Global| Feb 25 2009

Global| Feb 25 2009Yen-Based Japan Exports Are Cut Nearly In Half

Summary

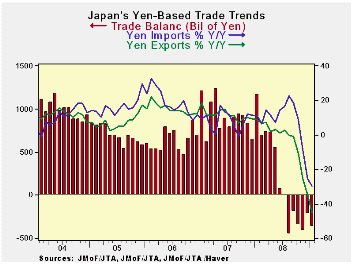

In a stunning blow to a reeling economy Japan reports that its exports are lower in January compared to one year ago by 45% - nearly halving of the flow. There are several components to this drop. One is the yen that has risen; that [...]

In a stunning blow to a reeling economy Japan reports that its

exports are lower in January compared to one year ago by 45% - nearly

halving of the flow. There are several components to this drop. One is

the yen that has risen; that will translate foreign currency-based

Japan exports into a smaller value in terms of yen. The yen rose to

90.12/$ in January compared to its level of 101.91/$ a year ago, a yen

rise of 16%. Another aspect of the drop in value is that yen-based

export prices have fallen Year over year. Japan export prices fell by

13.5% Year over year. These two factors make up a good deal of the 45%

drop in the yen value of Japan’s exports. But not all of Japan’s

exports are in dollar terms. Japan’s largest trade partner in fact is

China; its second largest partner is the US. Moreover, the drop in the

current value of yen trade flows is not simply an ‘index number’

problem. It does reflect real stress that flows back to Japan when

export dollar sales buy fewer yen, especially if Japan’s costs are

expressed in yen- as most surely are despite outsourcing.

Japan’s imports are down by nearly 30% Year-over-year, another

significant number. The rise in the yen plays a role there by first

taking a fixed import bill expressed in foreign currency and making it

smaller when translated into a stronger yen, just as for exports. But

eventually the stronger yen and weaker FX value of competing currencies

should lead to an increase in Japan’s import volumes and cause yen

VALUE flows to rise or at least to mitigate their drop (depending on

the size of the import price elasticities). Let’s look at this concept

of ‘elasticity:’ If Japan import price elasticities are less than

‘minus one’ Japan’s import values will eventually rise further as Japan

buys more of the cheaper import and that offsets the fact that each

import is worth fewer yen by increasing the volume of its purchases.

That is what the concept of elasticity measures. A price elasticity of

less than ‘minus one’ means that a one percent drop in yen prices (say

forced by a yen appreciation) will lead to more than a one percent

increase in the volume of goods imported. Yen import prices are falling

already (mostly lower oil prices). But the progression of events that

lead to a boost in import volumes takes time. Plus don’t hold your

breath waiting for this impact since Japan’s own recession is

contracting imports, a factor that will swamp and elasticity effect

from prices. For the moment, yen-based import prices are down by nearly

25% Yr/Yr accentuating any VOLUME drop in Japan’s imports on observed

import VALUE. Of course, to the extent that Japan invoices its imports

in yen the result of the yen’s rise would me blunted, since a yen

import is a yen import regardless of the dollar, euro or yuan exchange

rate.

On balance these trade flows for Japan paint a very distressed

picture of Japan’s economy. Japan has joined Germany and others in

being a voice in favor of maintaining ‘free trade.’ Just today the WTO

has issued another call for nations to uphold their free trade

agreements. The ‘buy America’ clause in the US stimulus bill is one

development that is cited again and again in these sorts of

communiqués. The US insists that its provision is fully consistent with

its free trade agreements.

We can see that with the world economy shutting down, like

some out of control Windows command that is turning off your computer

while you are trying to work, that chaos is being spread. Export

dependent nations are being crushed by the global economies since

manufactured goods exports have high relatively high income

elasticities. That means when times are good and global incomes are

growing exports shoot ahead strongly but it also means that export

volumes contract sharply in a downturn. Japan is being battered in part

by the impact of US auto sales dropping from over 15mu to just about

10mu. There is nothing anticompetitive about that: it’s just recession.

That is a drop of 33% and it will cause the Yr/Yr drop in yen exports

to be registered at about 46% if Japan holds its share in this

contracting market. Of course cutting back on shipments to the US to

trim inventories plus taking lower prices into account could further

exaggerate the flow’s ultimate decline. In the event, Japan’s exports

of autos in yen terms to the world have fallen by 66% since January of

one year ago.

| Japan Trade Trends | |||||||

|---|---|---|---|---|---|---|---|

| in period level of % ch | Average in period/or % change | ||||||

| All data yen basis | Jan-09 | Dec-08 | Nov-08 | 3Mprev | 6Mprv | 12-Mprv | 12 mo Ago |

| Balance on Goods | #N/A | (1,341) | (3,343) | (1,167) | (70) | 3,271 | 10,356 |

| % m/m | % saar | ||||||

| X Goods % | -10.4% | -11.6% | -13.4% | -83.5% | -63.5% | -44.9% | 8.8% |

| Motor Vehicles | -39.0% | -18.1% | -20.6% | -98.2% | -89.1% | -66.1% | 12.7% |

| M Goods %, | -6.9% | -14.2% | -11.7% | -79.5% | -57.1% | -29.6% | 11.3% |

| Motor Vehicles | -24.4% | 7.4% | 6.2% | -74.1% | -61.1% | -31.5% | 4.3% |

| Prices In %, saar | 3M | 6M | 12-M | 12 mo Ago | |||

| PX | 0.1% | -4.4% | -3.7% | -46.8% | -29.0% | -13.5% | -5.7% |

| PM | -4.2% | -11.4% | -10.3% | -77.8% | -57.0% | -24.6% | 7.4% |

| Memo: Yen/$, AVG, Level | 90.12 | 91.28 | 96.97 | 92.79 | 99.05 | 101.91 | 116.72 |

| Memo Yen Percent ('-' is a fall) | 1.3% | 5.9% | 3.0% | 48.9% | 28.9% | 16.4% | 10.5% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief