Global| Jun 16 2026

Global| Jun 16 2026ZEW Shows Mixed Conditions and an Expectations Rebound

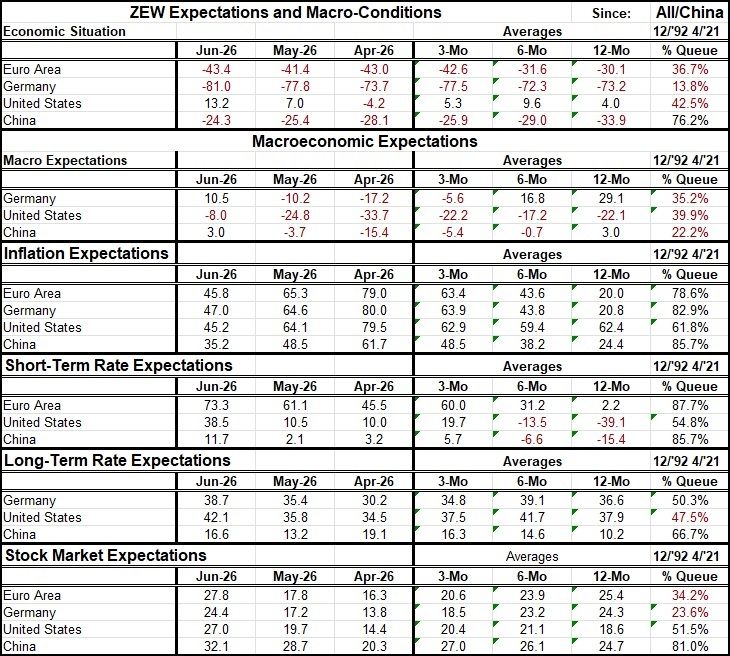

The ZEW diffusion survey (an up-minus-down survey) showed mixed improvements in the economic situation and improvements for macroeconomic expectations in June. The report shows the economic situation improving in the United States and China, with the euro area taking a small step back (to -43.4 in June from -41.4 in May), while Germany also saw a step back in the economic situation (to -81.0 from -77.8). The ranking metrics show the German reading as lower only 13.8% of the time—the weakest showing among the four. The EMU ranking is at a 36.7 percentile, with the U.S. ranking close to that at a 42.5 percentile. China has a 76.2 percentile ranking over a shorter timeline.

Macro expectations show solid improvements reported in Germany, the U.S., and China. Macroeconomic rankings all are muted, with the U.S. at a 39.9 percentile standing as the strongest, followed by Germany at a 35.2 percentile standing and China at a 22.2 percentile standing.

Inflation expectations are still high across the board, ranging from a low percentile standing for the EMU, Germany, and China—from a euro area low of 78.6 to a high standing for this group at 85.7 for China. In contrast, the U.S. ranking is still high, but only at its 61.8 percentile. And all the inflation expectations readings fell in June as optimism on opening the Strait of Hormuz has been growing.

Nonetheless, expectations for short-term rates have been rising. They rose solidly in the EMU and China, and strongly in the U.S., from 10.5 in May to 38.5 in June.

In contrast, long-term rate expectations rose across the board as well but by modest amounts. The rankings for short-term expectations are stronger for all three countries compared to the ranking on long-term rate expectations. I suppose we can understand that as expectations of anti-inflation medicine.

Stock markets are assessed as higher month-to-month in the EMU and in all three countries. China has a strong ranking for its stock market assessment at its 81st percentile. The U.S. standing is above its median at its 51.5 percentile; the euro area expectation is at its 34.2 percentile, with German stock market expectations still weak at its 23.6 percentile.

The pending conflict-ending deal in the Middle East should be a catalyst for further improvement. While the U.S.-Iran deal is not yet announced in detail—or even signed—market reactions are clear-cut across the board; there is no sign that this deal is expected to wither so soon. But it still has issues and contentious elements, such as Iran’s nuclear ambitions and the fact that the Israel is not on board with what it regards as a too-early exit from hostilities. Israel wants regime change and warns of a more difficult future without one.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief