EU Indexes Show European Improvement in June

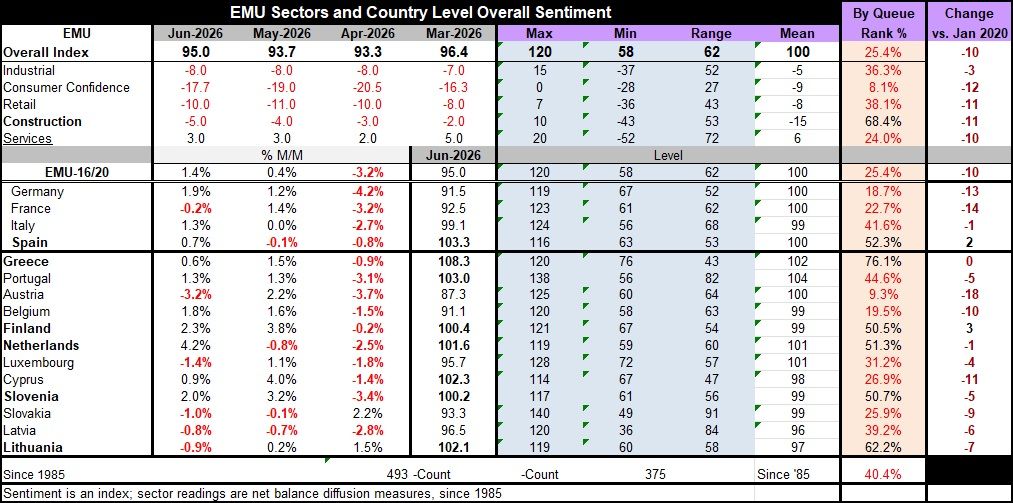

Headline indexes for the European Monetary Union improved in June to a reading of 95.0 from 93.7 in May. The index had been stronger at 96.4 in March; however, it fell to 93.3 in April, recovered slightly to 93.7 in May, and has now reached 95.0. While still below its March high, the index has made progress in the wake of the outbreak of war-like conditions and the closure of the Strait of Hormuz.

Sector performance The industrial reading for the sector, at -8, has a 36.3 percentile standing, which better than the headline index for the Monetary Union with a 25.4 percentile standing. The EMU-wide sector index, consumer confidence, improved to a net diffusion reading of -17.7 in June from -19 in May, but that still leaves it with a very weak 8.1 percentile standing, the lowest among sector readings. Retailing improved to a net diffusion reading of -10 in June from -11 in May and posted a 38.1 percentile standing. The construction sector deteriorated, falling back to -5 from -4 in May; it has been undergoing steady degradation since at least March, but it still has a 68.4 percentile standing. It is the only sector with a percentile standing above 50, placing it above its historic median. The services sector had a net diffusion reading of +3, identical to its May reading and has a 24-percentile standing.

Sector index ranking The sector readings clearly show that the monetary union is exhibiting a number of sectors with subpar growth; beyond ‘subpar,’ many are quite weak. The exception is—and has been for some time—the construction sector, which continues to perform above average and post an above-median metric. It is, perhaps surprising that we often think of consumer confidence as being relatively forward-looking, but in this schematic, consumer confidence is the weakest of the sectors; in fact, like statistics from the U.S., we find the same prevailing situation with consumer readings exceptionally weak. These weak consumer readings coexist with much stronger retailing readings and stronger industrial readings, although both of those are below their historic medians in Europe. This report is a sort of gut check for what consumer confidence means; it may not be as important as we used to think it was. Although the business cycle at this juncture seems to be concentrated more on the supply side and on recovery in the business community, that effect compounded by the influence of AI is much stronger in the U.S. than in Europe.

Country detail – Large economies The country detail shows 16 of 20 early reporting countries with only one of the top four countries showing a decline month-to-month, and that's France. France recorded a 0.2% decline in June, while Germany posted a 1.9% increase, Italy gained 1.3%, and Spain rose 0.7%. Spain had the lone small decrease in May, while in April all of the large countries showed significant monthly declines in their overall indexes in the wake of the onset of the war with Iran.

Smaller economies in EMU Apart from the Big Four economies, 12 other EMU members report in June; of those, 5 showed month-to-month declines in their country level indexes. This was up from three showing declines in May, although it was a vast improvement from April, when all of the country indexes turned negative and generated substantial month-to-month declines, except for Slovakia and Lithuania.

Big Four economy rankings Among the Big Four economies, the strongest ranking reading in June is Spain at a 52.3 percentile standing, followed by Italy at a 41.6 percentile standing, France at a 22.7 percentile standing, and Germany at an 18.7 percentile standing.

Other economy rankings Among the other 12 countries, the percentile standing readings range from a high of 76.1% for Greece to a low of 9.3% for Austria. Five of 12 of the smaller EMU members have percentile standings of 50% or greater, putting them above their historic medians, while the other 7 have rankings that range from a high of 44.6% in Portugal to a low of 9.3% in Austria.

Summing up Conditions in the monetary union have improved over the last two months after a substantial stumble in the wake of the war in the Middle East with Iran and the closure of the Strait of Hormuz. However, the rebound in the European recovery is in gear; it is slow and measured. Conditions are still weak on balance.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Asia

Asia