Global| Feb 20 2018

Global| Feb 20 2018ZEW Growth Assessments Begin to Stabilize

Summary

The German ZEW economic expectations index fell to 17.8 in February from 20.4 in January. The current index fell to 92.3 from January's 95.2. The current index is this high or higher only 0.9% of the time. The expectations index is [...]

The German ZEW economic expectations index fell to 17.8 in February from 20.4 in January. The current index fell to 92.3 from January's 95.2. The current index is this high or higher only 0.9% of the time. The expectations index is this high or higher 51.5% of the time. The ZEW experts make assessments of a group of countries and regions each month.

The German ZEW economic expectations index fell to 17.8 in February from 20.4 in January. The current index fell to 92.3 from January's 95.2. The current index is this high or higher only 0.9% of the time. The expectations index is this high or higher 51.5% of the time. The ZEW experts make assessments of a group of countries and regions each month.

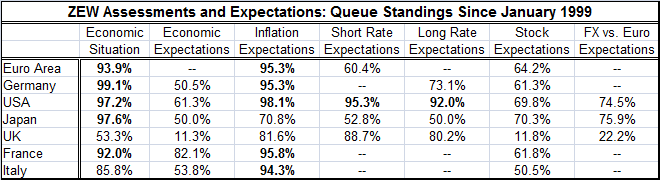

The ZEW assessments for each area or country and for each metric in the table are presented as queue standings in their respective time series back to 1999. The belief in Keynesianism emerges immediately from the table as you note that the consistently highest rankings are for the economic situation and for inflation expectations. Even though economic expectations are not elevated and, as a rule, are closer to their respective historic medians, where the economic situation is highly assessed inflation is also highly assessed. Japan is an exception. And oddly the United Kingdom, which actually has inflation, has more moderate expectations than its peers in the table as its economic situation has the weakest assessment of all as the U.K. prepares for its euro area exit.

In this environment, stock market assessments are mediocre with Japan's 70.3 percentile standing being the best of the lot and the U.K.'s 11.8 percentile standing being the weakest.

The dollar and yen are seen as moderately strong against the euro exchange rate while the pound is at a weak 22.2 percentile standing.

Long-term interest rate expectations line up more or less with inflation expectations.

Over the past year, there have been substantial upgrades to the economic conditions in France, Italy, the euro area, and Japan. Germany and the U.S. also have showed improvement but on smaller scale. Only the U.K. has worsened although the U.K. and Italy both continue to bear negative assessments

Expectations have seen the most improvement over the last 12 months in the two EMU countries that have been the weakest on average over the last 12 months, Italy and France. Even so, France has improved by twice as much as Italy and Italy has improved by more than twice as much as any other countries in the table. Over 12-month expectations have deteriorated for the U.K. and for the U.S. as of February. In this respect, the ZEW expectations differ markedly with those of U.S.-based analysts. Expectations for U.S. growth have been pushed up over the past few months by U.S. analysts in particular as GDP has consistently emerged as better and as a fiscal stimulus plan has been adopted. Europeans may simply be more skeptical about the impact of these programs on U.S. economic outcomes.

Changes in inflation expectations are most closely associated with changes in macroeconomic conditions. ZEW experts link their inflation expectations much more closely to changes in macro conditions than to actual macro conditions or to macroeconomic expectations or to changes in macroeconomic expectations. The ZEW experts are impressed with the change the economy has made over the past year more than any other single variable that affects their inflation outlook. However, stock valuations are dominated by changes in the expected macroeconomic situation.

The forward-looking nature of assessments on stocks coupled with a backward-looking assessment of inflation trends is an unusual mix. Moreover, the different European take on U.S. growth prospects will be something to watch. If U.S. growth does show a response to Trump-o-nomics, there should be some surprise content for Europe at least and that could lead to unexpected stock buying in the U.S. and dollar buying to facilitate that.

The outlook for 2018 is still unfolding and economic agents still seem to be trying to sort out what they think. The three-month changes in the assessment of current conditions, however, have stabilized over the past few months as have macroeconomic expectations. So not we are waiting to see if inflation develops and what central banks will do. Those are the next big events forecasters will be reacting to. In some sense, they have made their choices, put their chips on the table and now are waiting to see the outcome.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief