Global| Oct 13 2015

Global| Oct 13 2015ZEW Careens Lower

Summary

ZEW financial experts cut their assessment of current conditions in the German economy and chopped their expectations as well. Expectations were cut by 10.2 points while the current situation index was slashed by 12.3 points. These [...]

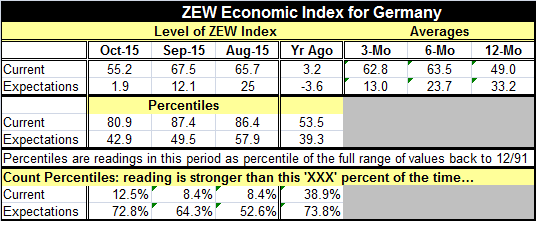

ZEW financial experts cut their assessment of current conditions in the German economy and chopped their expectations as well. Expectations were cut by 10.2 points while the current situation index was slashed by 12.3 points. These are substantial drops. The future index drops by more month-to-month only 17% of the time. The current index drops by more month-to-month less than 9% of the time. Expectations fell sharply for two consecutive months and that cumulative drop has been larger only 9% of the time.

ZEW financial experts cut their assessment of current conditions in the German economy and chopped their expectations as well. Expectations were cut by 10.2 points while the current situation index was slashed by 12.3 points. These are substantial drops. The future index drops by more month-to-month only 17% of the time. The current index drops by more month-to-month less than 9% of the time. Expectations fell sharply for two consecutive months and that cumulative drop has been larger only 9% of the time.

In terms of the standings of the ZEW indices, the current index is stronger only 12% of the time. So the Germany economy is still doing quite well even if that reading is down from 8.4% last month. Expectations are where we see the wear and tear taking place. Expectations are better only 72.8% of the time- only about one-quarter of the time. And this is sharply higher (worse off) than last month when expectations were worse only 64.3% of the time (about one-third of the time). The ZEW experts are getting more worried about the future.

ZEW financial experts have cut their view of profitability in 10 of 13 market sectors. The ranking of profitability by sector is the weakest it has been in one year on the ZEW professionals' estimates. Profitability estimates have been cut steadily since March of this year.

The VW scandal has come home to roost in Germany this month along with still-entangled economic conditions. Today Germany affirmed its zero year-over-year rate of inflation. The U.K. reported a return to negative inflation. Clearly, global weakness and weak/dropping commodity prices are still taking a toll. Developing economies are destabilized and the feedback through export performance is hitting developed economies hard.

China is getting worse. Today China reported a current account surplus at $60.3 billion in September nearly even with August and failing to fall to under $50 billion as had been expected. China's imports fell 20.4% year-on-year. Clearly, China is set to transmit even more weakness abroad. Conditions there are so bad that officials announced that China is going to give growth the priority over economic restructuring in the period ahead. China's Communist Party's central committee will meet from October 26-29 to set out its 13th five-year plan, a blueprint for economic and social development in the target period of 2016 and 2020. At that time, we will see what goals it actually adopts. For now, China appears to be a colossal drag on global growth. It seems to be wedded to keeping its reliance on exports in place for a longer stretch of time to support growth. That is not good news for the rest of the world.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.