Global| Mar 20 2018

Global| Mar 20 2018ZEW Expectations for Germany and Elsewhere Drop Sharply; What Would a Trade War Look Like--Really?

Summary

The ZEW expectations for Germany as well as across a number of developed economies pulled back relatively sharply in March as fears of a trade war touched all the outlooks and the rising euro had some special consequences for EMU [...]

The ZEW expectations for Germany as well as across a number of developed economies pulled back relatively sharply in March as fears of a trade war touched all the outlooks and the rising euro had some special consequences for EMU members.

The ZEW expectations for Germany as well as across a number of developed economies pulled back relatively sharply in March as fears of a trade war touched all the outlooks and the rising euro had some special consequences for EMU members.

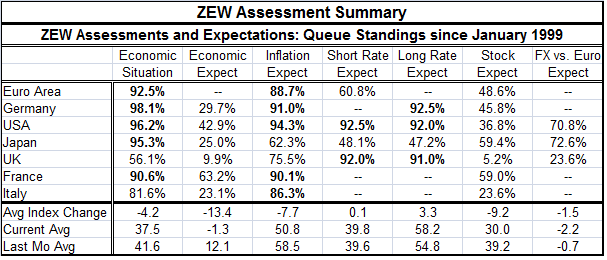

For Germany, the current index declined month-to-month and fell to its lowest level in three months. But German expectations fell even more abruptly, dropping from a value of 17.8 in February to settle at 5.1 in March. Expectations fell by over 12 points month-to-month and last exceeded such a drop in July 2016. The raw score diffusion reading of 5.1 was last lower in September 2016. German real exports are 50% of GDP (using 2010 basis euros) and in nominal terms goods and services exports are 48% of GDP. Obviously, anything about trade has the potential to rock the German economy. Between the up-creep in the value of the euro and U.S. President Donald Trump’s focus on trade and trade fairness combined with his actions on steel and aluminum, Germany has been put on-guard.

China is in the mix

In reaction to all this, China has already offered to open more of its economy. But the U.S. and China have a complicated economic and political relationship with so many U.S. firms located in China and with the U.S. having sought help from China in detaining North Korea while at the same time denying China’s claim to the South China Sea and dangling the potential for new relations with Taiwan that quickly have raised China’s ire. Geopolitics and trade quickly become linked in the modern world.

The trade game

Clearly, Germany is not the only nation with skin in the trade game. International trade has grown and flourished as the U.S. has a current account deficit that has become large and persistent. More than it just being a deficit, I think the size of the deficit and its persistence are the characteristics that have attracted the attention of Donald Trump as well as the attention of fair-minded economists who see the evidence of many things in this global trading system that do not look like the result of a free trade-based system. So now Trump has fired his warning shot and everyone is scrambling to react. Will there be a trade war? I doubt it. And I doubt it because this issue has been broadly studied and we know how it ends. Knowing that, there is no sense in even beginning. Moreover, Trump has showed that he is serious and not just making noises; this makes him dangerous. What makes it more dangerous is that maybe the U.S. is not as entitled as Mr. Trump claims on the specific issues of steel and aluminum as he has enunciated them, but Trump is largely right about trade not being fair to the U.S. and he is willing to take outside the box actions to get results and shake a few trees.

Handicapping a trade war and its odds...

There are (at least!) two models to use to understand what happens next. One is the way Trump approached Europe over NATO. Angela Merkel was angry and called the U.S. a bad ally. But Germany, a country with a fiscal surplus that has for years not lived up to its pledge to sustain military spending in support of NATO, was in default to its obligations. Many presidents before Trump had asked Germany and asked even Ms. Merkel herself to step up and pay. And she never did. But Trump’s rough, gruff, bombastic style got Germany off the dime and spending its own euros as it has previously promised. Trump prevailed. He huffed and he puffed, but he never intended to blow the NATO house down. A second way to understand this is through the lens of political scientist Daniel Ellsberg who is best remembered as the guy behind the release of the so-called Pentagon Papers. Ellsberg as a Rand analyst had pointed out that there is no way to assess the expected outcome of a nuclear war. Nuclear war was not a repeatable statistical event. It was binary. Either it would happen or it would not. And therefore there was no expected value for it or any way to assess it statistically. I believe there is a rough parallel to a trade war here, since it is well-known how destructive a trade war could be. And that is destructive enough to not want to be engaged in one. So if the U.S. is determined, belligerent and largely right (or having a strong point that cannot be dismissed), we are likely to see some sort of deal stuck to sweeten the pot for U.S. traders in world markets. In any event, it probably does mean less for other countries because it will mean more for the U.S. But we do not see that outcome in the ZEW assessments.

Of course, even when there is a preponderance of logic on your side, the logical course may not be the one that is followed. Countries have pride; their leaders have pride. So trade war still remains as a discountable possibility (more so that nuclear war- admittedly).

The ZEW experts and their assessments

But all of this explains why the ZEW expectations are lower across the board with Germany’s 12.7 point drop being only the fourth largest in diffusion points. Italy has a 20.7 point drop month-to-month, the U.S. has a 19 point drop, the U.K. has a 15.7 point drop, and then Germany has a 12.7 point drop. Right now I would suggest that this is bad and biased handicapping by the ZEW (German) financial experts who seem to see worse damage elsewhere when Germany is the country with the greatest trade exposure (exports at 48% of nominal GDP and imports at 40%).

Inflation and the outlook

While trade promotes efficiency and tariffs raise import prices, the ZEW experts see inflation lower in March than in February with trade war on the table. The inflation outlook change is lower for each country in the table. From this, we can conclude that ZEW experts seem to be handicapping an actual trade war in which the debilitating impact of trade war weakens economic growth creating deflation and dominating the impact of tariffs in pushing up import prices and in pushing up inflation. On the face of it, the ZEW inflation expectations and macro expectations do not appear to be in sync. Inflation expectations have been scaled back modestly to a level below their January level and above their December value, while macro-expectations have been rolled back farther. Still, inflation expectations average an 83rd percentile standing in this new world with new risks as of March while expectations are only peeled back to the lower one-third of their range (in general). For some reason, France will rate the strongest relative growth (highest queue standing) followed by the U.S. with all other countries in the lower 25th percentile of their historic queues on economic expectations or lower (e.g., the U.K.).The percentile standings for macro-expectations and expected inflation simply seem out of whack. Current conditions, inflation expectations, and expectations for interest rates all seem to be on the same page but macroeconomic expectations alone are low (but not that much different than they have been). Will the central banks continue to hike rates as they have been or, as they had been planning, if there is a trade war? That is doubtful, but that is also the ZEW view.

Given such changes, there are too few shifts in interest rates. Short-term rate expectations remain barely changed with long-term rate expectations a touch higher in general but just a tough higher leaving them at a 90th-plus percentile queue standing everywhere but in Japan.

The stock markets are noticeably weaker but still not weaker in a draconian fashion. Only Japan and France have stock market assessments that reside above their historic medians. The U.S. and Italy have the relative worst stock market reaction while in Germany stock market expectations are just a few ticks below their long-term median. Is that good analysis or wishful thinking from the German financial experts?

Forecasting in a swamp

It is very hard to make a forecast in a period like this. You are not going to make a forecast that there will be an outright major trade war and base everything on that as it would be a complete horror show. So you have to take that possibility and apply some discount factor to it and try to do that even handedly for everything that you forecast. I’m not sure that the ZEW experts have done that fairly. If there were any kind of a trade war, I’d expect Germany to be hurt worse. I’d also not expect France to be as insulated as they seem to have it. And Italy is already in bad shape so how much worse would a trade war be for Italy? And…if we are going to be logical about it, if Italy were really dragged down, it would probably boost the five-star movement further and could result in Italy choosing to leave the EMU creating a whole new wave of instability. The consequences of a trade war would be far reaching. Want an analogy? Just think of what the special prosecutor, Mr. Mueller, was set up to do and what he is now getting involved in. A trade war would spread like that in somewhat inconceivable ways with unpredictable connections.

The problem with disaster scenarios is that no one really wants to think through all the consequences. Disaster or the worst order of magnitude probably will not happen. But I think the ZEW people have this backward. I think exporting not importing countries will be hurt more. Importing countries have enough demand they are able to grow and do without some stuff – I get it, maybe a lot of stuff. But the U.S. has (1) energy and (2) food. Cut off the export market and suddenly (foreign) production has nowhere to go. Output piles up and excess inventories lead to layoffs and that leads to a spreading disaster. That will hit exporting nations the hardest. But I offer this one bit of hope for the future. Let’s, in this case, hope that on this occasion, time will not tell.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief