Global| Sep 19 2017

Global| Sep 19 2017ZEW Survey for September - Kick the Can

Summary

The ZEW survey of macroeconomic conditions shows little change between August and September. Four regions are slightly weaker and three are slightly stronger. However, the queue standings of the readings are uniformly firm to high [...]

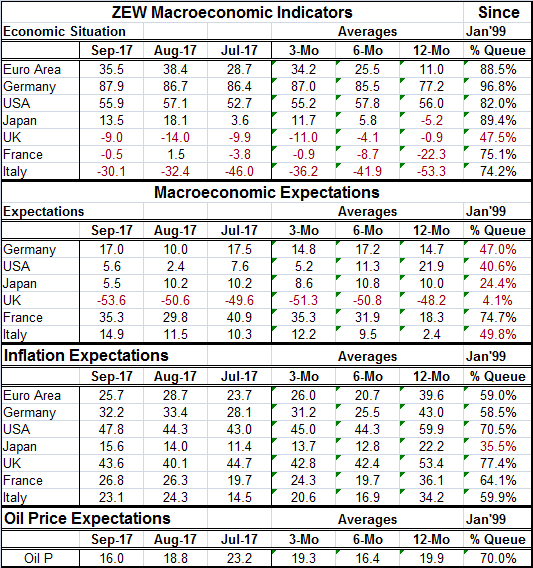

The ZEW survey of macroeconomic conditions shows little change between August and September. Four regions are slightly weaker and three are slightly stronger. However, the queue standings of the readings are uniformly firm to high with Japan, the United States, Germany and the EMU with readings at the 82nd percentile or better and France and Italy with readings in the mid-70th percentile. The United Kingdom has the lone reading below the 50th percentile of its historic queue because of its Brexit gambit. Oddly, France and Italy each have outright negative readings that nonetheless have mid-70th percentile standings.

The ZEW survey of macroeconomic conditions shows little change between August and September. Four regions are slightly weaker and three are slightly stronger. However, the queue standings of the readings are uniformly firm to high with Japan, the United States, Germany and the EMU with readings at the 82nd percentile or better and France and Italy with readings in the mid-70th percentile. The United Kingdom has the lone reading below the 50th percentile of its historic queue because of its Brexit gambit. Oddly, France and Italy each have outright negative readings that nonetheless have mid-70th percentile standings.

Conversely, expectations in September are more likely to have been marked up than down. Four regions see improvement in September; only two see weaker conditions. Not surprisingly, it is a case of the weak getting weaker as the U.K. and Japan have the weakest expectations in September plus worsened outlooks. The U.K. has a 4.1 percentile queue standing for expectations, rarely lower and Japan's expectations are at their 24.4 percentile. Despite the tendency for the outlook to improve, ALL queue standings for September are below their respective historic medians except France. The jump in German expectations in September brings it closest to its median (50) with a 47th percentile standing. The upshot is that expectations are on the rise but are lackluster.

With strong but little change macroeconomic conditions and generally below par macroeconomic expectations, inflation expectations are rising in all areas except two (the EMU and Germany). That is interesting since inflation in the EMU is below its target and the ECB needs to see progress toward inflation in order to raise rates. Germany and others have been pressing the ECB to begin to unwind some of its stimulus programs, but inflation is not pulling the trigger for rate hikes and not expected to do it soon either according to the ZEW experts. The U.K. and the U.S. have the highest inflation expectation queue standings. The U.K. is no surprise since the BOE post-Brexit vote response was to cut rates sharply, an action that weakened the pound and has brought a considerable lingering inflation impulse to the U.K. In the U.S., inflation is still below the Fed's objectives and not rising very fast with inflation expectations in the University of Michigan survey at extremely weak levels, in contrast to the ZEW expectations. Japan is the only country with inflation expectations actually below its (ZEW members') historic median and yet creeping up very slowly.

Oil price expectations are slightly weaker on balance in September even though a Saudi push to further restrict oil output and exports has been getting some traction and spot oil prices have been rising.

On balance, the ZEW experts appear to be locked into a view. Current data readings are still firm so current assessments on the macro-economy are not much changed. Expectations for the economy ahead are slightly elevated as PMI surveys have been somewhat upbeat, but there is still nothing there we could call optimism. And ZEW experts, somewhat cynically, see inflation in the U.K., the U.S., Italy and France, but not in the places where it is most needed: Japan or Germany or the EMU generally. Not surprisingly, with such a view, short-term rates in the EMU are seen softer, but U.S. rates are seen a bit firmer. That also simply rolls the trends forward. Globally, bond yields are seen mostly firmer, but not by much. I would say that the ZEW experts appear to be caught in the grip of Keynes: Not seeing that much growth, but seeing a current 'strong level of activity,' they see some improvement and are not expecting low inflation to last, yet not willing to forecast an inflation pickup. As a result, they compromise on the outlook by projecting higher bond yields - a sort of magical market tightening. The ZEW experts see 'no end in sight' to the current conditions with weak growth. Inflation in Japan is underperforming as is inflation in the EMU. Although since ZEW experts do see somewhat of an improvement in growth in the EMU/Germany, there may be an end game hiding there somewhere. But by and large, the view from the ZEW experts is that we are just kicking the same old can down the same old road. The ZEW experts are unwilling to project any kind of a breakout.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief