Asia| May 05 2026

Asia| May 05 2026Economic Letter from Asia: Everybody’s Changing

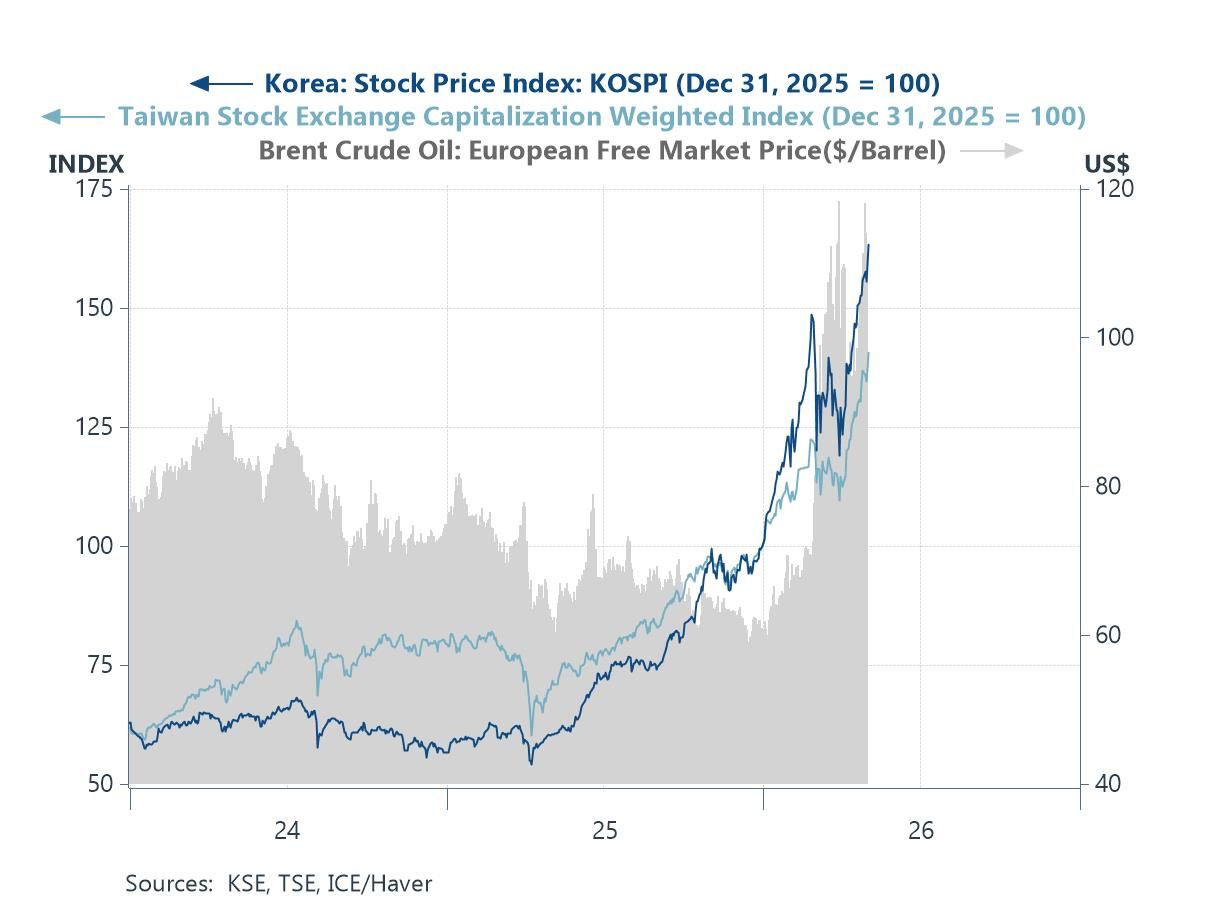

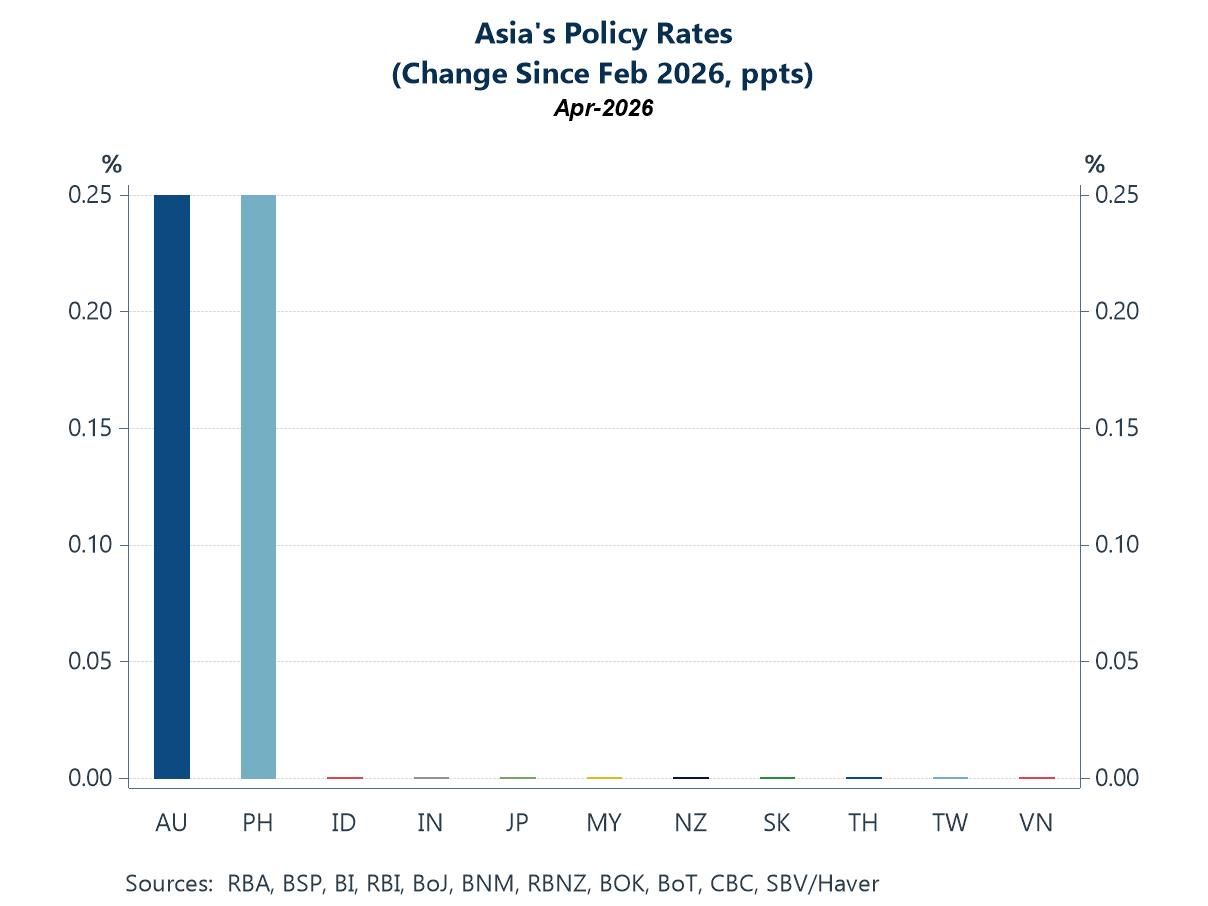

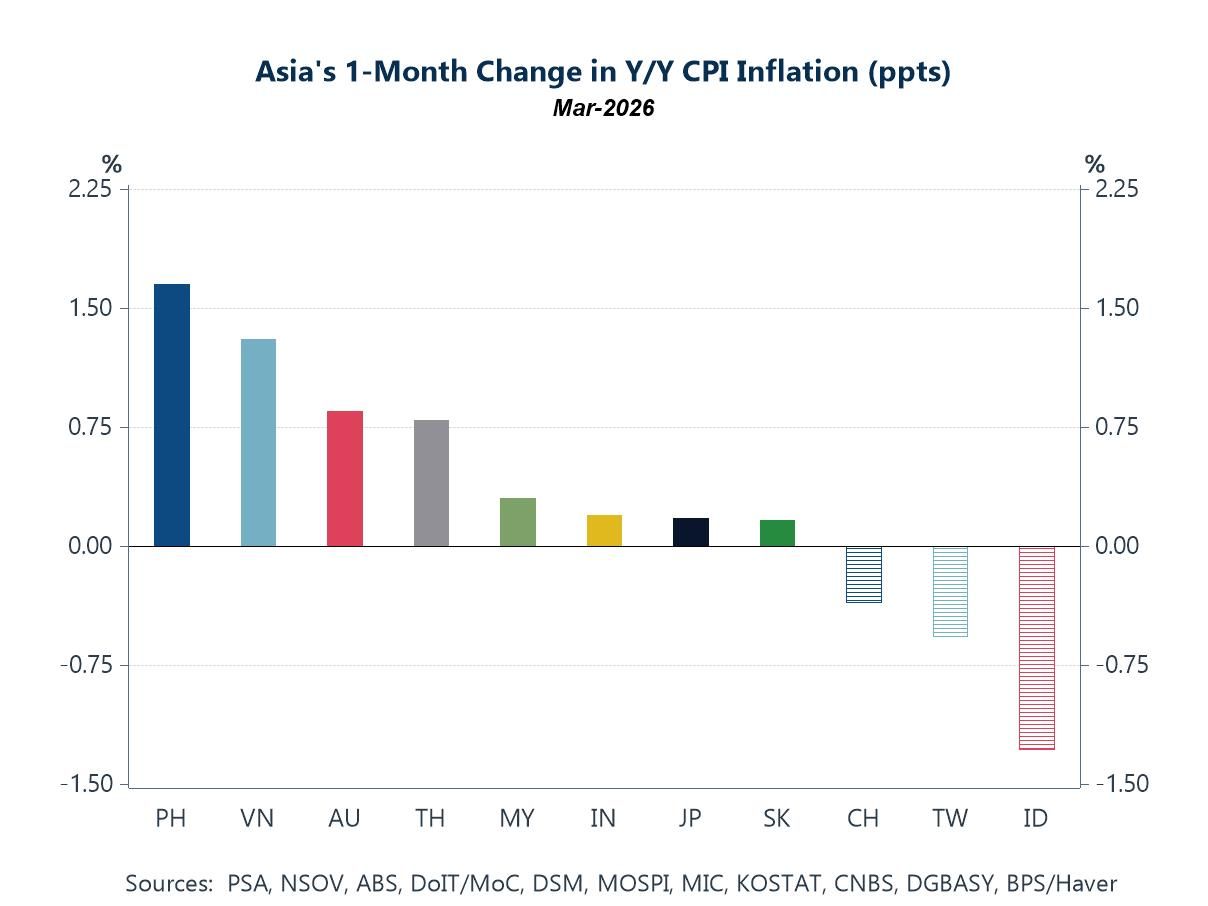

In this week’s Letter, we take another pulse on recent key developments relating to, and affecting, Asia. The week has once again begun on a hopeful note, following reports that the US will guide neutral vessels through the Strait of Hormuz, signalling a partial easing of trade flows through the waterway. Asian markets, including South Korea and Taiwan, were further buoyed by persistent AI-related optimism (chart 1). A full tally of central bank decisions since February highlights a growing divergence across the region. While most central banks have opted to hold back on tightening, a subset has already moved to raise policy rates in response to inflation pressures stemming from higher oil prices (chart 2). A cross-country comparison of consumer inflation reinforces this divergence, with more pronounced CPI increases in economies such as Australia and the Philippines, where central banks have recently hiked rates (chart 3).

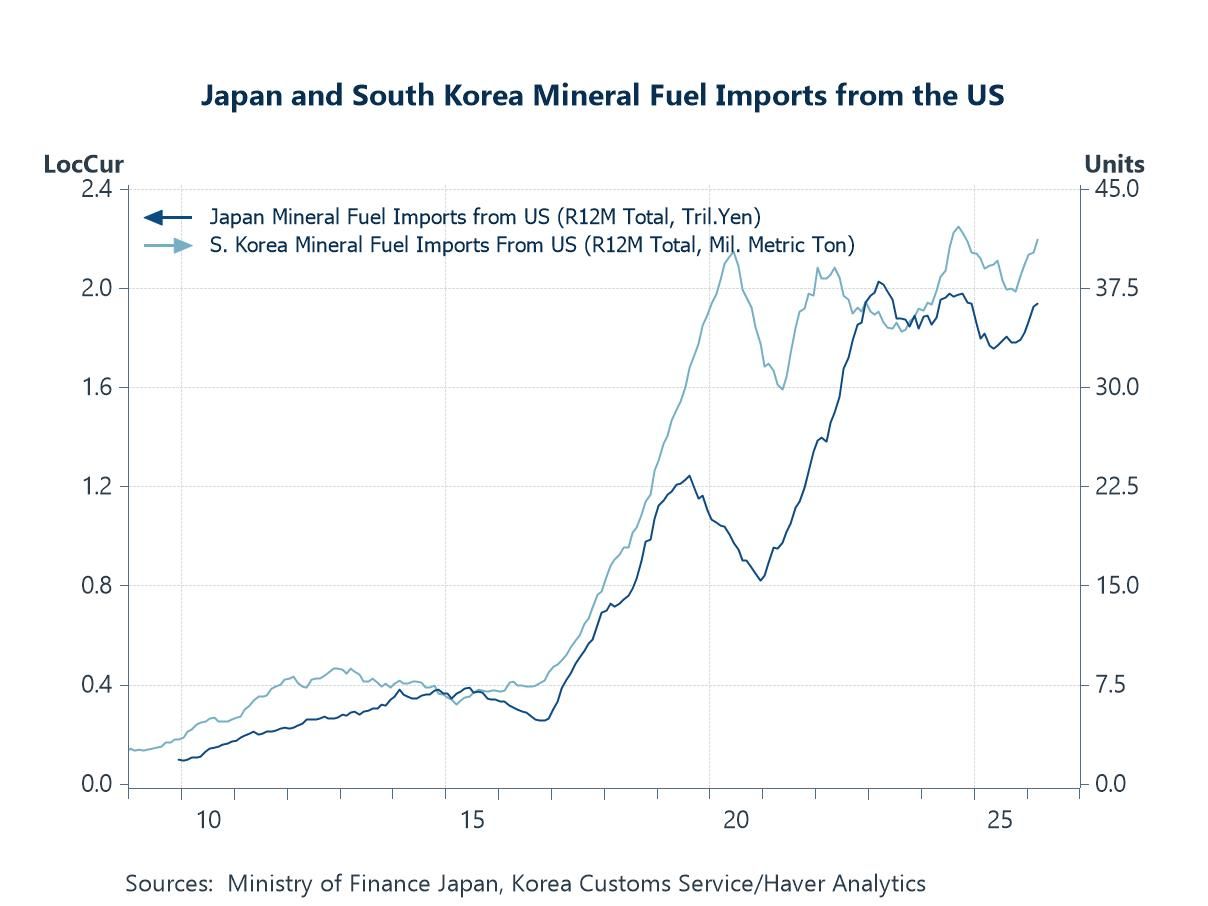

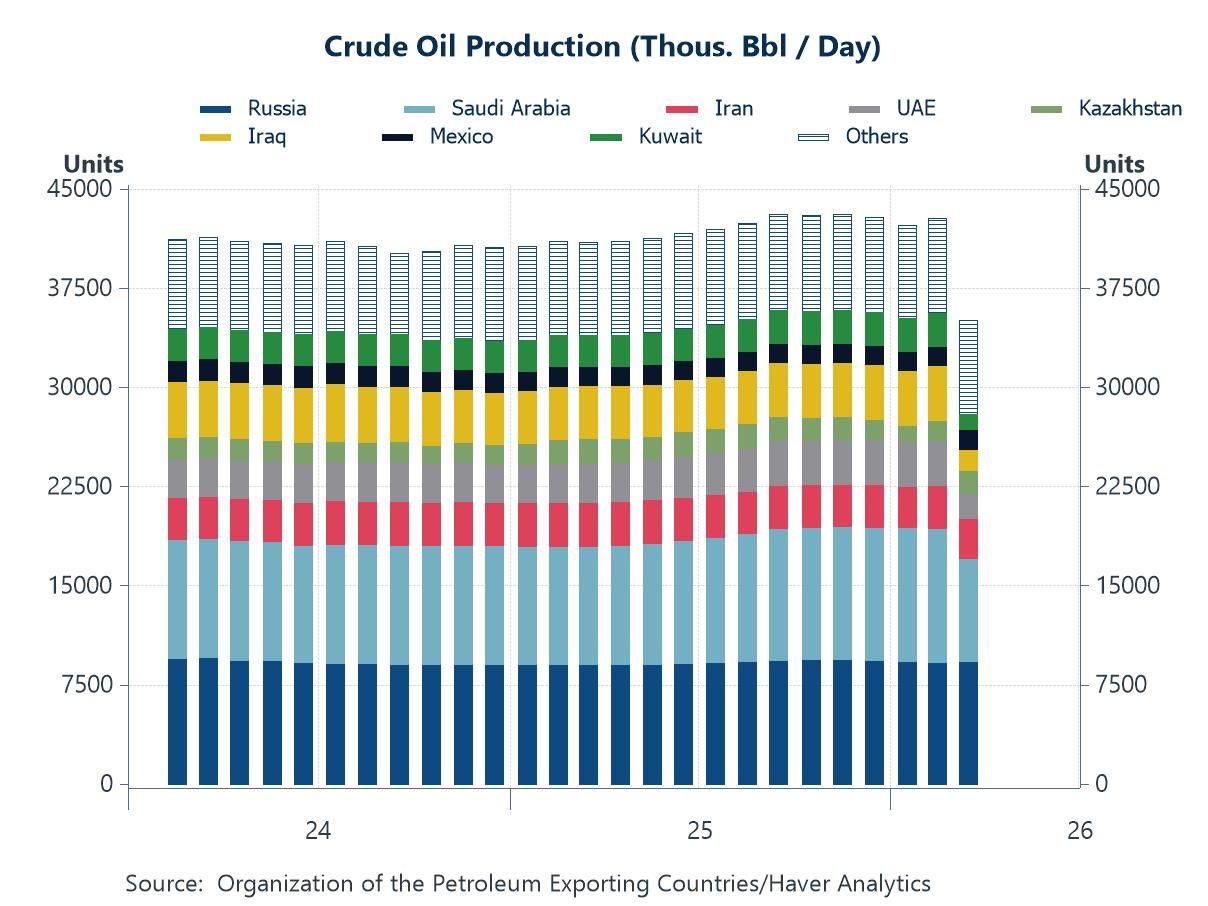

In the meantime, amid the absence of oil flows through the Strait, many Asian importers have begun sourcing supplies from alternative producers, including the United States (chart 4). At the same time, major oil exporters affected by disruptions in the Strait of Hormuz have been forced to scale back crude production significantly due to storage constraints (chart 5). Looking ahead, attention turns to a three-pronged week featuring regional PMIs, additional central bank decisions (chart 6), and further Q1 GDP releases.

Early-week optimism Asian markets began the week on an optimistic footing, supported by developments in the Middle East. Reports that the US will guide neutral vessels through the Strait of Hormuz have lifted expectations of a partial resumption in trade flows through what has been a severely constrained passage. That said, while any reopening of oil and broader shipping routes is a key factor in easing the supply shock stemming from the conflict, the situation remains far from resolved. Uncertainty persists over both the scale and durability of any recovery in shipping activity. Elevated tensions between the US and Iran—underscored by exchanges of fire as US forces escorted vessels through the waterway on Monday—continue to leave the outlook vulnerable to renewed disruption. Nonetheless, ongoing AI-related optimism has continued to underpin equity markets. Asia stands to benefit disproportionately given its central role in the global AI supply chain, helping keep equity prices elevated across key markets such as South Korea and Taiwan (chart 1).

Chart 1: KOSPI, TAIEX, and Brent crude oil prices

Central bank decisions, inflation Given that the Middle East conflict has already persisted for some time, chart 2 shows the first full tally of Asia’s policy rate decisions in April. Most central banks opted to hold their policy rates steady, signalling a broadly wait-and-see approach despite still-elevated and persistent inflation risks. In contrast, a smaller group, including Australia and the Philippines, moved to raise rates, reflecting ongoing inflation concerns. It should be noted, however, that Australia had already been tightening its policy prior to the outbreak of the Middle East conflict. While the majority of central banks have so far refrained from further tightening, this stance should not be assumed to persist. This is particularly true if inflation were to accelerate further, or more critically, if inflation expectations begin to show sustained signs of becoming unanchored. Such dynamics could trigger feedback loops that become increasingly difficult to contain if left unaddressed.

Chart 2: Changes in policy rates in Asia

As such, while the broad policy balance currently leans toward avoiding unnecessary damage to growth while monitoring inflation risks, that equilibrium may soon be forced to shift toward more decisive action if inflation pressures begin to accelerate. Turning to inflation, chart 3 presents a comparison of March CPI inflation readings against February’s, the latter of which preceded the outbreak of the Middle East conflict. The data again highlights recent central bank actions, particularly in Australia and the Philippines, where CPI inflation has picked up, helping to explain the rationale behind their rate hikes. In Vietnam’s case, CPI inflation has also accelerated in recent months. However, the central bank has thus far opted for a more growth-supportive stance. It remains to be seen how long this position can be sustained if inflation continues to build.

Chart 3: Changes in CPI inflation in Asia

Pivotal moves Amid the ongoing constraints in the Strait of Hormuz, Asian economies have already moved to secure oil supplies from alternative sources. In Japan’s case, imports have increasingly shifted toward suppliers such as the US, reflecting the disruption to traditional flows that are heavily reliant on transit through the Strait. South Korea has similarly diversified its sourcing to supplement its energy needs. A comparable trend can be observed across other Asian economies, with oil imports gradually being redirected toward exporters that can deliver shipments without passing through the Strait of Hormuz. While these adjustments represent a pragmatic response to the current supply shock, it remains unclear whether the resulting shifts in market share for alternative suppliers are merely temporary. The crisis has, in any case, reinforced a broader reassessment of energy security and supply chain diversification strategies across the region.

Chart 4: Japan and South Korea mineral fuel imports from the US

Meanwhile, major oil producers affected by disruptions in the Strait of Hormuz, including Saudi Arabia, Iran, and the UAE, have been forced to scale back crude oil production significantly (chart 5). With exports through the Strait effectively constrained, output has increasingly had to be diverted into storage facilities. The UAE’s recent announcement of its departure from OPEC adds an additional layer of uncertainty to the regional production landscape. The key constraint lies in limited storage capacity. Once storage sites approach saturation, additional production cannot be efficiently absorbed, effectively forcing output cuts in the absence of alternative export routes. This bottleneck explains the recent adjustments in production levels across affected producers. Looking ahead, elevated inventory levels could also complicate a normalization of production flows should the Strait conclusively reopen. Producers would likely need to draw down existing stockpiles before meaningfully ramping up output again. In addition, a sufficient return of tanker capacity would be required to facilitate the shipment of accumulated inventories back into global markets.

Chart 5: Global crude oil production

Asia this week It is a three-pronged week in Asia, with regional PMIs, a pair of central bank decisions, and several Q1 GDP releases due. Beyond the region’s manufacturing PMIs released earlier this week, China’s unofficial April services PMI will also be closely watched, helping to complete the month’s activity picture. On the monetary policy front, attention will be on decisions from Australia and Malaysia. Australia, as widely expected, delivered a third consecutive rate hike in response to persistent inflation risks. Malaysia, who is scheduled to announce its decision on Thursday, is seen keeping its policy rate on hold. In addition, Q1 GDP readings from the Philippines are due over the course of the week. Meanwhile, in markets, Japan-focused attention is likely to remain on the yen amid ongoing talk about authorities’ intervention in response to recent weakness.

Chart 6: Australia inflation and policy rate

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.