Asia| Oct 20 2025

Asia| Oct 20 2025Economic Letter from Asia: Clearing the Fog

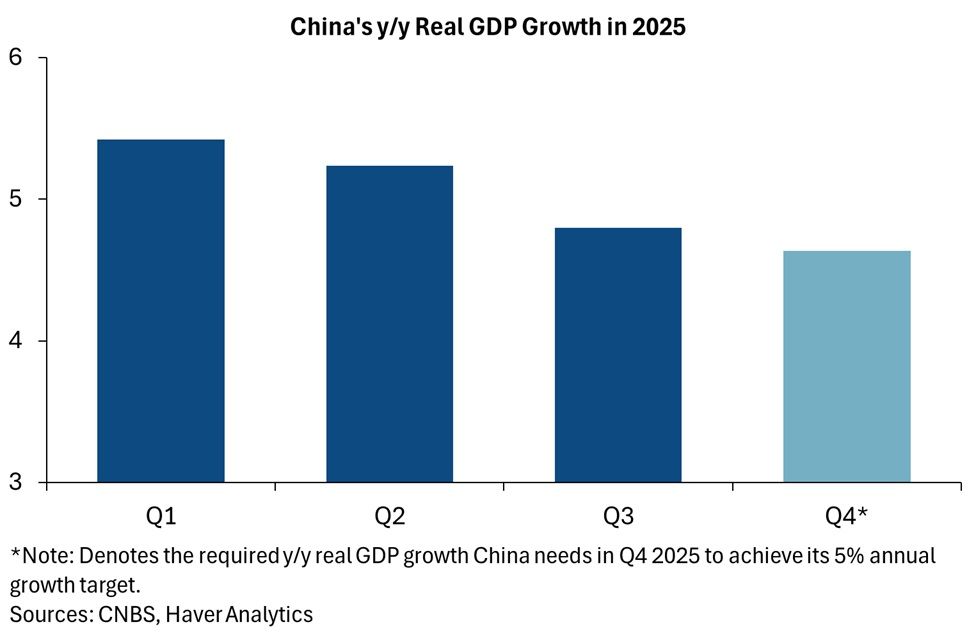

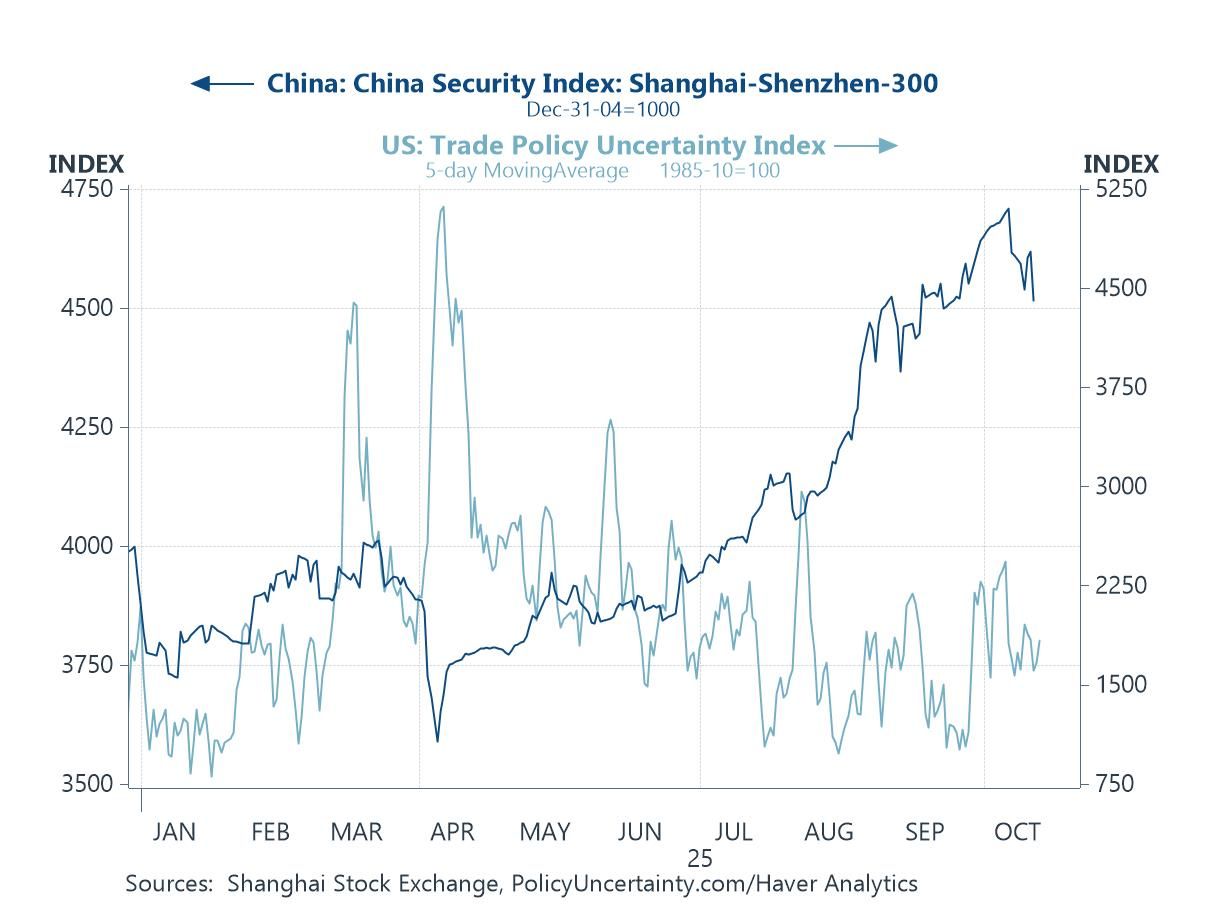

This week, we examine key developments across China, Japan, and the broader Asian region. In China, the Q3 GDP outturn extended the recent trend of slowing growth amid a still-fluid external backdrop and uneven domestic performance. While exports—and almost by extension, industrial production—continued to support growth, domestic demand remained soft, with retail sales and the property market still facing headwinds (chart 1). Nonetheless, despite growth moderating to 4.8% y/y, a mild source of comfort is that China remains on track to meet its 5% annual growth target, even if Q4 growth eases further to around 4.6% y/y (chart 2). Externally, uncertainty persists. US-China tensions have resurfaced, dampening sentiment in Chinese equity markets after initial post–Golden Week resilience (chart 3). All eyes are now on US-China talks in Malaysia and the Fourth Plenum in Beijing this week for potential policy or strategic signals.

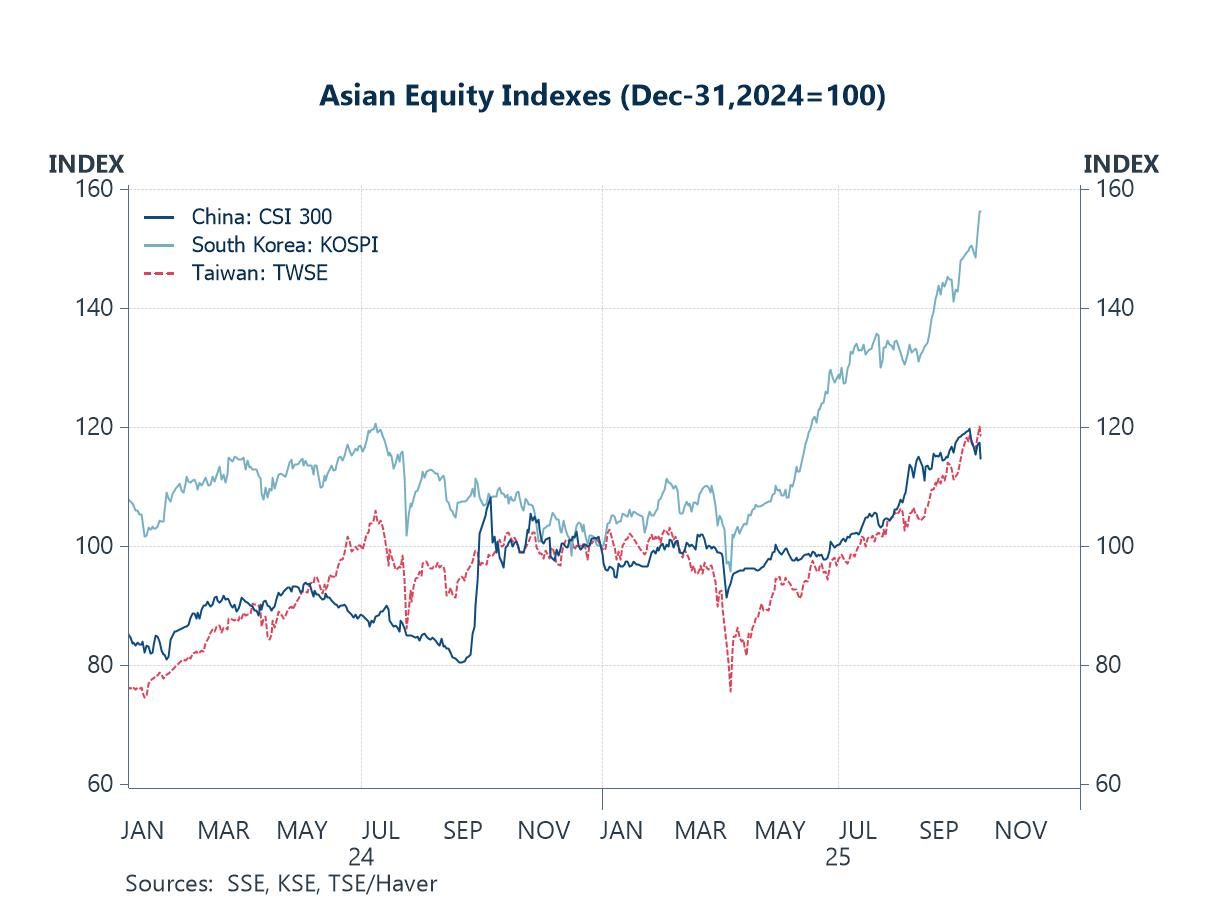

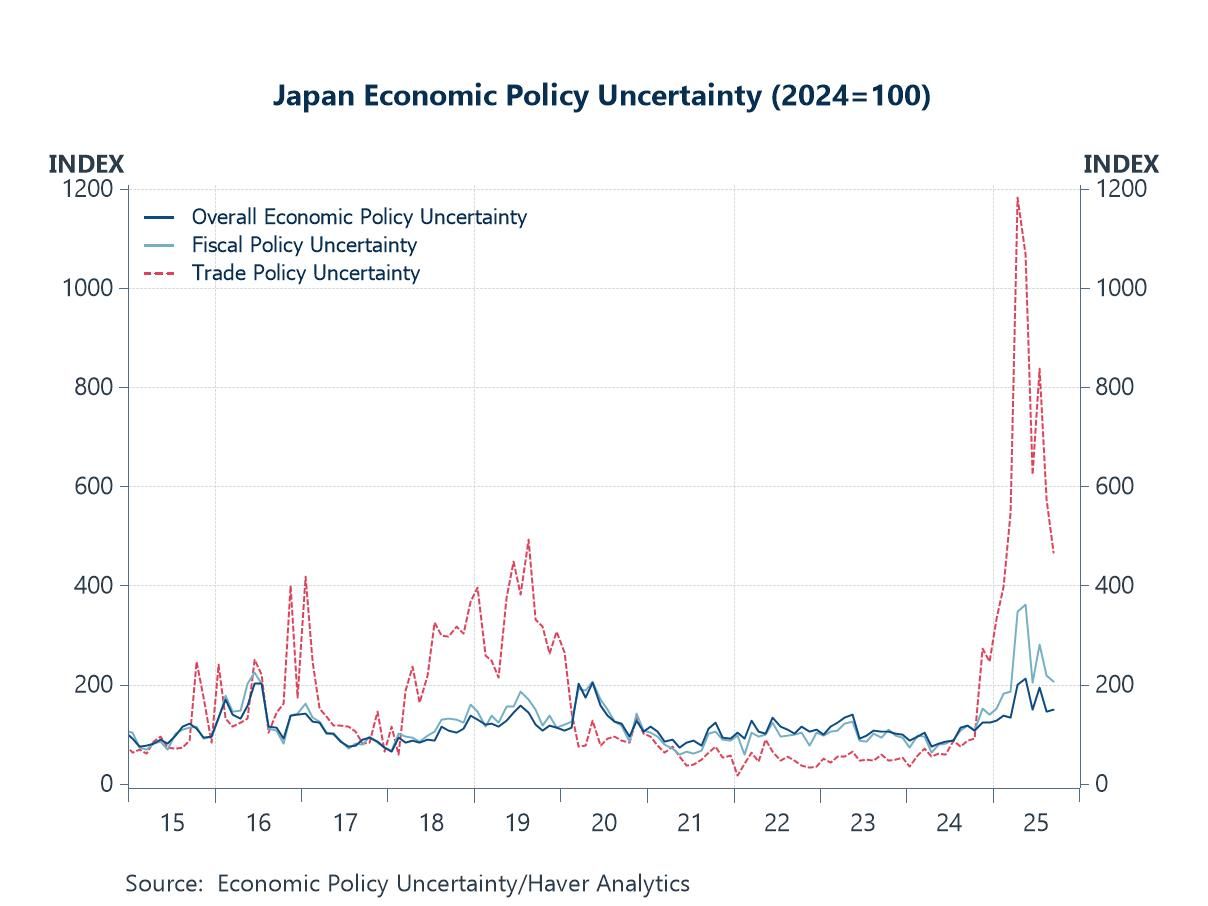

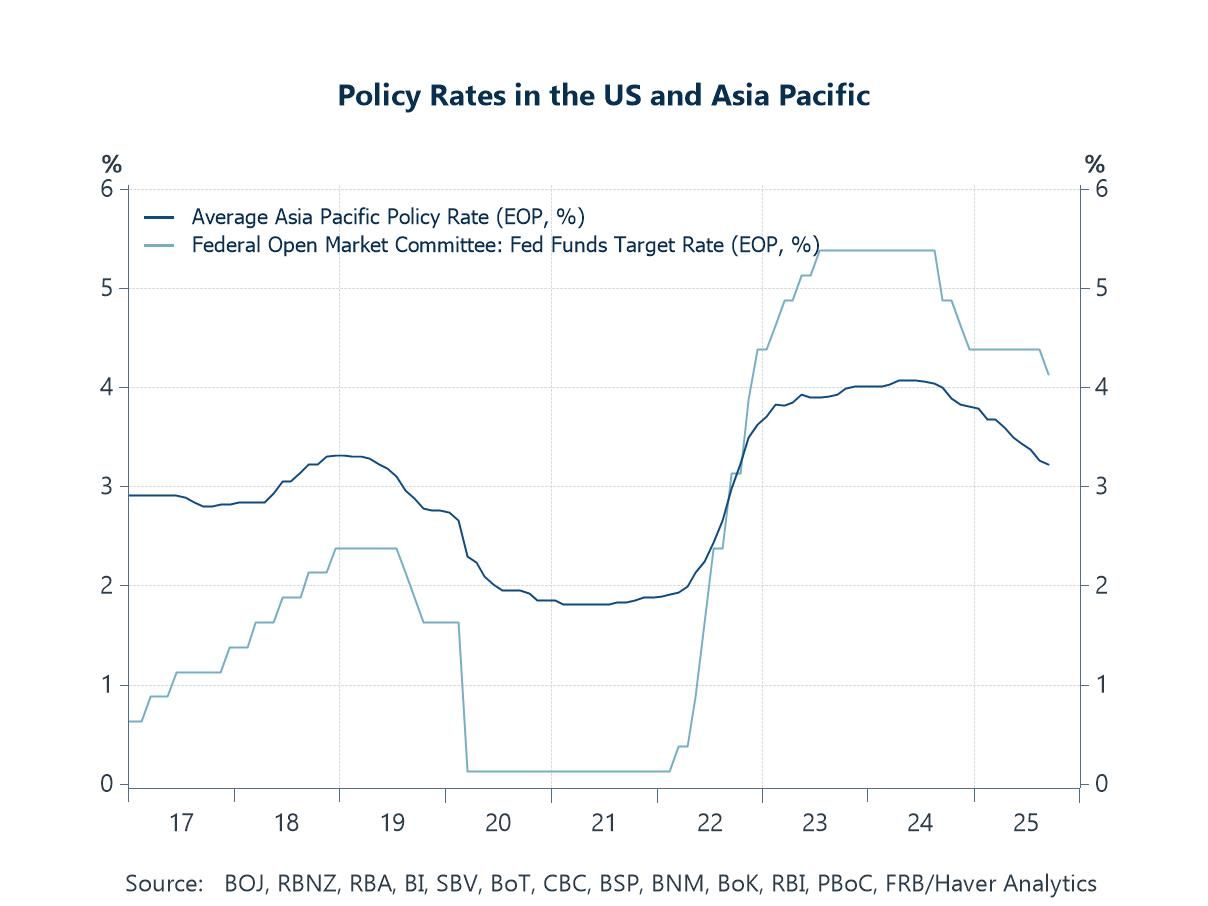

Elsewhere in the region, AI-related optimism continues to drive gains across several Asian equity markets (chart 4). In Japan, political uncertainty has eased slightly as LDP leader Takaichi’s path to becoming the next Prime Minister became clearer following the Japan Innovation Party’s decision to form a coalition with the LDP. That said, economic policy uncertainty remains elevated following the LDP’s recent string of weak election results (chart 5). Finally, attention turns to upcoming monetary policy decisions in South Korea and Indonesia, where further easing appears less certain given domestic considerations (chart 6).

China’s Q3 results China’s Q3 real GDP growth came in at 4.8% y/y, slightly above expectations, though the latest print extends the country’s recent trend of moderating economic momentum. While exports likely helped support growth during the quarter—thanks to China’s diversified export base despite plunging shipments to the US—other sectors continued to show signs of weakness. This uneven growth pattern was echoed in the accompanying September activity data: retail sales growth cooled further, even as industrial production accelerated (chart 1). Meanwhile, property prices extended their multi-year decline, though the pace of contraction continued to slow. Looking ahead, investors are watching to see how China’s recent “super golden week” holidays will feed into Q4 growth indicators. At the same time, renewed US-China tensions threaten to disrupt late-year momentum should new tariff or non-tariff measures take effect soon.

Chart 1: China exports, retail sales, and industrial production

A comforting point, however, is that given China’s relatively strong economic results in Q1 and Q2, aided again largely by exports, the Chinese economy can still achieve its 5% growth target this year even if its growth slows further. Specifically, China needs to manage y/y growth of at least about 4.6% (chart 2), which is lower than its 4.8% outturn in Q3 for the 5% target to be reached. Nonetheless, and given China’s softening growth backdrop in the face of external headwinds, investors are also looking to China’s fourth plenum taking place this week, for any policy cues and more broadly, any changes to the government’s five-year strategy for the Chinese economy. Of particular interest too concerns any decisions by the Chinese government that pivot the Chinese economy towards a more consumption-driven one, as opposed to the existing export and investment-led model.

Chart 2: China y/y real GDP growth

US-China trade relationship China’s latest economic data has not, however, overshadowed the recent flurry of exchanges between the US and China. To some, these developments reflect a resurfacing of tensions; to others, they may represent an effort to build bargaining chips ahead of a possible extended US-China tariff pause or a more conclusive trade deal. The recent exchanges—covering issues such as China’s rare earth export controls, mutual imposition of port fees, and even a potential additional 100% tariff on US imports from China starting November 1—have certainly kept investors cautious. This is especially evident in Chinese equity markets. As shown in chart 3, post–Golden Week selloffs underscored this caution, although some of those losses have since been pared. Recent equity market support, meanwhile, has been underpinned by key sectors such as technology—boosted by AI optimism—as well as telecommunications and materials, while others, including utilities and energy, have lagged.

Chart 3: China equities and US trade policy uncertainty

Asia equity markets Persistent AI optimism and the broader upcycle are most evident in the strong performance of semiconductor-heavy equity markets such as Taiwan and South Korea. As shown in chart 4, both markets have recorded meteoric gains this year, with strong double-digit year-to-date increases. While such sustained rallies have raised concerns about a potential tech bubble, recent major earnings releases—many of which have exceeded expectations—have only reinforced market optimism. Notably, TSMC’s recently-announced and stronger-than-expected Q3 earnings added further momentum. South Korean equities have stood out in particular, with the KOSPI surging nearly 60% year-to-date, buoyed by substantial gains in major names such as Samsung Electronics and SK Hynix.

Chart 4: Asian equity indexes

Japan politics Meanwhile in Japan, political uncertainty persists as parliament prepares to select the next Prime Minister. What was initially seen as a near-certain path for the LDP’s Takaichi to become Japan’s first female leader has been complicated by the exit of the LDP’s long-standing coalition partner, Komeito, effectively collapsing the minority coalition government. The LDP’s interim vulnerability opened a window for opposition parties to form alliances ahead of the October 21st vote for Japan’s next Prime Minister. In practice, however, it is difficult for these parties to unite behind a single candidate. Since then, the LDP has managed to secure the Japan Innovation Party as a new coalition partner, though a coalition of just these two parties would still fall short of a majority. While the political landscape remains fluid, economic policy uncertainty has been elevated amid the LDP’s recent string of weak electoral results (chart 5), staying well above levels seen a year ago.

Chart 5: Japan’s economic policy uncertainty

Central bank decisions This week also brings central bank decisions in Asia, specifically from South Korea and Indonesia. Prospects for near-term US Fed rate cuts have eased external constraints on additional monetary easing—moves that many of Asia’s central banks have already pursued this year (chart 6). However, domestic factors remain important. In South Korea, rising house prices are seen as a barrier to further Bank of Korea easing in October. In Indonesia, domestic currency weakness, with the rupiah among the worst-performing Asian currencies year-to-date, may limit additional policy easing following the central bank’s surprise September rate cut. This, however, must be balanced against the need to support continued economic growth.

Chart 6: Asia average monetary policy rate

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief