Global| Jun 13 2017

Global| Jun 13 2017ZEW Survey for June Show Stronger Germany, EMU, Japan and France; Outlook Is Less Buoyant

Summary

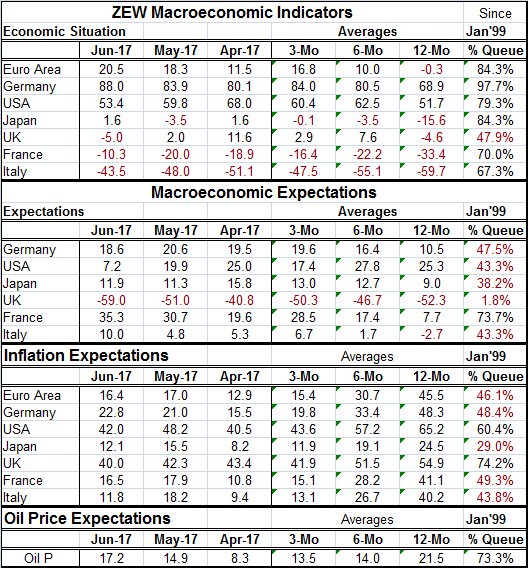

The way things are... The ZEW survey shows that the current rated economic situations in June improved everywhere except in the U.S. and the U.K. The absolute readings still show negative readings for Italy and France despite their [...]

The way things are...

The way things are...

The ZEW survey shows that the current rated economic situations in June improved everywhere except in the U.S. and the U.K. The absolute readings still show negative readings for Italy and France despite their improvement. The U.K. is alone is seeing a weakening that drags the net score into a negative value this month. Both Germany and the euro area overall show sequential improvement in their readings from 12-month to six-month to three-month. Japan, France and Italy show the same improving trend as the net negative rating gets sequentially smaller (in absolute value). The U.S. shows improvement over six months compared to 12 months then deterioration.

However, the rank scores of performance are quite different. On that ground, Germany is the strongest followed by the EMU then Japan, then the U.S.; France, Italy and the U.K. round out the rankings in descending order. The U.K. economy is struggling in this post-Brexit vote environment and ahead of the upcoming Brexit negotiations.

Expectations

Expectation readings are several orders of magnitude weaker than the current readings if we evaluate them by their queue standing values. On that basis, France, a chronic underperformer, has very high expectations (73.7 percentile) and a new government to boot. Germany is in second position with a below median reading at its 47.5 percentile followed closely by the U.S. and Italy, each with 43.3 percentile standings. Next comes Japan and finally the U.K., the latter with a standing that has been lower less than 2% of the time. U.K. expectations have been steadily chopped-down over the past several months and it just concluded an election that has destabilized the sitting government. Brexit negotiations are about to start and the U.K. appears to be in an economic and political mess. Since April, the evaluation of the U.S. economy has deteriorate the most and France has improved the most. Still, in the U.S. the central bank has one of its key meetings this week and still is expected to continue hiking rates. The weakness in the ZEW expectations survey might raise an eyebrow on that move or maybe not because the Zew inflation expectations....

Inflation expectations

Inflation expectations are a curious thing. While the various inflation expectation surveys in the U.S. remain very low with a new lower reading from a recent Federal Reserve Bank of NY index, the ZEW experts have the U.S. as one of two countries with inflation expectations above their median. The U.S. reading is in its 60.4 percentile compared to the UK where it reads even higher in its 74.2 percentile and may worsen there given the recent weaker performance of the pound sterling on foreign exchange markets in the wake of the recent U.K. elections. Inflation forces are near balance (or near their median anyway) in Germany and in the euro area with readings that are just shy of their historic medians in both cases. The medians for all queue rankings occur at the respective 50th percentile standing mark. Japan, still struggling to raise inflation, has the lowest queue standing for inflation at its 29th percentile although the raw score has it higher in June than it was in April (although lower than it was in May). France and Italy join their fellow EMU members with expectations for inflation below their respective medians. Still, there seems to be a renewed push for higher interest rates from Germany where the finance minister today registered hope that the ECB would be raising rates soon. While the ZEW metrics do not speak to the issue of inflation in terms directly translatable into the ECB's mandate, since the ECB has hit its inflation target on average or been below it, a below median reading for inflation expectations should translate into a still quiescent and under target expectation for inflation in the EMU.

Oil

Oil prices, judging from the raw score for inflation expectations, have been stepping up their role steadily from April to May to June. At its June level, oil has a 73rd percentile standing. Oil recently has been underperforming and languishing below $50/barrel. But today the Saudis announced a plan to make output cuts and that sent prices higher in daily trading. As always, the future for oil is a big black hole.

Summing up ZEW findings

On balance, this comprehensive survey from the ZEW financial experts paints a picture of a nicely growing global economy, but one in which the U.K, is starting to stall with both growth and inflation becoming issues. Japan still is not seen as reaching its inflation targets in this survey although Japan's growth and expected growth metrics are in line with everyone else's. The ZEW experts have cut their expectations for U.S. growth but still see some lingering inflation issues for the U.S. Moreover, the ZEW view does not back the recent German call for the ECB to start hiking rates.

Implications

Since France is an unlikely engine of growth for the global economy and since it shows the best pick up, one thing we might be wary of is the prospect for central banks to overdo their tightening. Between expected rate hikes and balance sheet adjustment central banks acting in isolation but still doing many of the same things at the same time, could wind up squeezing a fragile recovery much more than they think. Economic circumstances remain fragile and because central bankers' reactions will be conducted on such similar timelines, policy risk will be magnified but probably not in focus anywhere. Central bankers all seem to have the same fear and the question is this: is it the wrong one? Bankers are afraid that inflation is rising and that they have left rates too low for too long. But global supply is still in excess. Globally labor is in excess. Debt levels are high and new debt cycle is unlikely to emerge to drive prices higher. Between the forces of global competition and technology, the prospects for much stronger wage gains and income growth remain dim. The real risk might be overdoing the tightening by acting too soon and because bankers fail to take into account what their fellow central bankers are doing. Beware! Do not feed the central bankers.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief