Global| Jul 14 2020

Global| Jul 14 2020ZEW Macro Expectations Bend Lower After Rebound

Summary

The three exhibits serve to summarize the thinking, assessments, and history of the ZEW financial experts on the global situation. These exhibits, beginning with the graph, show an extended period of weakening expectations, [...]

The three exhibits serve to summarize the thinking, assessments, and history of the ZEW financial experts on the global situation. These exhibits, beginning with the graph, show an extended period of weakening expectations, culminating in a sharp drop then a strong rebound in ZEW expectations that has transitioned into a bend lower without follow-through this month.

The three exhibits serve to summarize the thinking, assessments, and history of the ZEW financial experts on the global situation. These exhibits, beginning with the graph, show an extended period of weakening expectations, culminating in a sharp drop then a strong rebound in ZEW expectations that has transitioned into a bend lower without follow-through this month.

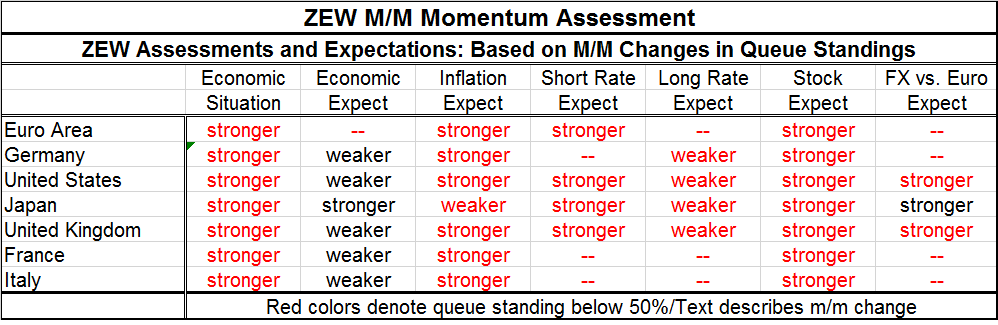

The table without numbers shows general tendencies: the economic situation improved across countries with readings that remain below their respective medians. And while there was 'broad' weakening in expectations month-to-month, the readings uniformly stay above their respective medians. Inflation expectations broadly rose but remain below their respective medians. Interest rate expectations were mixed with short-term rate expectations higher and long-term expectations lower but with levels of expectations below their median for both rate terms. Stocks are expected broadly stronger, but they still languish below their respective median values. That is a lot of agreement across some key variables and a good spread of countries.

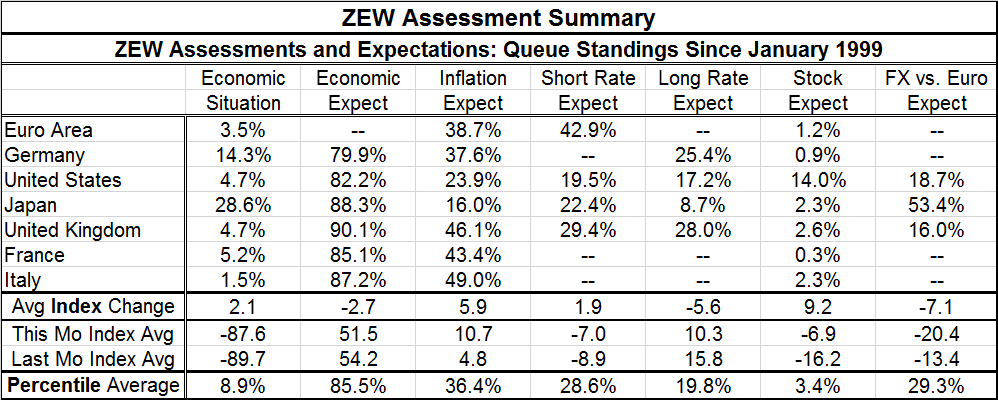

However, the table with the actual numerical assessments reminds us how strange some of these assessments are. The current economic situation is not just below its median; it is extremely weak with all standings in the lower one-third of their historic queue of values and most in their lower 6 percentile. Economic expectations are indeed above their respective medians and are, in fact, mostly in their eightieth percentiles or higher. To the ZEW experts, the situation is as dour as expectations are buoyant. Inflation carries an assessment that look more normal. Still, broadly that outlook is below its medians (50th percentile for each country or region marks the median value) but still quite moderate. As noted above, there are different changes afoot for short vs. long rates, but both sets of rate expectations are below their respective medians and generally by quite a lot, except for the euro area where short rate expectations are still well below their median but generally higher than in other surveyed countries. Stock market expectations did firm month-to-month, but the readings remain extremely weak with the lowest percentile average among measures in this table.

The ZEW survey is always an interesting set of data to observe since the ZEW experts tell you what well-informed German financial experts think. Their view this month shows some strengthening in Japan's macroeconomic expectations even though the BOJ just cut its assessments for all nine Japanese regions. ZEW experts did cut the assessment on the current situation in Japan this month.

Of course, I have managed to describe data changes and levels of assessments so far without saying the word 'virus.' That has just ended. Obviously, the progress and expected progress of the virus haunts and helps to determine these numbers. There is now serious global backtracking after an extended period of progress. The fact is that you can hide but you cannot run, to 'flip' an old expression. The virus is there. People can shelter from it and reduce infections for a time. But when an economy is re-opened, the virus is still out there. It circulates again and expands its reach. Simply put no country has any model to deal with it. Sweden alone is trying to live with it. Other countries have used lockdowns and now are using selective restrictions to calm the most recent outbreaks. It is quite unclear how successful this will be. For my taste, the ZEW outlook expectations are simply too high. Conditions are likely to continue to improve, but how fast and by how much are still big question marks. And there can still be backtracking. Countries will tell you they still have actions they can take, but in fact there is not much more that can be done. The virus spreads easily. It is lethal to people with health problems and most do not understand that it is rarely lethal to healthy people. But that does not mean that young healthy people are not at risk; some do suffer lung damage; the really unlucky ones die. No one is 'immune' but the probabilities shift sharply according to one's healthiness. What Covid-19 does and where there risks lie from it are actually not very well described to the public. Public health officials prefer the binary view that either it is safe to go out or you should stay at more. More places are recommending wearing masks.

What is most worrisome about all this is that there is still no agreement on an approach to living with the virus other than these economy-on/economy-off switches that are in any event devastating to businesses especially to small businesses. There is also the very unscientific plan to wait for a vaccine to be invented (…if ever). I can only conclude that the outlook should be more guarded and construed as being murkier than what ZEW experts seem to think.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief