Global| Sep 15 2009

Global| Sep 15 2009US Retail Sales Make StrongGains...

Summary

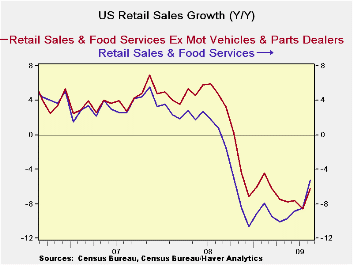

US retail sales rang up strong results in August. The cash for clunkers program aided auto sales to a greater extent that most economists had anticipated. Sales rose by 2.7% month-over-month boosted by vehicle sales which rose by [...]

US retail sales rang up strong results in August. The cash for

clunkers program aided auto sales to a greater extent that most

economists had anticipated. Sales rose by 2.7% month-over-month boosted

by vehicle sales which rose by 10.7% on the month. Most major

categories of sales rose in the month; furniture and electronics was a

minor exception dropping by 0.1% and building materials was a major

exception falling by an outsized 1.2% on the month. Stripping out

gasoline stations where sales rose 5.1% mostly on higher prices and

removing motor vehicles as well left retail sales up by 0.6% on the

month. That particular sub-group exhibits improving sequential growth

rates as well.

Year-over-year sales declines are still severe and that is a

legacy of the severity of the recession and its impact on the consumer.

Over 7miln jobs have been lost in the business cycle and that is a huge

loss of income and of spending power for those consumers. But while the

Yr/Yr drops are severe there are also some distortions. Nondurable

goods sales excluding gas stations are down by only 0.9% Yr./Yr.

Durables spending is down by 5.8% Yr/Yr on large declines in building

materials and in furniture. The boost to vehicle sales this month

leaves them lower Yr/Yr by just 1%.

The messages from this report are that the consumer sector has

been hit hard by recession. Cash for clunkers has boosted auto’s up

form weakness overall and has given those sales a huge boost in the

month- a boost that is likely not sustainable – that’s the bad news

looking ahead. Still, the August results leave sales in the new quarter

(Q3) expanding at an annual rate of 9.5%. Extracting the vehicle

component that growth rate comes down to 2.7%. Ex food and energy sales

are up at a pace of 8.5% in Q3 and estimating the inflation impact

leaves real core sales up at a pace of nearly 7% at an annual rate in

Q3 compared to Q2. This is the compounded growth rate for Q3, two

months into the quarter. But a drop off in auto sales is likely to trim

this impact of quarterly consumer spending on retail sales by the time

the quarter’s final numbers are in.

While it is good news for August and it the best news may be

that sales have spread beyond autos, and have done so without a

government help plan. The real question is how far will auto sales fall

when the cash for clunkers program ends? There will be a spillover of

some sales into September but Q4 will have to do what it can without

any boost from this special program. All that raises some questions

about the future, despite some nice improving fundamentals for the

economy. The downside of government support programs is that those

programs one day end… a second downside factor is that somebody has to

pay for them.

| Retail Sales Trends | |||||

|---|---|---|---|---|---|

| Mo/Mo | Seasonally Adjusted Annual Rate | ||||

| Retail Aggregates | 2009.Aug | 3-Mo | 6Mo | Yr/Yr | YrAgo:Y/Y |

| Retail & Food Service | 2.7% | 14.3% | 4.7% | -5.3% | 0.8% |

| Retail Excl MV&Parts | 1.1% | 5.1% | 0.1% | -6.2% | 4.7% |

| Retail Excl MV&Parts&Gas | 0.6% | 1.0% | -2.3% | -2.9% | 2.5% |

| Durables | 2009.Aug | 3-Mo | 6Mo | Yr/Yr | YrAgo:Y/Y |

| Totals | 5.9% | 32.1% | 10.8% | -5.8% | -10.1% |

| Building Materials | -1.2% | -13.6% | -9.5% | -13.6% | -2.0% |

| Motor Vehicles & Parts | 10.6% | 70.3% | 29.5% | -1.0% | -14.4% |

| MV Dealers | 11.9% | 83.3% | 35.0% | -0.8% | -15.9% |

| Furniture,electonics,etc | -0.2% | -4.5% | -15.9% | -11.6% | -5.0% |

| NonDurables | 2009.Aug | 3-Mo | 6Mo | Yr/Yr | YrAgo:Y/Y |

| Totals | 1.4% | 7.8% | 2.3% | -5.1% | 6.2% |

| Food&Bev | 0.5% | 0.9% | 1.9% | -1.1% | 6.8% |

| Health | 0.4% | 1.3% | 2.3% | 2.9% | 3.2% |

| Gasoline | 5.1% | 47.4% | 24.5% | -26.7% | 20.6% |

| Clothing | 2.4% | 1.2% | -4.8% | -5.1% | 0.6% |

| SportGoods | 2.3% | 12.8% | 0.4% | -0.4% | 0.6% |

| GenlMerch | 1.6% | 5.0% | -1.9% | -0.7% | 3.7% |

| NonStore Retailers | 0.1% | 9.7% | 2.5% | -2.6% | 4.0% |

| Misc Retail | 0.2% | 1.3% | 2.3% | 2.9% | 3.2% |

| NonDurables EXCL Gas | 0.8% | 3.2% | -0.4% | -0.9% | 3.8% |

| Services | |||||

| Food Service & Drinking | 0.3% | -0.5% | -1.7% | 0.7% | 3.7% |

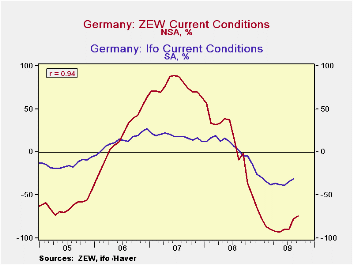

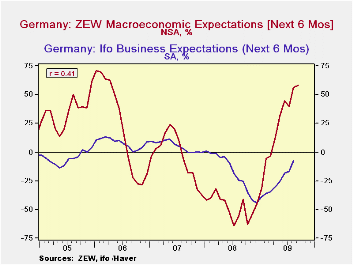

Optimism Among German Investors Somewhat Subdued

by Louise Curley September 15, 2009

In the September ZEW survey, released today, German analysts

and institutional investors were only slightly more optimistic about

the next six months than they were in August. The ZEW balance of

optimists over pessimists rose only 1.2 percentage points from 56.1% to

57.7%. The views of the financial community tend to be considerably

more volatile than the views of those engaged in industry, trade and

services. The latter represented in the IFO measure of German economic

opinion, were still showing an excess of pessimism regarding

the outlook for the next six months of 7.7% in August. The two measures

are shown in the first chart. The correlation between the two series is

only .41 suggesting that the two groups frequently differ as to the

outlook.

The German investors were also subdued in appraising the current situation. The excess of pessimists regarding the current situation declined only 3.2 percentage points to 74.0 from 77.2 in August. Again, the views of the financial community are more volatile than those of the participants in the IFO survey. The excess of pessimists among the latter was only 31% in August. In contrast to their often divergent views on the outlook the two communities tend to view the current outlook similarly. In spite of the greater volatility, the views of the financial community move in the same direction as that of the business community, as attested by the high degree of correlation--.94--between the two series shown in the second chart.

According to the President of ZEW, Prof, Dr. Dr. h.c. mult. Wolfgang Franz, "The economic expectations for Germany are consistent with the picture that the Germany economy is recovering, but at a slow pace."

| Sep 09 | Aug 09 | Sep 08 | M/M | Y/Y | 2008 | 2007 | 2006 | |

|---|---|---|---|---|---|---|---|---|

| ZEW % balance | ||||||||

| Current Conditions | -74.0 | -77.2 | -1.0 | 3.2 | -73.0 | 7.3 | 75.9 | 18.3 |

| Expectations for Economy 6 mos ahead | 57.7 | 56.1 | -1.0 | 1.6 | 98.8 | -47.5 | -3.0 | 22.3 |

| IFO % balance | ||||||||

| Current Conditions | n.a. | -31.0 | -- | n.a. | n.a. | 4.0 | 18.1 | 12.7 |

| Expectations 6 mos ahead | n.a. | -7.7 | -- | n.a. | n.a. | -17.4 | 5.2 | 7.9 |

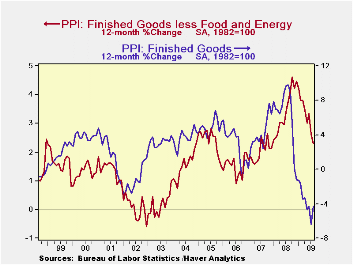

PPI Headline Spurts As Core Is Stable

by Robert Brusca September 15, 2009

The PPI headline spurted by 1.7% in August as the core rose by

02% and core for consumer prices at the producer level edged up by just

0.1%. Finished energy prices rose by 8% in the month. The headline

displays an accelerating pattern of growth rates for 12-month to

6-month to 3-month rates of inflation. But the core pattern has been

more settled and core pattern for consumer prices at the producer level

has been even more tranquil.

We learned from the last time energy prices spiked in the

recession that a transmission of their gains to the core was not

automatic. Rising energy prices have both inflationary and deflationary

effects. When consumers and firms do not have the power to bargain for

wage and price hikes, as is the case now, it is more likely that rising

energy prices impact growth adversely instead of impacting inflation

positively.

Still what we are seeing here are volatile price movements.

Energy prices have had a standard deviation of 5 percentage points on

the month to month percentage changes since the recession began. That

kind of volatility tends to impart considerable uncertainty into the

headline PPI each month.

The 8% m/m rise in energy prices in August is the largest

since a 10.2% gain in November 2007. Energy prices are up in four of

the last five months and in six of the last eight months. Prior to that

energy prices had fallen for five months in a row.

Spot oil prices on world markets, however, have been hovering

around the $70/bbl mark for a number of months. Oil prices have been

playing catch up since the recession has come off its worst of times

and oil prices have bounced and are trying and find a new higher

equilibrium.

For now the core PPI price patterns are reassuring. Since

global oil price trends are not running away we can look for the energy

market in the US to find a level that is consistent with global prices

and for the energy component of the PPI to settle down. It does not

look very inflationary now in this economy but we are looking for

recovery to set in. As that happens the risk will multiply and the

potential for inflation to take root will improve somewhat. I am no

inflation monger. But circumstance will change. For now inflation is

not the worry, it’s just a bad monthly result in the least important of

all US inflation reports.

Long live the CPI and the PCE deflator where trends are more important. In that regard the tranquil inflation embedded in core consumer prices at the producer prices level is reassuring.

| Key Trends In Producer Prices | |||||

|---|---|---|---|---|---|

| Aug-09 | PPI Trends By Type Of Good | ||||

| PPI | 1Mo:M/M | 3-Mo:ar | 6-Mo:ar | 1-Yr | Yr-Ago |

| Total PPI | 1.7% | 11.0% | 4.3% | -4.3% | 9.8% |

| Finished Consumer Gds | 2.3% | 14.4% | 5.5% | -5.9% | 11.7% |

| Consumer Foods | 0.4% | 0.0% | -1.7% | -3.9% | 9.1% |

| Finished C Gds Excl Foods | 2.9% | 19.5% | 8.1% | -7.0% | 12.7% |

| Nondurables less Food | 3.9% | 26.6% | 10.4% | -10.4% | 16.6% |

| ConsNonDurxF&E | 0.0% | 1.9% | 2.0% | 3.0% | 5.4% |

| Durable Goods | 0.3% | 2.8% | 2.1% | 2.5% | 2.2% |

| Finished Core Cons Gds | 0.1% | 2.2% | 2.0% | 2.8% | 4.0% |

| Capital Goods | 0.3% | 2.3% | 0.6% | 1.8% | 3.3% |

| MFG Industries | 0.1% | 0.8% | 0.3% | 0.6% | 3.9% |

| NonMFG Industries | 0.3% | 2.9% | 0.8% | 2.2% | 3.1% |

| Core PPI | 0.2% | 2.4% | 1.4% | 2.3% | 3.8% |

| Memo: Finished Energy | 8.0% | 59.6% | 19.8% | -21.3% | 27.9% |

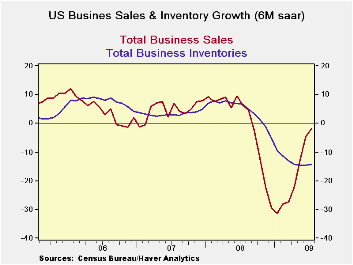

Sales Trim Losses As Inventories Are Looking Lean

by Robert Brusca September 15, 2009

Inventories fell again in the current month. Still the 1% drop

while large is the smallest drop in eight months. Inventories average a

1.3% monthly decline in Q2 so in Q4 inventories are improving by 30%

over the previous quarter.

The inventory conundrum - For the impact

on GDP, it is not the change in inventory levels that matters but the

change in the change. If inventories fall by the same amount in each

month of Q2 and in Q3 the change in inventory investment will be zero

(the same amount of investment in each quarter). The fact that

inventories are falling by less in Q3 is the key to seeing there is a

boost in GDP in the offing even though inventories are still falling.

Right now the average drop per month in Q3 is $13bln compared to a drop

of $18bln in Q2. Annualize that difference and you get a large swing.

Still you still have to inflation-adjust those numbers and remember, it

is only one month in the new quarter. But you get the picture.

Inventories are a positive factor already.

I to S ratio is LOW - In the table above we

show the percentile standing of the I-to-S ratio in its three-year

range. For retailers it is the lowest inventory-to-sales ratio in three

years. Wholesalers have inventories at a mid range mark, while for

manufacturers inventories are still in the top 22% of their three year

range (78th percentile) relative to sales.

Sequential growth trend is your friend--

The sequential growth rates show that the pace of sales has moved from

the negative to the positive from 12-months to six-months to 3-months

across manufacturers, retailers and wholesalers. This is good news. The

pace of inventory declines for the most part seems to have plateaued as

three month growth rates are even with six month growth rates for the

major business sectors.

The end of days…the dog days -- Despite the fact that inventories are still declining you cans see the whites of the business expansion’s eyes. The end of recession is at hand; the start of recovery is in play. Sales are on an upswing across sectors the I-to-S ratios are mostly low and the pace of the inventory decline is flattening out. These facts should make inventories a positive factor for growth in Q3 and could make them a powerful factor for Q4 growth as well. Remember that inventories are still falling and the rebuilding process has not yet begun, so this switch powered eventually by inventory growth, not just slower paring, could go on for some time.

| 2009.Jul | Inventory and Sales Paired Growth Rates by Major Divisions | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| 3-Mo Growth |

6-Mo Growth |

12-Mo Growth |

YrAgo Growth |

I:S ratio |

|||||

| Sales | Inventory | Sales | Inventory | Sales | Inventory | Sales | Inventory | %-tile | |

| Total Business | 4.7% | -13.6% | -1.9% | -14.2% | -17.8% | -11.8% | 7.9% | 6.7% | 52.4% |

| Manufacturers | 3.8% | -10.0% | -3.6% | -11.8% | -22.2% | -10.0% | 7.1% | 7.8% | 78.6% |

| Retailers | 5.5% | -14.6% | 0.2% | -13.9% | -9.5% | -12.9% | 1.5% | 2.2% | 0.0% |

| Wholesalers | 5.0% | -17.0% | -2.0% | -17.4% | -19.8% | -12.8% | 15.2% | 11.0% | 52.2% |

| Ratio of STOCKS to Sales; Stocks Vs Flows | |||||||||

| Inventory-to-Sales Ratios In Perspective | Over three Years | ||||||||

| 2009.Jul | Current | 3Mo Ago |

6Mo Ago |

Yr Ago |

2Yrs Ago |

3Yrs Ago |

%-tile | Max | Min |

| Total Business | 1.36 | 1.43 | 1.46 | 1.27 | 1.28 | 1.28 | 52.4% | 1.46 | 1.25 |

| Manufacturers | 1.40 | 1.45 | 1.46 | 1.21 | 1.20 | 1.19 | 78.6% | 1.46 | 1.18 |

| Retailers | 1.45 | 1.53 | 1.57 | 1.51 | 1.50 | 1.50 | 0.0% | 1.62 | 1.45 |

| Wholesalers | 1.23 | 1.31 | 1.34 | 1.13 | 1.17 | 1.17 | 52.2% | 1.34 | 1.11 |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief