Asia| Mar 23 2026

Asia| Mar 23 2026Economic Letter from Asia: A Crude Awakening

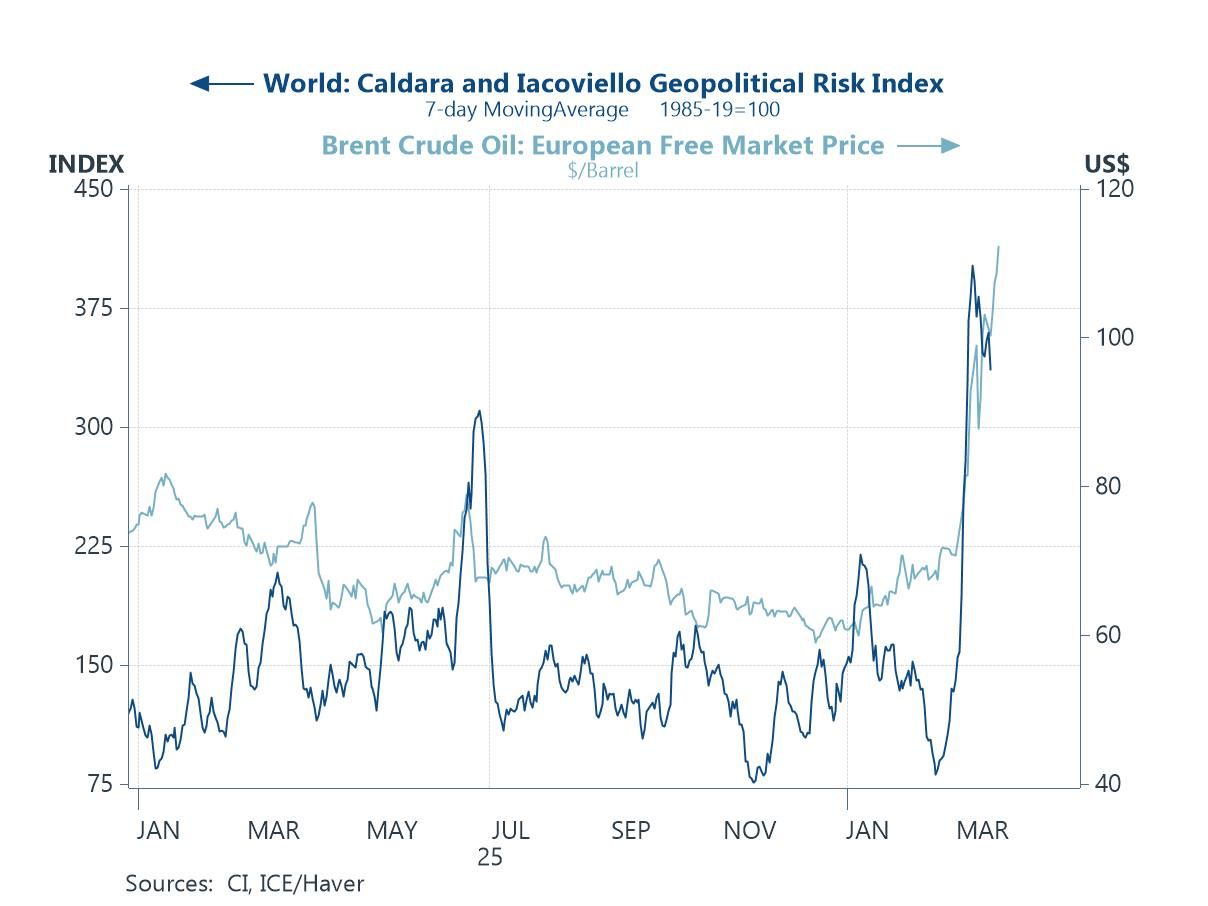

In this week’s Letter, we take stock of the ongoing Iran conflict, review key developments across Asia, and assess consumer sentiment in the region. The conflict continues to weigh on markets, with oil prices remaining elevated (chart 1). At the same time, global pressure is building against the continued disruption of flows through the Strait of Hormuz, though concrete actions to restore shipments remain uncertain.

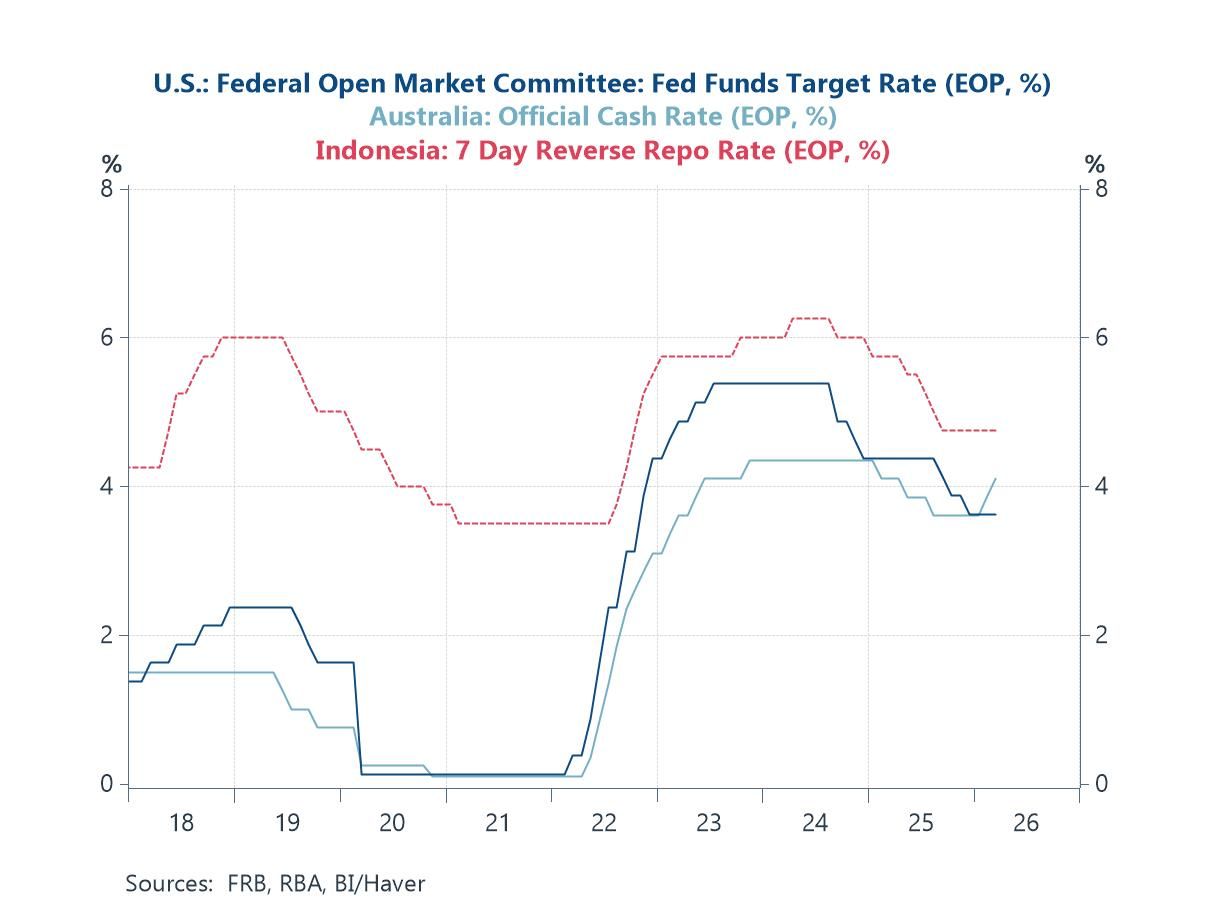

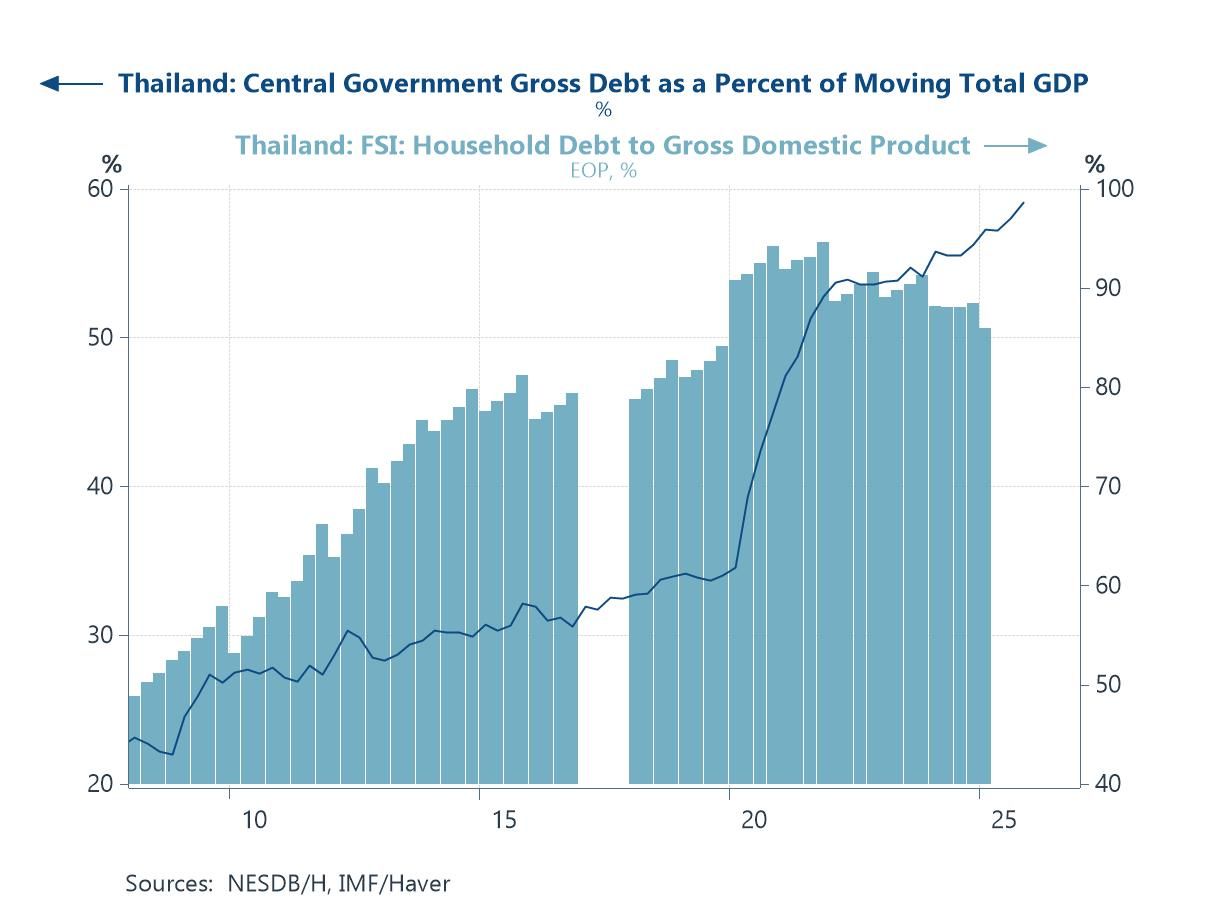

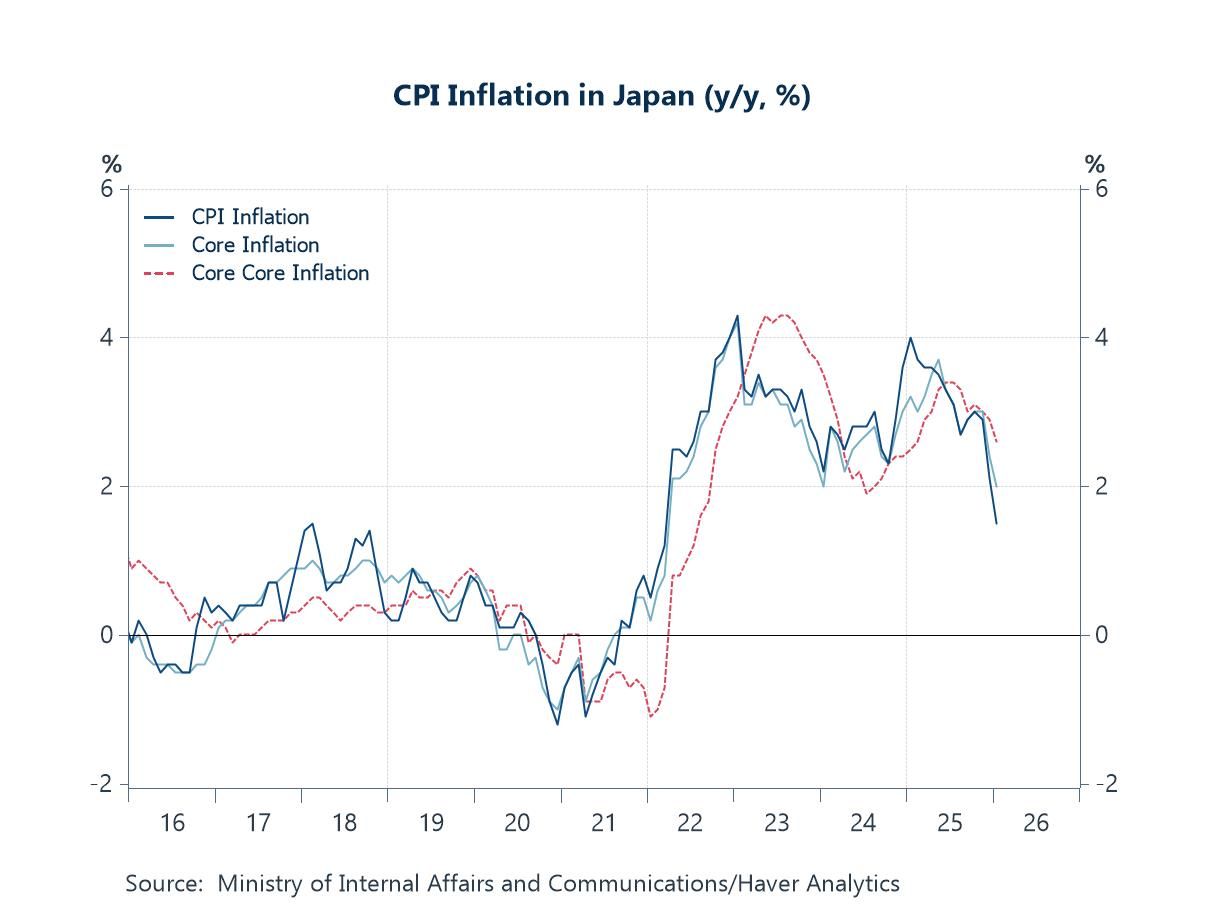

Amid this backdrop, several Asian central banks delivered policy decisions last week (chart 2), with the Middle East conflict explicitly cited as a key consideration. In effect, higher oil prices have either reinforced existing tightening biases or reduced the likelihood of rate cuts, reflecting mounting inflation concerns. On the domestic front, Thailand stood out, where Prime Minister Anutin’s decisive parliamentary re-election has eased lingering political uncertainty. Attention now shifts to how the new government will address longstanding challenges, particularly elevated debt levels (chart 3), alongside broader economic reforms. Looking ahead, the regional calendar remains active. Beyond flash PMI releases, focus will turn to Japan’s latest inflation print (chart 4) and China’s industrial profit data.

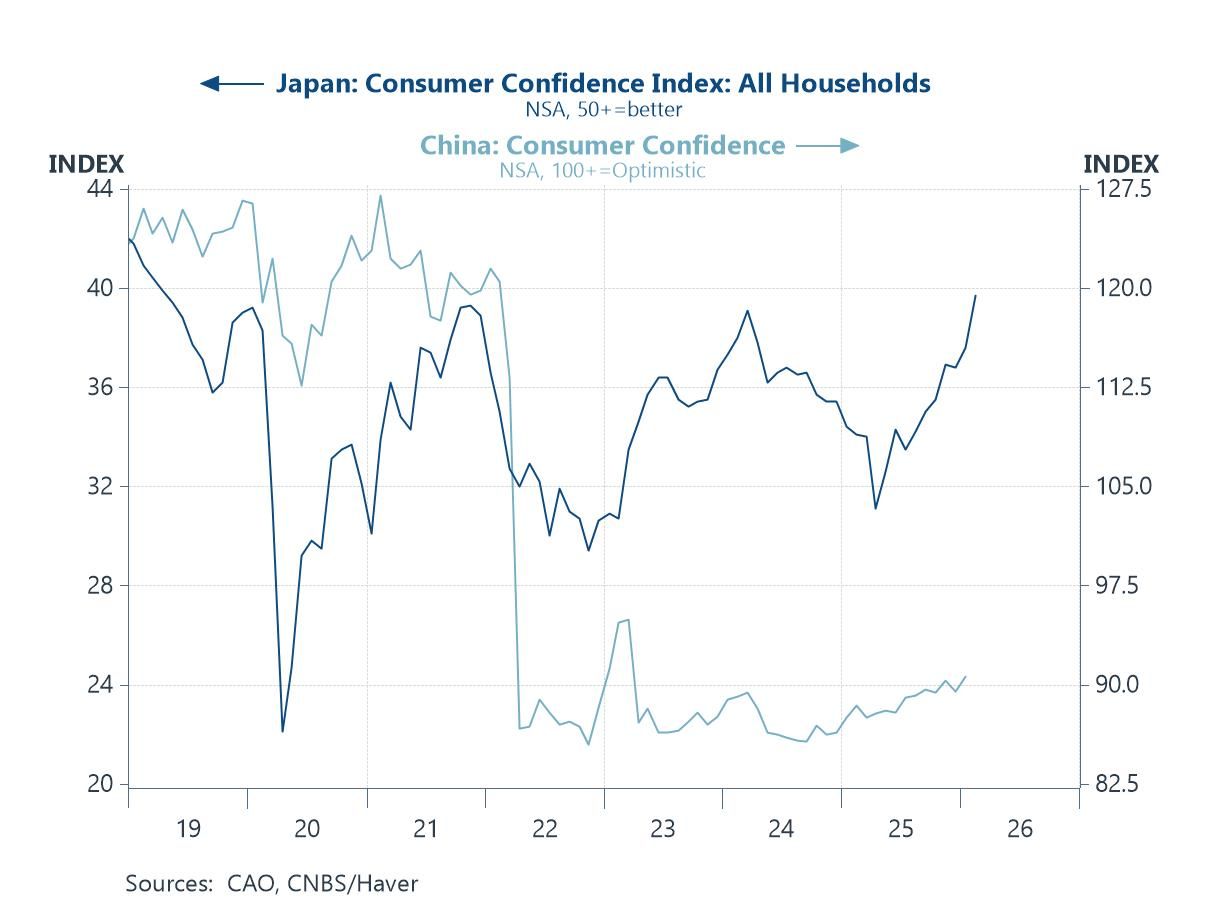

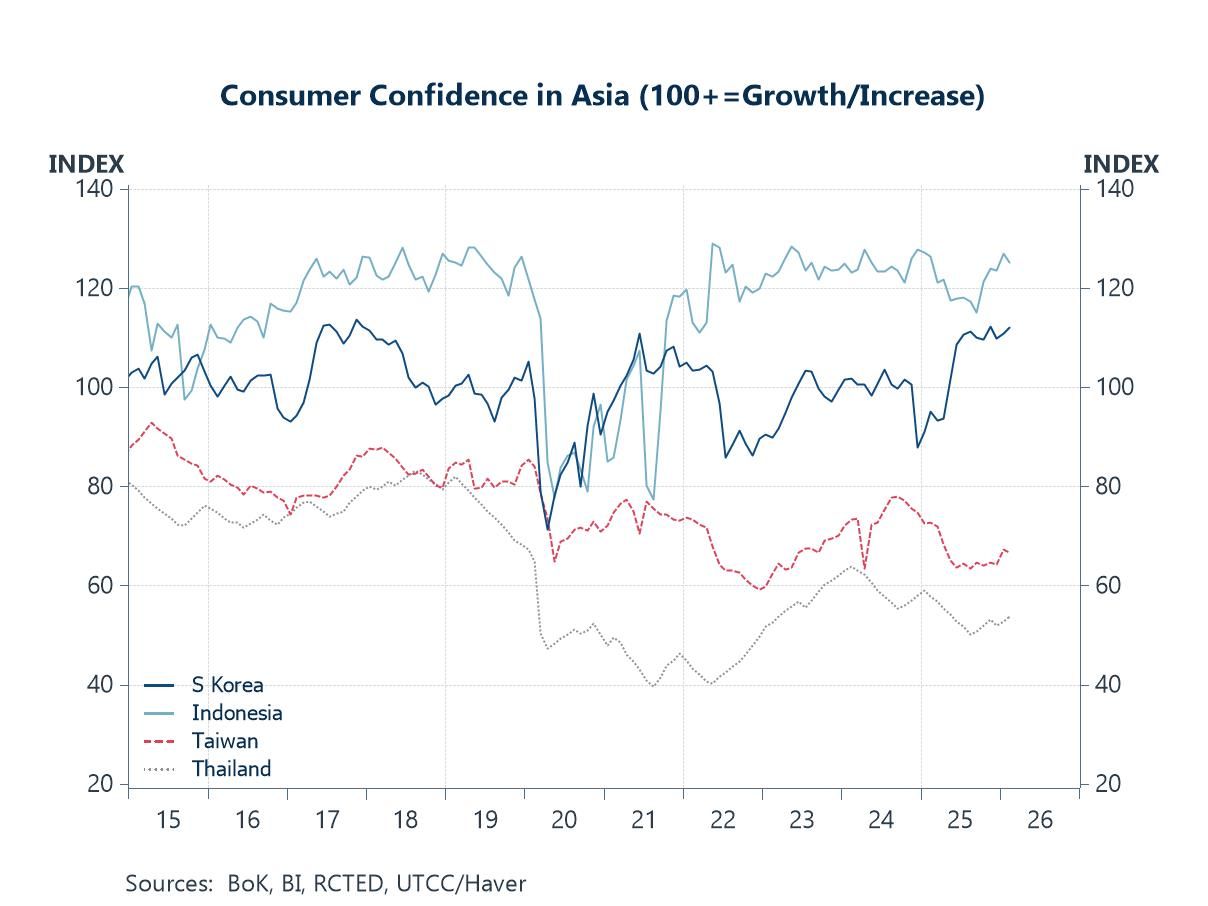

Turning to the Asian consumer, sentiment in China and Japan has improved in recent months (chart 5), supported in part by government policy and expectations of further consumer-focused measures. However, the Iran conflict poses downside risks, particularly through higher energy prices. Elsewhere in Asia, consumer confidence has stabilised (chart 6), though it remains exposed to similar risks, with the ongoing conflict threatening to weigh on sentiment across the region.

Iran conflict and energy prices The Iran conflict continues to rage, with shipping through the critical Strait of Hormuz still heavily constrained. This has kept a tight lid on crude supply, leaving oil prices significantly elevated (chart 1) relative to recent history. The resulting supply drag and price surge are adding upward pressure on inflation and, potentially, weighing on growth—particularly for oil-importing economies across Asia. That said, momentum is building on the diplomatic front. More than 20 countries have now backed a joint statement calling for safe navigation through the strait. Still, it remains unclear how this will translate into concrete actions, or—crucially from an economic perspective—how quickly it might restore disrupted oil flows.

Chart 1: Geopolitical risk and crude oil prices

Recent central bank decisions in Asia As discussed previously, persistently elevated oil prices are likely prompting Asian central banks to reassess their policy stance amid rising inflation risks. This shift was evident in three decisions last week as the Iran conflict continued. The Reserve Bank of Australia (RBA) delivered its second rate hike of the year, explicitly citing the Middle East conflict and warning that short-term inflation expectations have already edged higher (chart 2). Meanwhile, Bank Indonesia—previously expected to ease—held its policy rate steady, pointing to deteriorating global conditions linked to the conflict. In Taiwan, the central bank also kept rates unchanged, citing the Iran conflict and surging energy prices as upside risks to inflation. Taken together, the spillover effects of the Iran conflict are already showing up in policy decisions and are likely to become increasingly evident in upcoming economic data.

Chart 2: US, Australia, and Indonesia policy rates

Thailand’s re-elected Prime Minister Turning to Southeast Asia—specifically Thailand—Prime Minister Anutin last week secured a landmark re-election in parliament, winning the backing of 293 out of 499 members. With his party’s recent electoral victory and now firm parliamentary support, a period of relative political stability is in sight, allowing policymakers to refocus on pressing domestic challenges. Attention now turns to how Anutin will steer the economy beyond years of underperformance and tackle longstanding issues, including elevated government and household debt (chart 3), as well as how he navigates external risks stemming from the Middle East conflict—particularly via channels such as higher energy prices and inflation.

Chart 3: Thailand central government and household debt

The week ahead Looking to the week ahead, Asia faces a comparatively busier data calendar, with flash PMIs due alongside February releases for Japan’s CPI and China’s industrial profits. In Japan, CPI inflation has eased sharply in recent months (chart 4), with headline inflation dipping below the 2% threshold for the first time in years in January. However, the combination of recent yen weakness and the surge in oil prices could reintroduce inflationary pressures going forward. In China, attention will focus on whether industrial profit growth can build on the recent run of better-than-expected February data, adding further momentum to signs of a stabilising economic backdrop.

Chart 4: Japan consumer inflation

Asia and consumption Amid a fragile global backdrop shaped by the ongoing Iran conflict, the outlook for consumers in Asia remains cautious—particularly for younger cohorts without significant intergenerational wealth buffers. This is compounded by a challenging labour market, where the rise of AI capabilities is, in some cases, weighing on lower- to mid-level white-collar roles. That said, this caution is not yet fully reflected in aggregate consumer confidence readings for China and Japan (chart 5). One reason may be timing, as late-February to March data—when the Iran conflict intensified—are likely not yet captured. In addition, AI-related effects are still gradually feeding through these economies. In China, recent government measures to support consumption may provide a partial offset to these headwinds. In Japan, some of the drag may be mitigated by improving labour market conditions, alongside a degree of optimism surrounding the policies of new Prime Minister Takaichi.

Chart 5: China and Japan consumer confidence

Beyond the risks discussed above, similar pressures are evident across other Asian economies—albeit to varying degrees, depending on factors such as reliance on imported oil and the health of the labour market. As shown in chart 6, consumer confidence remains uneven across the region. While readings have broadly stabilised in recent months, they remain vulnerable to downside risks, particularly from price pressures linked to the ongoing Iran conflict. Among the economies highlighted, confidence remains relatively weak in Taiwan and Thailand, while South Korea and Indonesia appear more resilient, supported by their respective growth dynamics. Another key metric to watch—where available—is consumers’ price expectations. As awareness of the Iran conflict’s impact deepens, inflation expectations may begin to drift higher, posing additional risks to the regional outlook.

Chart 6: Consumer confidence in South Korea, Indonesia, Taiwan, and Thailand

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief