Global| Dec 12 2017

Global| Dec 12 2017ZEW Experts See Gradual Improvements and Rising Inflation Risks

Summary

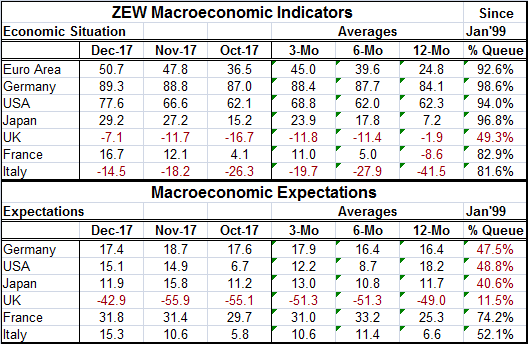

The chart is a reasonably good overview of what ZEW economic experts think. For a time, U.S. economic expectations outstripped everyone else - but no more. Over the last few months, in fact, there has been a very slow upgrading in the [...]

The chart is a reasonably good overview of what ZEW economic experts think. For a time, U.S. economic expectations outstripped everyone else - but no more. Over the last few months, in fact, there has been a very slow upgrading in the current economic assessment across the board and some improvements made to the outlook as the U.S. has sunk into the pack.

The chart is a reasonably good overview of what ZEW economic experts think. For a time, U.S. economic expectations outstripped everyone else - but no more. Over the last few months, in fact, there has been a very slow upgrading in the current economic assessment across the board and some improvements made to the outlook as the U.S. has sunk into the pack.

Economic situation

The economic situation finds very high assessment for all the countries in the table except for the United Kingdom. The U.K. assessment in December has it only in its 49th percentile, just below its historic median with some very slow improvements to that assessment afoot. Taken as a whole, the euro area is in its 90th percentile as well as Germany, Japan and the United States. France and Italy have standings in their respective 80th percentiles. The euro area has had better assessments from the ZEW experts less than 8% of the time, historically. With one exception, these are all strong assessments. The euro area is also still in an uptrend unlike Germany that simply seems to get steady readings. The U.S. current assessment has been creeping up as has Japan's assessment and the assessment for France. Italy has been making improvement as well over the last three months and with a bit more vigor.

Macroeconomic expectations

Expectations are a different story with all assessments below or near their historic medians (median occurs for each at its 50th percentile mark). France is an exception that posts a 74th percentile standing. Germany's assessment has been steady over the past three months. The U.S. assessment has crept higher. Japan's assessment also is mostly moving sideways. Expectations for Italy are slowly improving. France is more or less at a steady and at quite a firm expectation level. France's momentum for expectations seems to have abated even as its current condition improves.

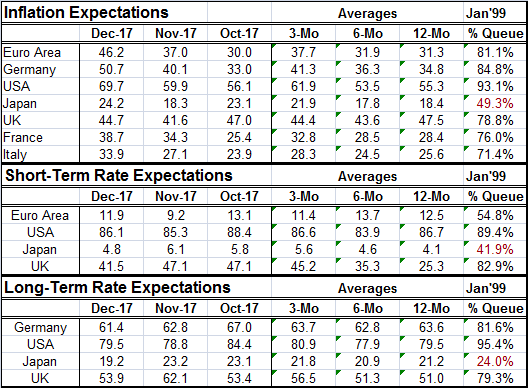

For inflation and interest rate expectations, only the U.S. has expectations at or near their 90th percentile. Germany and the euro area have inflation expectations in their 80th percentile decile. The U.K., France and Italy have expectations strewn across the 70th percentile decile. Japan, where it is trying to get inflation in gear, is the only country with its gauge below its median, but at the 49.3 percentile, Japan is now close to a median inflation expectations reading. However, in Japan there is no upward momentum to the inflation assessment. Everywhere else, except the U.K., inflation expectations are on a rising trend.

Short-term rates

Short-term interest rate expectations are not much of a surprise with the EMU at a 54th percentile standing and the U.S. at an 89th percentile standing. The euro area is in the process of dismantling its stimulus programs while the U.S. has been engaged in rate hiking since end-2015. The U.K. is given the same rough interest expectations as in the U.S. with a nearly 83rd percentile standing. Only Japan has short-term interest rate expectations below its historic median at a 41.9 percentile standing.

Long-term rates

Long-term rate expectations are more uniform because here EMU-area rates already are firmer but not rising. U.S. expectations are very high with a 95.4 percentile standing, but they are actually beginning to ease now. There is a slight easing of expectations in Japan and also in the U.K. Japan has an already low reading for long-term rate expectations stemming from accommodative policies buttressed by a yield curve target. The U.K. has much higher long-term expectations with a 79th percentile standing.

Summing up

On balance, the ZEW experts are playing conservative with their outlooks. But assessments of current conditions are improving steadily if slowly across the board. Compared to the economic situation seen over the last 12 months on average, most are substantially higher in December. The exception to this generalization is the U.K. which is weaker in December than it has been over 12 months on average. Expectations are much more varied on this same comparison to the 12-month average. Expectations for the U.K. inflation are higher in December than they have been over the last 12 months and for Japan too; at least that is good news for Japan. Inflation expectations like growth are creeping up. But the ZEW experts just can't seem to pull the trigger for optimism on expectations, too. Only France and Italy have much stronger expectations for growth in December, compared to their 12-month averages. The ZEW experts are part of the group that is driving this view of improving growth and rising inflation.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief