Global| Feb 16 2016

Global| Feb 16 2016ZEW Weakens Further As Both Current Assessment and Outlook Dim

Summary

The ZEW index was in denial last month but the German IFO sector report showed some clear-cut weakness. This month the ZEW is giving way with a drop in the current index to 52.3 from 59.7 last month. Expectations have plunged all the [...]

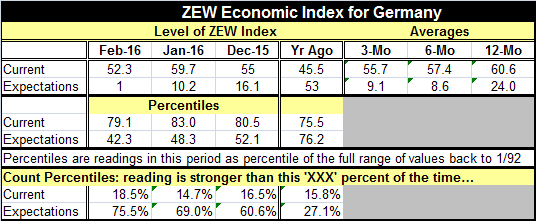

The ZEW index was in denial last month but the German IFO sector report showed some clear-cut weakness. This month the ZEW is giving way with a drop in the current index to 52.3 from 59.7 last month. Expectations have plunged all the way to 1 from January's 10.2 as they continue their descent.

The ZEW index was in denial last month but the German IFO sector report showed some clear-cut weakness. This month the ZEW is giving way with a drop in the current index to 52.3 from 59.7 last month. Expectations have plunged all the way to 1 from January's 10.2 as they continue their descent.

To understand the context of these values, we calculate their percentile tendencies. The current index is stronger only 18.5% of the time, so it still has a relatively firm standing; it is higher only one-in-five-times, roughly. But expectations are more substantially weak. They are higher 75.5% of the time or lower roughly only one time in four.

The chart above shows that the expectations gauge has moved sharply lower in recent months while the current index has been undergoing very gradual erosion from a relatively high level.

Ahead of the last German recession, the ZEW current index was falling fast ahead of the recession's onset while expectations were also collapsing and in the neighborhood of a -50 reading as recession set in. The ZEW readings now show nothing of that sort. What we see is some lost momentum in the economy and some significant concerns about the pace of future growth. But there is not even a glint of concerns over a coming contraction. Month-to-month expectations have fallen harder than this less 18% of the time. That is a relatively severe one-month change in view.

Looking at ZEW members' stock sector assessments, there is still exceptional confidence in the expected performance of the consumption and construction sectors. The influx of migrants has given the construction sector a jolt of stimulus in Germany. Still, overall profit expectations for all stock sectors have been weaker historically only one about one-third of the time. Banking, insurance and utilities all have extremely low expectations set. The financial sector is pressured by growth concerns; utilities have an ongoing issue with German denuclearization.

The ZEW index is a poll of financial experts and their collective view on the economy and its performance. Last month's weakness in the IFO survey, an industry survey of actual sector-based firms, showed deterioration was afoot while the ZEW poll was more equivocal. The ZEW and the IFO now seem to be much more on the same page. Clearly, Germans have concerns related to the migrants and how Germany will deal with them based on the ongoing disruptions that have been reported. There is a question of how large the influx will eventually become. There are also raw economic issues and some structural questions about the EU as Europe continues to be weak. The EU is trying to offer up a package to keep the U.K. in as an EU member. The U.K. thinks its financial burden has been too great and is looking to pare that back.

The main report out of Europe today did show that vehicle registrations were up again in January for the 29th consecutive month. Despite industry problems, new car registrations have continued to advance and to underpin consumer spending in Europe much as they have in the U.S. as well. But Europe is still not out of the woods and everyone is waiting to see what steps the ECB takes in March. The Bundesbank has recently taken a good look at the future and has cut its already low view of inflation for the year ahead based on lower oil prices.

While oil rumors swirl, it should be clear that getting a deal among OPEC members and other large producers is going to be harder than herding cats. And it will remain just as hard to keep a deal in line if one is forged since the OPEC has always been about cheating on agreed production quotas. I see the risks of sharply higher sustained oil prices as a glimmering hope in the eye of dreaming producers, not as a reality. Look with skepticism upon rumors of a credible oil deal.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief