingdom is showing a progression of sales that is fairly firm. In January, sales rose by 1.9%. The annual growth rate is at 4.5% over 12 months, easing slightly to 3% over six months, and then jumping to 7.7% over three months.

Sweden and Norway are fellow Northern European economies but do not share the same trends in retail sales. In January, Swedish sales rose by 0.1%, while Norwegian sales rose by 1.1%. The progression of growth rates in Sweden shows sales over 4% over six months and 12 months, with the growth rate decelerating to 2.1% at an annual rate over three months. In Norway, 12-month and 6-month growth rates for sales are at 3% to 4% and then jump to a 7.3% annual rate over three months.

Monthly data on sales volume growth have been irregular. January was the most consistently strong month of the most recent three, albeit with Germany posting a significantly large drop in retail sales, which is disconcerting for the largest economy in the euro area.

The sequential data show sales accelerations in the Netherlands and in Norway juxtaposed once again to Germany, where sales growth rates are decelerating and culminate in declining growth over the most recent three months. Sequential data also show a clear deceleration in sales volumes for the euro area as a whole. In addition, there is a significant sales implosion for motor vehicle registrations on the same timeline.

The quarter-to-date data for the euro area show weak sales growth, while the country level data show sales increasing for all the countries in the table except Germany in the quarter to date, which is a nascent calculation at this point.

From here on out, the outlook encounters more cross currents since inflation in the euro area appears to be tamer but continues to run at a pace slightly excessive relative to target. Now with a new conflict in the Middle East and concern about oil being able to squeeze through the Strait of Hormuz, there's a more significant question about how much further oil prices might rise, further stoking inflation that is already mildly excessive in most countries that target inflation. There is an additional facet about uncertainty and the impact it will have on growth, although at this point the war in the Middle East appears to be exceptionally well conducted and appears to be quite contained. However, we know that conditions like this can change quickly, although it's not out of the question that this could be an exception.

These factors infuse the outlook with additional elements of uncertainty. Central banks are going to be faced with the question of whether they are going to allow themselves to continue overshooting their targets as they have been doing for some time, or whether they are going to take even mild steps to try to contain what could be spreading inflation pressures.

In Asia, Japan is facing more extreme questions, with its exchange rate having moved strongly and its Prime Minister wanting to put monetary tightening on hold to solidify an economic expansion despite the fact that inflation has been running on the hot side. And in the United States, political pressures continue to tear at the political fabric, and it faces midterm elections at the end of the year; both parties are preparing for and posturing for that event. The year ahead could prove to be interesting in either a desirable or an undesirable way - stay tuned.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global