Global| Jul 10 2018

Global| Jul 10 2018ZEW Assessments Are Trimmed in July

Summary

The ZEW expectations and assessments were cut in July with average percentile standing ranking falling by 1.6 points and with France’s 4.3 point drop and Italy’s lone gain of 1.7 points as the outliers on either side. Apart from [...]

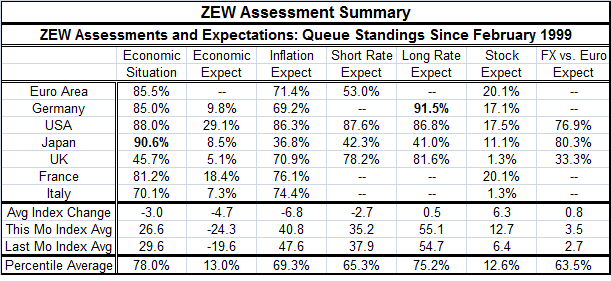

The ZEW expectations and assessments were cut in July with average percentile standing ranking falling by 1.6 points and with France’s 4.3 point drop and Italy’s lone gain of 1.7 points as the outliers on either side. Apart from Italy, all assessments of the current situation were trimmed with the U.S. and Japan’s 0.4 point trimming being the most modest. The ZEW financial experts are trying to assess the impact of tariffs on the outlook and some swirling cross currents.

The ZEW expectations and assessments were cut in July with average percentile standing ranking falling by 1.6 points and with France’s 4.3 point drop and Italy’s lone gain of 1.7 points as the outliers on either side. Apart from Italy, all assessments of the current situation were trimmed with the U.S. and Japan’s 0.4 point trimming being the most modest. The ZEW financial experts are trying to assess the impact of tariffs on the outlook and some swirling cross currents.

I plot the macroeconomic expectation indexes for the U.S., Japan and Germany. A sharp slide for all three countries is clearly the order of business since early 2018 and from there, a substantial dip to log negative readings. Economic expectations standings average a very low 13th percentile standing with standings for Germany, Japan, Italy and the U.K. all in single digits (in their lower 10 percentile range). The average reading is boosted by the French standing at 18.4% and the U.S. which is still quite weak at a 29th percentile standing. All expectations were trimmed on the month except for Italy where there was a sizeable 11.2 point gain in its assessment. The average macroeconomic assessment in the table fell by 4.7 points on the month.

The macro assessment (expectation) is very weak. It has been weaker less than 6% of the time since end-1991. There are only two episodes when the unweighted ZEW macro indicators were weaker than they are now. One was in the global recession and financial crisis from November 2007 through January 2009. The other was from September 2011 through December 2011. In the financial crisis, the average reading for macro expectations was -41.5 ranging from -32.1, which was both the starting and the ending readings to the weakest reading of -59.5 in October 2008. While the average reading is quite weak reading -24.3 this month, it is still a long way from the extreme weakness registered in the last recession. But just as clearly ZEW experts are already worried about the outcome. And tariffs are only just being imposed; we have seen no damage from them as of yet.

Apparently the ZEW advisors see the tariff-tradeoff as deflationary despite the obvious import-price raising impacts. Inflation expectations in July are weaker everywhere except in the U.S. where the inflation expectation is just a couple of points higher. Inflation expectations are still elevated as the average standing for the group is at 69.3%. The U.S. standing is in its 86th percentile, compared to a 71st percentile for the EMU and still very low 36th percentile for Japan.

The ZEW experts see slightly lower short-term rates and slightly higher long-term rates compared to last month. The short-term rate result is driven by trends in the U.K. and EMU while the U.S. is an exception with short-term rates seen higher. Long-term rates are seen higher in Germany, the U.S. and Japan, but lower on balance in the U.K. The short-term rate expectation standings are all over the map. Japan has the lowest expectations with a standing at its 42nd percentile. The EMU has short-term rates at a 53rd percentile standing and the U.K. has a much higher 78th percentile standing with the U.S. at an 87th percentile standing. Yet, inflation is building almost nowhere. But for long-term rates, the German standing is the highest at its 91.5 percentile, followed by the U.S. at is 86.8 percentile and the U.K. at its 81.6 percentile. Japan’s 41st percentile standing is similar to its short-term percentile. It is the German-EMU long-term/short-term percentile standings that are so different.

Expectations for equities improved across the board but nowhere as dramatically as in Italy where the stock market assessment rose from -26.3 in June to -7.0 in July. Even so, the Italian equity market outlook is still net lower over three months such has been the impact of Italian political uncertainty on markets.

Obviously, the outlook is a bit upside down at the moment as Europe is dealing with all sorts of stimulus from Brexit, to migrant issues, to U.S.-imposed tariffs, to a dispute over NATO funding and an unraveling Iran nuclear deal, just to name a few of the bigger things in transition. The outlook has been deteriorating and sharply. However, the current situation had improved steadily and quite smartly in the course of 2017 having since flattened out in the U.S. in 2018 and begun backsliding in the EMU and in Japan in 2018. There remains a lot of uncertainty about how these various bargaining arrangements will settle out. It seems certain that there is going to be more pain before any deal is struck on tariffs. We are clearly sliding into the unknown in 2018 and we are all wondering how deep the pit will turn out to be. Some are still looking for growth acceleration. Well, good luck with that.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief