Canadian Retail Sales Drop and Growth Falters

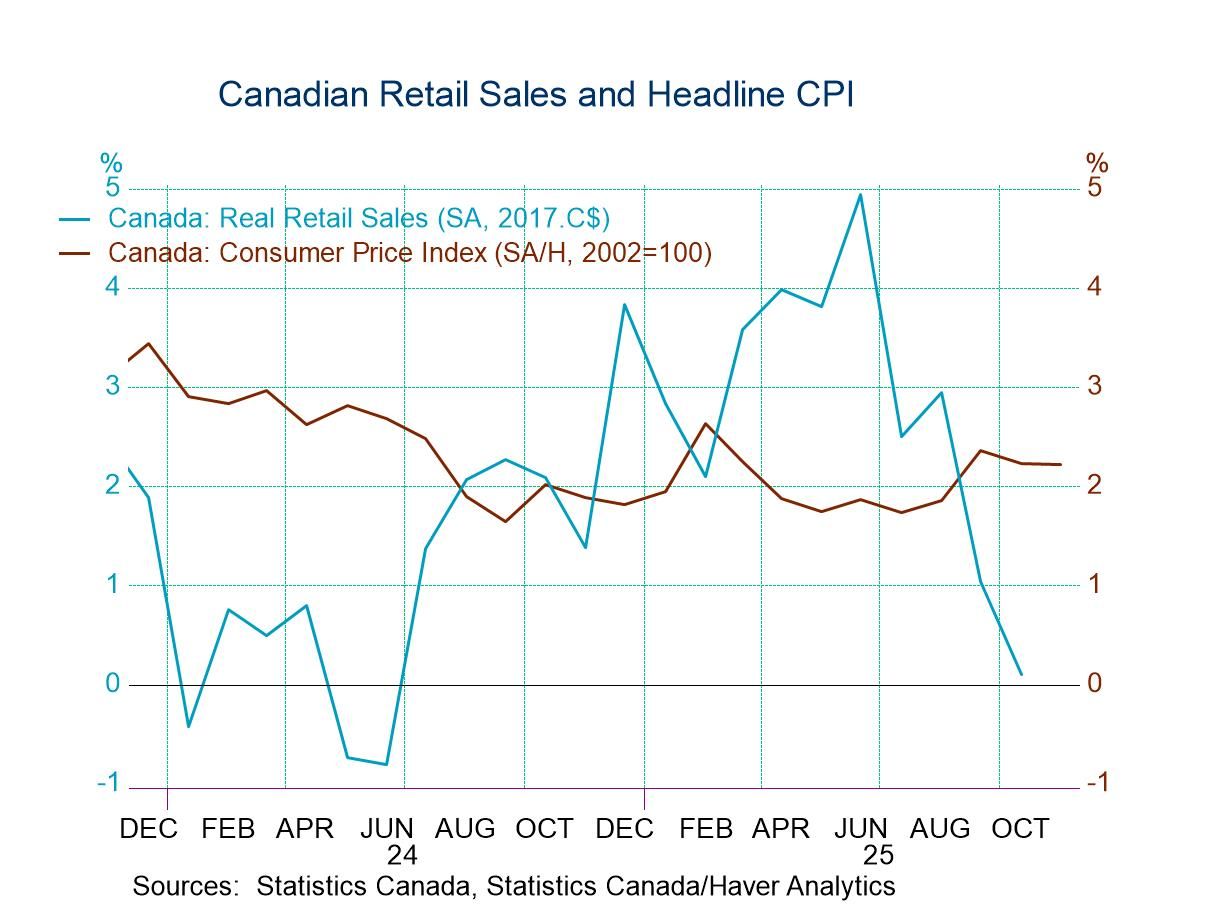

Canadian retail sales and other growth metrics appear to be weakening as the year draws to a close. Inflation has firmed up as well. Retail sales in October saw a month-to-month drop of 0.2% as supermarket sales fell 0.7%, month-to-month, clothing store sales fell 1.2%, and retail excluding motor vehicle sales fell by 0.6%. Overall real retail sales fell by 0.6% in October from September. This is the second consecutive month in which total nominal retail sales and retail sales in real terms both dropped month-to-month. Total retail sales and real retail sales both are declining over three months. Total retail sales at a -0.6% annual rate real retail sales-3.2% annual rate. Real retail sales are decelerating from a 2% growth rate over 12 months to a -1.7% annual rate over six months to a - 0.6% annual rate over three months. Real retail sales show more severe deceleration, growing by merely 0.1% over 12-months shrinking at a 3.8% annual rate over six-months and declining at a 3.2% annual rate over three-months.

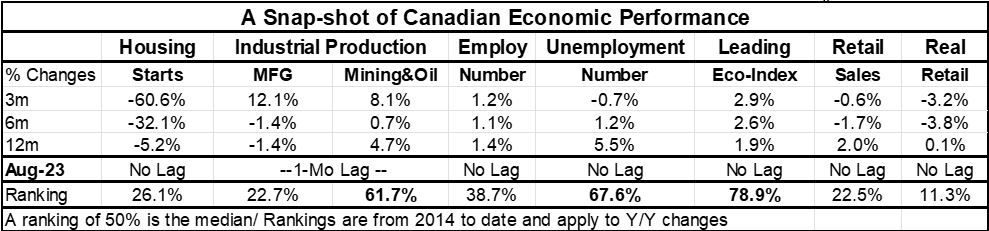

Other indicators weaken Over three months housing starts show a sharp contraction, falling at a 60.6% annual rate, a clear ongoing deceleration from a -5.2% drop over 12-months. However other metrics show slightly more upbeat results: employment, for example, yields job growth still at 1.2% at an annual rate over three-months although it slowed from a 1.4% year-over-year gain. The all-encompassing leading economic index shows an actual step up to a pace of 2.9% over 3 months from 2.6% over 6-months and 1.9% over 12-months. Manufacturing and mining output also show gains and a sharp acceleration from their year ago pace; for manufacturing output fell 1.4% year-over-year then rose at a 12.1% annual rate over the three-months ended in September; mining and oil production speeded up from a 4.7 percent 12-month gain to an 8.1% annual rate over three-months. The manufacturing and mining statistics lag by one-month. Another positive sign for the economy is unemployment as the number of unemployed declines at a 0.7% annual rate over three months even though it rises by 5.5% over 12 months.

Ranking metrics We can also vet these various sector results by looking at the growth rates year over year and comparing that pace to what has happened historically back to 2014. These individual category ranking statistics provide better relative comparisons across components. On that basis, the weak sector is retailing with real retail sales having 11.3 percentile standing and overall nominal retail sales having a 22.5 percentile standing. The next lowest year-over-year ranking is from manufacturing at a 22.7 percentile standing, that compares to a 26.1 percentile standing for housing starts. The performance of employment fares relatively better at a 38.7 percentile standing, but that's still below the 50% mark, putting job growth below its median for the period. The number unemployed, however, has a 67.6 percentile standing which is above its median and, of course, not a good result because here we would prefer to see leaner numbers on unemployment changes. The year-over-year growth rate for unemployment is solid, in the top one-third of all of the growth rates of the employed that we've seen since January of 2014. For unemployment, at least the sequential growth rates show that the process of unemployment creation is not accelerating. On the positive side the leading economic index has a 78.9 percentile standing which is quite strong and the mining and oil production have a 61.7 percentile standing which is above their median for the period.

Further context? And, when we consider the ranking of these growth rates, we can also look at the progression of growth in the table, such as the mention I made above for unemployment. For example, housing starts have a weak year-over-year standing but they have a much weaker growth rate over three months Compared to 12-months…on the other hand, manufacturing has a weak year-over-year standing but over three months manufacturing output has stepped up growth considerably. No one statistic can create a profile of these industries which live in the real world and have multiple dimensions and where the trends may be dynamic, in flux, and hard to singularly characterize.

Got inflation? As of October, Canadian inflation had picked up to some extent, inflation in Canada had dipped below the 2% mark from April through August of 2025. In September and October, the year-over-year growth of headline inflation was in the 2.3 to 2.2% region. The CPIx which didn't get quite that low, that recently got down to 1.5% and 1.6% in late 2024 and was as low as 2.2% and 2.5% from March to May of 2025 has moved up. September and October price growth rate is up to the 2.8 to 2.9% pace with the core rate running in the neighborhood of 2.6% toward the end of the year after reaching a low just below 2% in November of last year.

Nothing dramatic but a tilt to more of what Canada wants less of Oh no there's nothing dramatic going on in Canada, the economy appears to be weakening to some extent, the retail sales numbers show the largest deceleration. Of course, Canada and the US continue to have a spat over tariffs, and their two leaders still appear to be somewhat antagonistic about how that process is unfolding. Some Canadian stores have even taken the action of removing form the shelves some goods from the US, particularly US alcoholic products. The step up of inflation is something to watch and does not pair well with the weakening in economic activity.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global