Asia| Sep 08 2025

Asia| Sep 08 2025Economic Letter from Asia: Political Woes

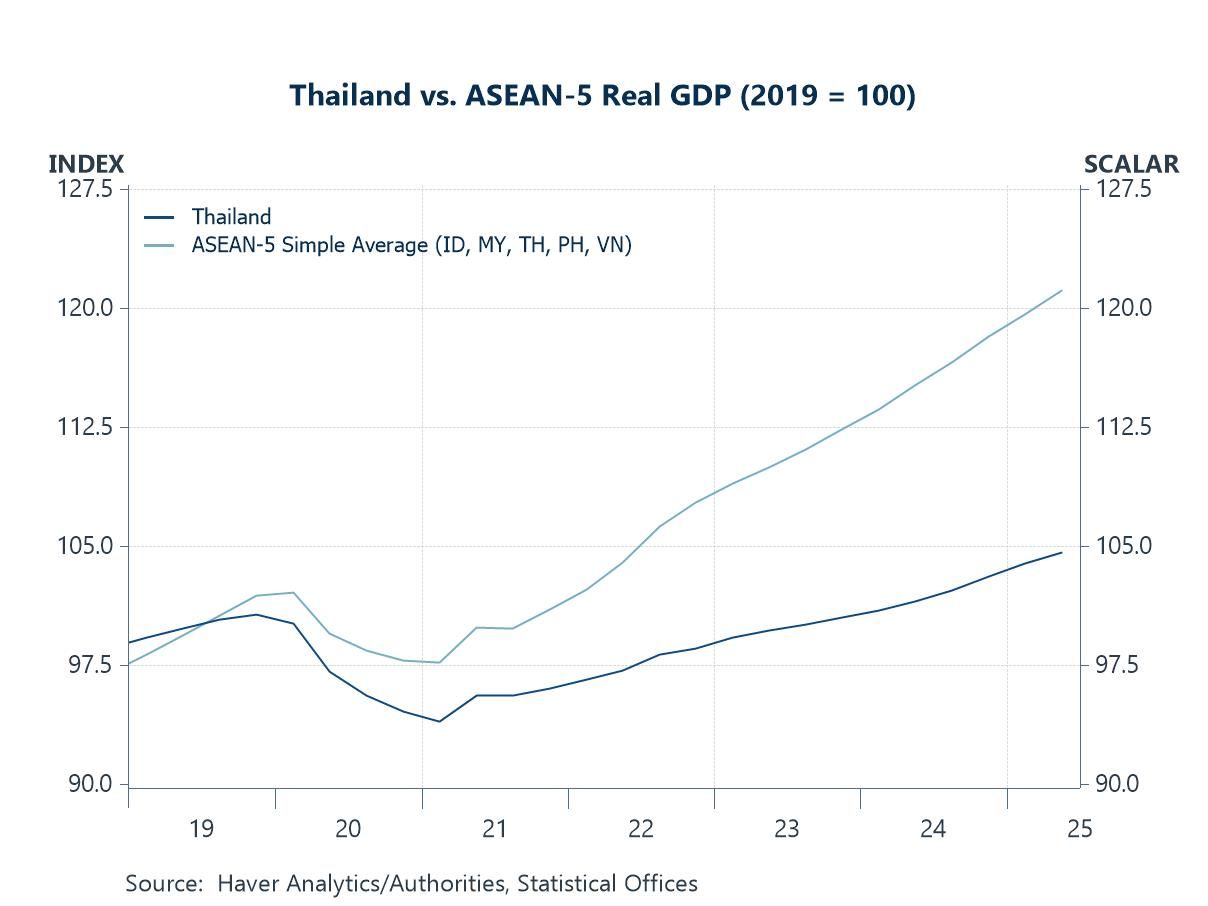

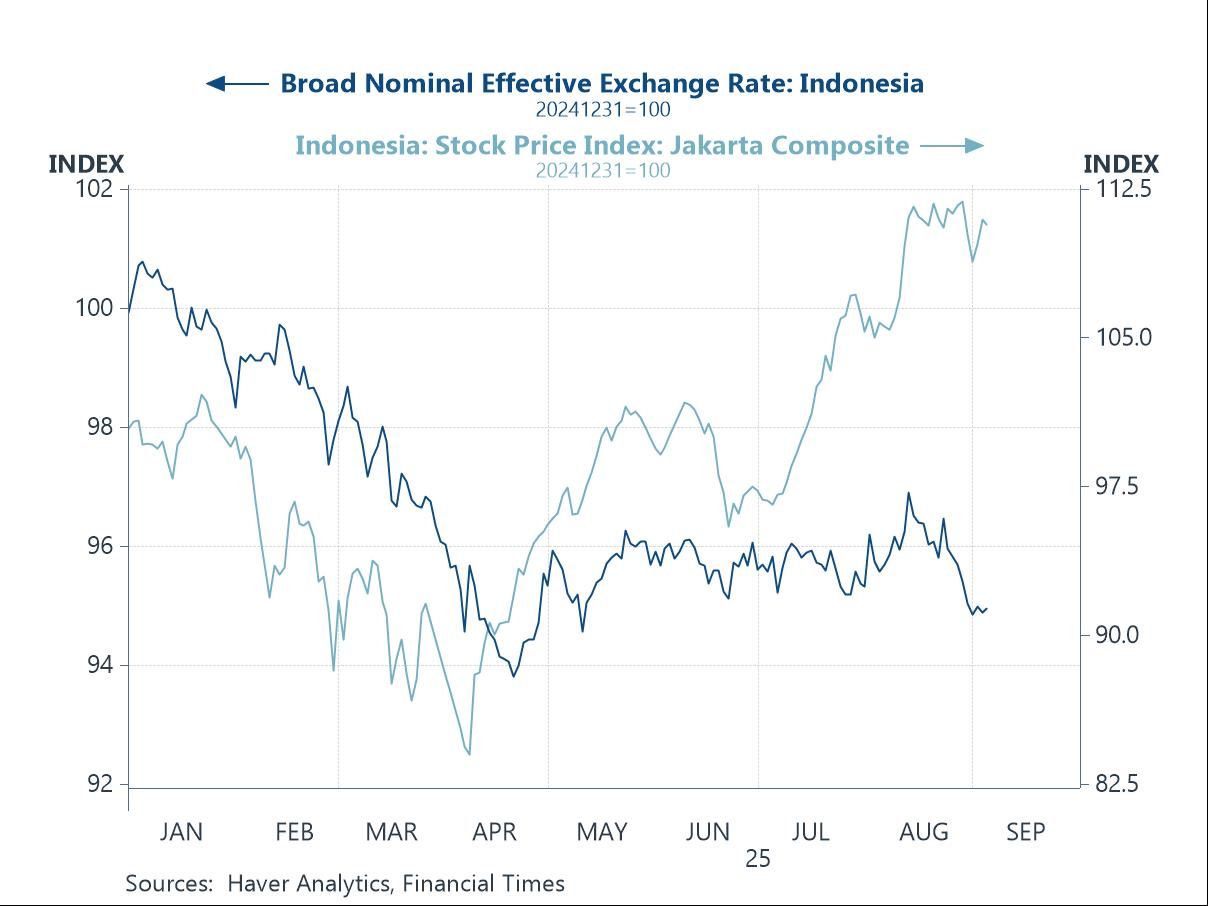

This week, we review the state of play in Southeast Asia and Australia. In Thailand, political uncertainty lingers after the removal of former Prime Minister Paetongtarn, with investors now eyeing fresh elections in the coming months. The ongoing political flux has only deepened concerns over Thailand’s persistent economic underperformance relative to regional peers (chart 1). Indonesia, too, has faced recent political turmoil, as protests over lawmakers’ housing allowances turned violent. While tensions have since eased and financial markets partially recovered (chart 2), the episode highlighted the fragility of investor confidence.

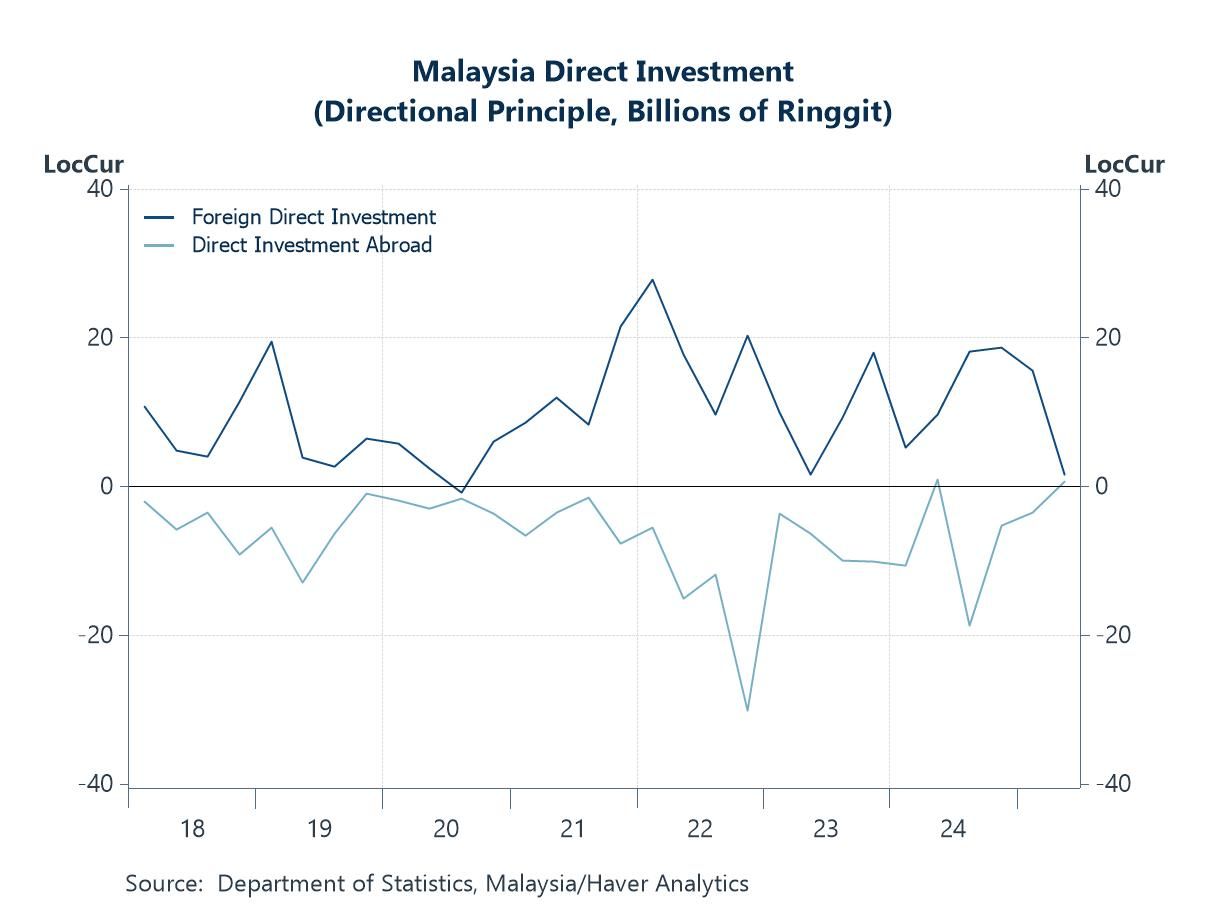

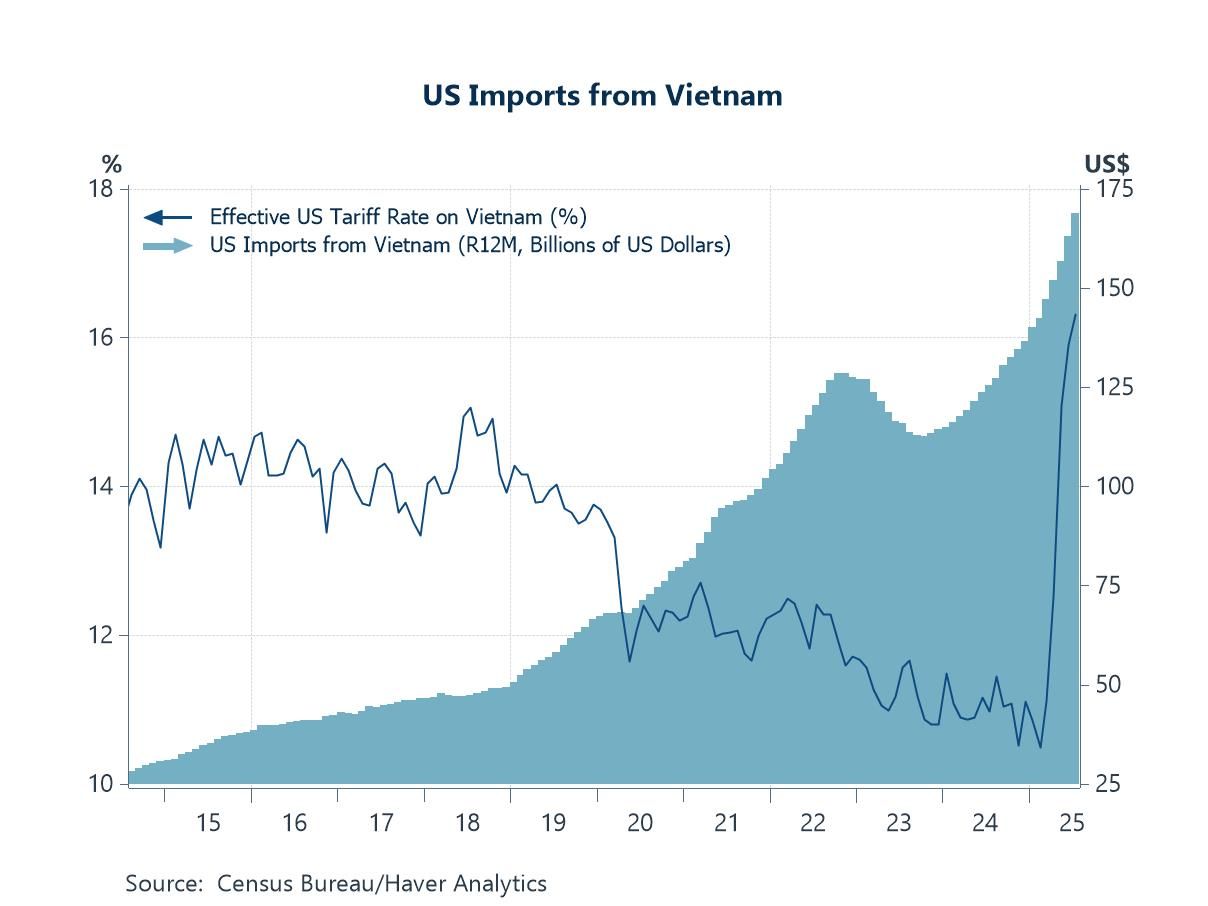

Elsewhere in Southeast Asia, some economies are pressing ahead. Malaysia has made significant strides in establishing itself as a global tech hub, supported by robust direct investment flows (chart 3). Vietnam, likewise, continues to position itself as a manufacturing and electronics powerhouse. Its strong export performance has driven growth but also drawn scrutiny, particularly as the US trade deficit with Vietnam has widened alongside rising imports (chart 4).

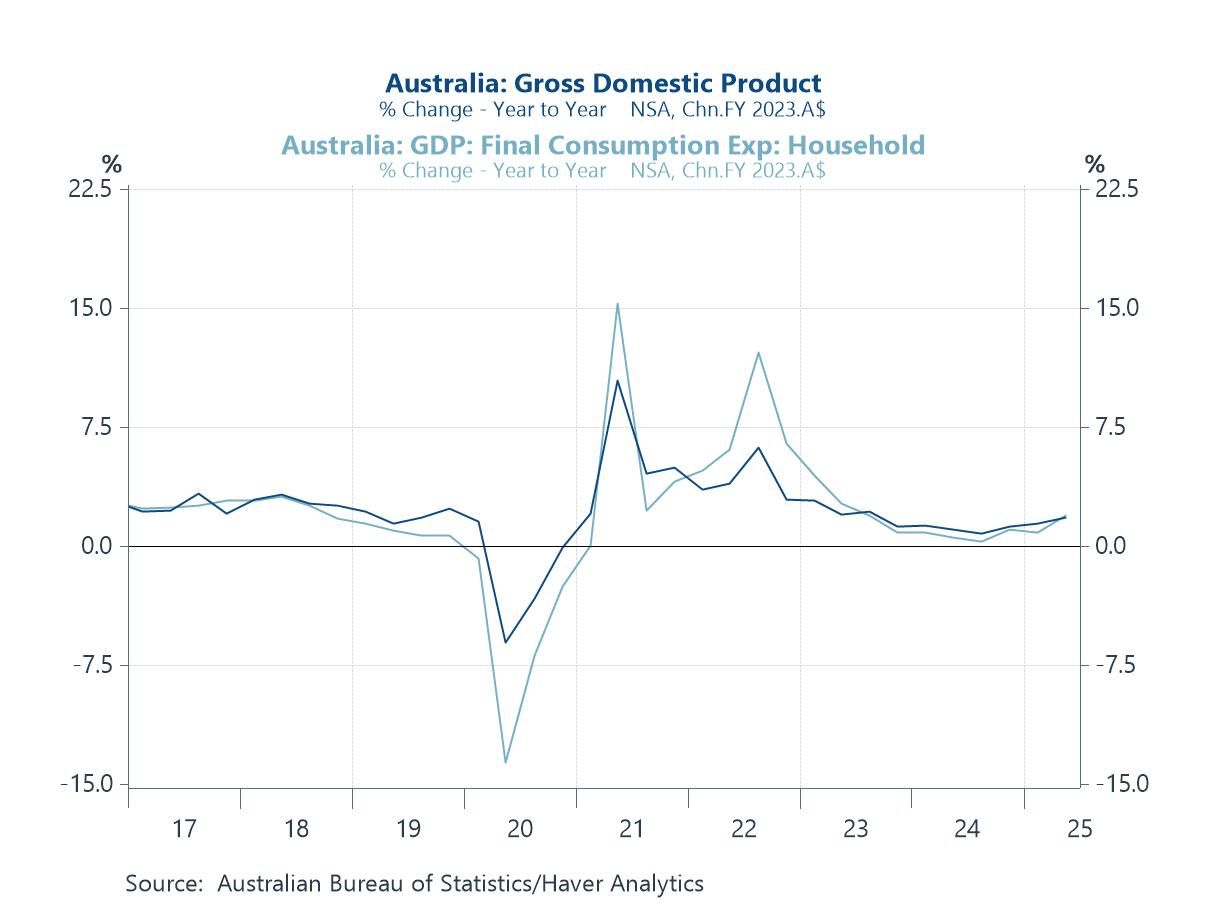

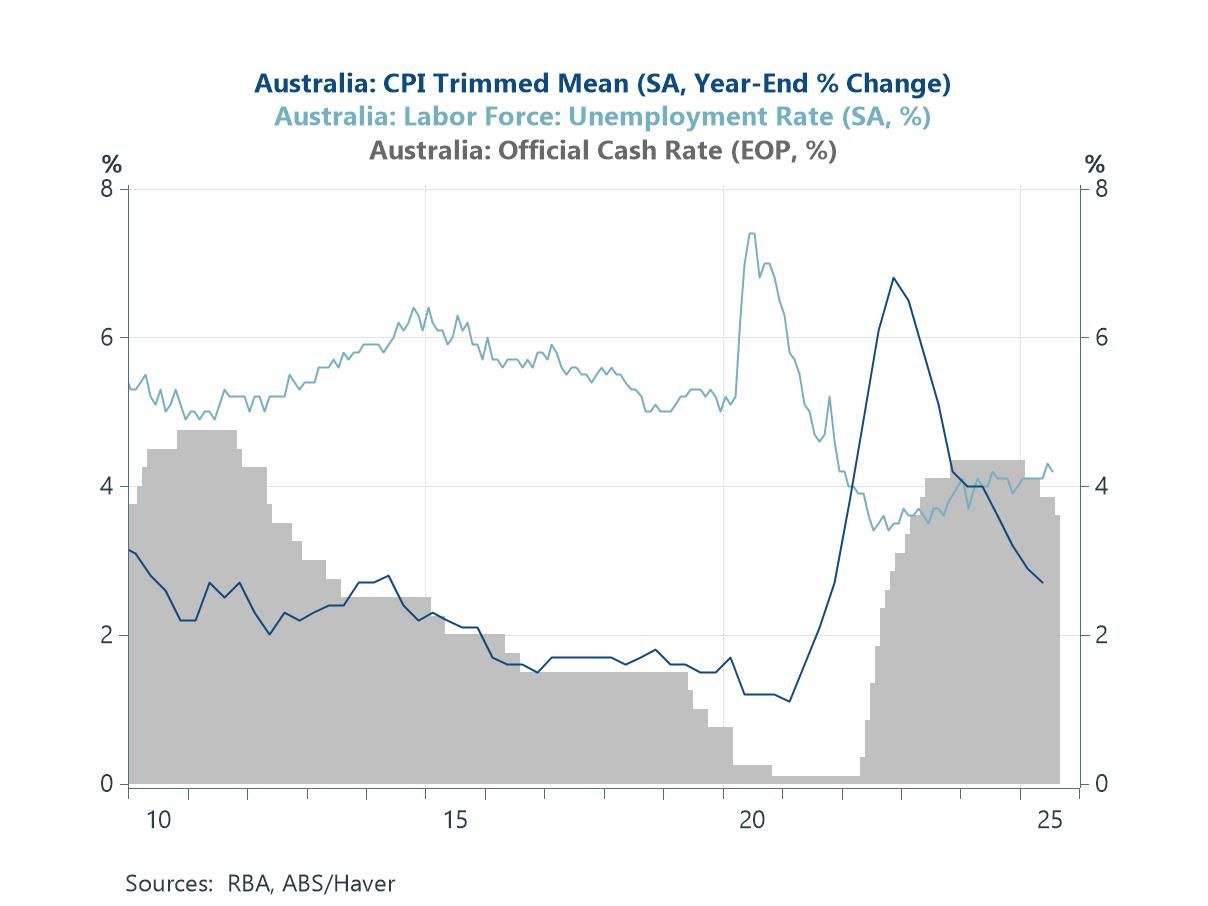

In the Pacific, Australia has shown encouraging signs, with Q2 GDP growth outperforming expectations on the back of stronger household consumption (chart 5). This has bolstered expectations that the RBA will pause rate cuts at its month-end meeting. Even so, close attention remains on the labour market (chart 6), potential headwinds from US tariffs, and a broader productivity challenge.

Thailand Thailand continues to struggle to regain its footing, weighed down by ongoing political turmoil. Former Prime Minister Paetongtarn was removed from office by the Constitutional Court in late August, following her July 1st suspension over a leaked phone call with former Cambodian leader Hun Sen. In her place, lawmakers elected former Deputy Prime Minister Anutin as the new premier. However, as part of the deal that secured his appointment, Anutin has pledged to dissolve parliament within four months and call a general election. This political upheaval compounds Thailand’s broader economic challenges. Growth has persistently lagged behind its Southeast Asian peers (chart 1), with tourism—a key revenue source—stalled and still short of pre-pandemic levels. At a time when deeper reforms are needed to unlock the country’s full potential, Thailand instead faces prolonged political flux, leaving policy clarity and direction uncertain even as neighbours forge ahead.

Chart 1: Thailand vs. ASEAN-5 Real GDP

Indonesia Thailand is not alone in Southeast Asia in grappling with political turmoil. Indonesia has recently faced its own unrest, as initially peaceful demonstrations against housing allowances for lawmakers turned violent after a motorbike taxi driver was fatally struck by a police vehicle during an earlier rally in Jakarta. Although protests have since subsided, the turmoil comes on the heels of policy moves that have already unsettled some investors. Concerns have centred on the fiscal strain from large-scale spending programs such as Prime Minister Prabowo’s free school meals initiative. While the program is well-intentioned—aimed at reducing poverty and improving child development—its hefty cost implies spending cuts elsewhere and higher taxes, fuelling unease. Markets have reflected these concerns, with Indonesian equities and the rupiah selling off during the recent protests, though both have staged a partial rebound as tensions eased (chart 2).

Chart 2: Indonesian rupiah and equities

Malaysia While Thailand and Indonesia have been grappling with political woes, other Southeast Asian economies have pressed ahead. Malaysia, for instance, has made notable strides in establishing itself as a global tech hub, with significant advances in semiconductors—largely centred in Penang—and, more recently, in electric vehicles, where Malacca is emerging as a key industry hub. These developments have been fuelled in part by strong foreign investment flows, which, while healthy in recent years (chart 3), slipped to a five-year low in Q2 2025 on a directional basis. Still, Malaysia’s semiconductor push remains robust: Prime Minister Anwar announced earlier this year that the country had already secured more than 63 billion ringgit ($14.9 billion) in semiconductor investments, mostly from foreign sources, under its National Semiconductor Strategy—less than a year after the scheme’s launch. More broadly, Malaysia has pressed ahead on multiple fronts in its drive toward high-income status by 2030—an ambition that is looking increasingly attainable.

Chart 3: Malaysia direct investment

Vietnam Moving to Vietnam, the economy—like Malaysia’s—has been pushing hard to establish itself as a manufacturing and electronics hub. Vietnam continues to outpace its ASEAN peers in growth and shares Malaysia’s ambition of reaching high-income status, though with a later target of 2045. Its export boom has been central to past success but has also drawn scrutiny, particularly as the US trade deficit with Vietnam has widened with rising imports (chart 4). As a result, Vietnam now faces a more constrained trade environment even as it relies on exports as a key growth driver. For now, Vietnam has avoided a worst-case scenario with the US: a recent trade deal reduced the reciprocal tariff rate from a potential 46% to 20%, though US-perceived “transshipments” will still be hit with a 40% tariff. Beyond navigating this delicate global landscape, Vietnam is also instigating deep structural reforms—such as strengthening the role of the private sector—to sustain growth and meet its long-term development goals.

Chart 4: US imports from Vietnam

Australia Moving to the Pacific, Australia is among the few economies relatively insulated from US tariffs, facing only the baseline 10% rate under the revised tariff schedule that took effect in early August. On the domestic front, Australia’s economy outperformed expectations in Q2, with real GDP growth accelerating to 1.8% y/y. The pickup was driven by stronger household consumption (chart 5), offering an encouraging signal for the outlook and easing earlier concerns about economic momentum—perhaps also suggesting that the central bank’s earlier rate cuts are beginning to take effect.

Chart 5: Australia real GDP and household consumption

Turning to monetary policy, the recent upbeat data have reinforced expectations that the RBA will hold rates steady at its September meeting, after cutting a cumulative 75 bps since the start of the year. That said, markets are still pricing in further easing down the line, supported by Australia’s disinflationary trend (chart 6) and lingering downside risks from weaker global demand amid US trade tariffs. Another key dimension is the labour market, which remains tight but has shown signs of softening in recent months. A broader concern is productivity, which has stagnated in recent quarters, raising questions about the sustainability of real wage growth.

Chart 6: Australia inflation, unemployment, and policy rate

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief